· Abhilash John Philip · 65 min read

Location Evidence Requirements for Digital Sales: Complete 2026 Tax Compliance Guide [EU, US, Asia-Pacific]

Master location evidence requirements for digital sales across 50+ countries. Complete guide to VAT/GST compliance, two-piece evidence rule, tax technology, and audit-proof documentation for SaaS, e-commerce, and digital services.

TL;DR: Key Takeaways

- The Golden Rule: For most global sales (EU, UK, APAC), you must collect two pieces of non-conflicting evidence to prove customer location (e.g., Billing Address + IP Address).

- US Complexity: The US uses “economic nexus” thresholds ($100k sales or 200 transactions) rather than strict evidence counting, but 50 states have different rules.

- Automation is Mandatory: You cannot manually verify location for every SaaS transaction. Use a tax engine or Merchant of Record (MoR) to automate this.

- The Risk: Failure to prove location shifts the tax liability to you (the seller), with penalties up to 75% in some jurisdictions.

Table of Contents

- Understanding Global Location Evidence Requirements

- EU VAT Location Evidence Rules (27 Member States)

- US Sales Tax Location Requirements (50 States)

- Asia-Pacific Digital Tax Location Rules

- Location Evidence Collection: Step-by-Step Process

- Tax Technology Stack for Location Compliance

- Future-Proofing Location Evidence Systems

- Frequently Asked Questions

In the borderless digital economy, determining and proving customer location has become the cornerstone of tax compliance for SaaS companies, digital content providers, and e-commerce businesses. Whether you are selling software subscriptions in Stockholm, streaming content in Singapore, or online courses in San Francisco, understanding location evidence requirements for digital sales is no longer optional—it is the foundation of avoiding costly penalties and audit findings across fifty-plus tax jurisdictions worldwide.

The fundamental question haunting every digital business operating internationally is deceptively simple: where is your customer located, and how do you prove it to tax authorities in a way that withstands audit scrutiny? Since the landmark European Union VAT reforms of 2015, which shifted taxation of digital services to the customer’s location rather than the seller’s location, tax authorities across North America, Europe, Asia-Pacific, Latin America, and the Middle East have implemented similar destination-based taxation systems, each with unique location evidence requirements, retention obligations, and penalty structures.

The stakes for getting location evidence wrong are extraordinarily high across all major markets. In the European Union, inadequate location evidence can result in penalties reaching thirty percent of tax due plus interest. United States state tax authorities impose penalties ranging from ten to twenty-five percent of uncollected tax, with some states adding criminal sanctions for willful non-compliance. Australian and New Zealand tax authorities can assess penalties up to seventy-five percent for deliberate avoidance. Beyond financial penalties, businesses face reputational damage, customer trust issues, and potential marketplace suspensions when location evidence failures come to light during audits.

Understanding Global Location Evidence Requirements

Location evidence for digital sales tax refers to the documentation and data points that businesses must collect, validate, and retain to prove where their customers are located for tax purposes. This seemingly straightforward concept becomes remarkably complex when applied across different tax jurisdictions, each with varying definitions of customer location, different standards for acceptable evidence, and different requirements for evidence quantity and retention periods.

The complexity facing digital businesses is not merely compliance with one set of rules, but rather navigating dozens of different regulatory frameworks simultaneously. A SaaS company selling project management software globally might need to comply with European Union VAT location evidence rules requiring two pieces of non-contradictory evidence, United States economic nexus thresholds across fifty states with varying location determination methods, Australian GST customer location requirements, Canadian GST with provincial variations, Singapore GST location rules, and emerging digital services taxes in India, South Korea, Japan, and numerous other markets.

Location Evidence Requirements by Major Jurisdiction (2026)

| Jurisdiction | Evidence Pieces Required | Acceptable Evidence Types | Retention Period | Registration Threshold |

|---|---|---|---|---|

| European Union (27 states) | 2 non-contradictory pieces (B2C); VAT ID (B2B) | Billing address, IP geolocation, bank details, MCC, landline location, VAT number (B2B) | 10 years | €10,000 (simplified), €0 (standard) |

| United States (50 states) | Reasonable documentation | Billing/shipping address, IP address, customer declaration, resale/exemption certificates (B2B) | 3-7 years (varies by state) | $100,000 or 200 transactions (typical) |

| Australia | 2 non-conflicting pieces; ABN (B2B) | Billing address, payment details, IP location, customer declaration, Australian Business Number (B2B) | 5 years | AUD $75,000 |

| United Kingdom | 2 pieces of evidence (B2C); VAT number (B2B) | Billing address, IP location, bank location, SIM card MCC, VAT number (B2B) | 6 years | £85,000 |

| Canada | 2 pieces of evidence; GST number (B2B) | Billing address, IP geolocation, payment information, GST/HST registration number (B2B) | 6 years | CAD $30,000 |

| New Zealand | 2 non-conflicting pieces; GST number (B2B) | Billing address, bank details, IP address, customer location, GST registration number (B2B) | 7 years | NZD $60,000 |

| Singapore | Sufficient evidence; GST number (B2B) | Billing address, IP location, payment details, SIM card country, GST registration number (B2B) | 5 years | SGD $1,000,000 global + SGD $100,000 Singapore |

| India | Documentary evidence; GSTIN (B2B) | Billing address, IP address, payment bank location, GSTIN (B2B) | 6 years | No threshold (all B2C sales) |

| Japan | Appropriate evidence; registration number (B2B) | Address, IP location, credit card issuing country, Qualified Invoice Issuer number (B2B) | 7 years | ¥10,000,000 |

| South Korea | Location verification; business number (B2B) | Address, payment card country, IP geolocation, Business Registration Number (B2B) | 5 years | No threshold |

Why Location Evidence Has Become Critical for Digital Businesses

The shift toward destination-based taxation for digital services represents one of the most significant changes in international tax policy over the past decade. Historically, businesses paid taxes where they were physically located—their headquarters, offices, or warehouses. This model worked reasonably well for traditional brick-and-mortar retail but created massive distortions in the digital economy where a company in Ireland could sell to customers in Germany without collecting German VAT.

Tax authorities worldwide recognized that this system allowed digital companies to concentrate operations in low-tax jurisdictions while serving customers globally, creating competitive disadvantages for domestic businesses and eroding tax bases. The solution was destination-based taxation: requiring businesses to charge tax based on where customers are located, regardless of where the business operates.

However, this solution created an operational challenge that did not exist under origin-based taxation. Businesses now must determine customer location for potentially millions of transactions annually, apply different tax rates for each location, register with tax authorities in jurisdictions where they have no physical presence, and prove to auditors years later that they correctly determined customer location for every single transaction.

EU VAT Location Evidence: The Pioneer Framework

The European Union fundamentally transformed digital taxation on January 1, 2015, when it implemented rules requiring that telecommunications, broadcasting, and electronically supplied services be taxed where the customer belongs, regardless of whether that customer is a business or a consumer. This landmark change affected every business selling digital services to EU customers, from multinational corporations to solo entrepreneurs selling e-books from home offices.

What Qualifies as Electronically Supplied Services Under EU VAT

Understanding whether your product qualifies as an electronically supplied service under EU VAT rules is the essential first step. The VAT Implementing Regulation defines electronically supplied services as those delivered over the Internet or an electronic network where the supply is essentially automated, involves minimal human intervention, and is impossible to ensure in the absence of information technology.

The regulation provides extensive lists of services that qualify, including website hosting and web hosting services, distance maintenance of programs and equipment, software supply and updates, supply of images and text and information, making databases available, supply of music and films and games including gambling games, political and cultural and artistic and sporting and scientific and entertainment broadcasts and events, and supply of distance teaching where content is automated.

Specific examples that clearly qualify as electronically supplied services under current EU regulations include Software-as-a-Service platforms like CRM systems and project management tools and accounting software, cloud storage and file sharing services, website themes and templates and plugins, stock photography and video footage and music libraries, e-books and digital magazines and online newspapers, streaming video services and video-on-demand platforms, music streaming and downloadable music files, online gaming including mobile games and browser-based games, webinar platforms and online course platforms with automated content delivery, and SEO tools and marketing automation platforms.

Importantly, the regulation also specifies services that do not qualify as electronically supplied services, even when ordered online. Physical goods remain outside the scope even if ordered through electronic systems. Professional services such as legal advice or financial consulting delivered via email do not qualify because they require substantial human intervention. Teaching services where a live instructor delivers content remotely do not qualify, though this distinction has become more nuanced with the rise of hybrid learning platforms. Offline computer repair services, telephone helpdesk services requiring human interaction, and tickets to events booked online also fall outside the electronically supplied services definition.

The EU Two-Piece Evidence Rule: Requirements and Implementation

The European Union’s approach to location evidence balances the need for compliance certainty with practical business realities. Recognizing that determining customer location with absolute certainty is often impossible, EU regulations created a sophisticated system of presumptions allowing businesses to rely on collected evidence without conducting extensive customer investigations.

For business-to-consumer transactions where the customer is not VAT registered, suppliers must determine where the consumer is registered, has their permanent address, or usually lives. The regulations provide several pathways to make this determination, starting with specific presumptions applicable in defined situations.

When services are supplied through a fixed landline, the customer is presumed to be located at that landline’s registered location. This presumption works well for traditional internet services delivered through DSL or cable connections tied to specific addresses. When services are supplied through mobile networks, the customer’s location is determined by the Mobile Country Code embedded in the International Mobile Subscriber Identity stored on the SIM card. This approach works effectively for mobile apps and services consumed primarily on smartphones and tablets. When services require a decoder or viewing card such as satellite television or premium streaming services, the customer is presumed located where the device is installed or where the viewing card is sent.

For situations where these specific presumptions do not apply, businesses can use the general presumption requiring two pieces of non-contradictory evidence from the approved list. The regulation provides an illustrative but non-exhaustive list of acceptable evidence including the billing address provided by the customer, the Internet Protocol address of the device used or any geolocation method, bank details including the location of the bank account used for payment or the billing address held by the customer’s bank, the Mobile Country Code from the customer’s SIM card even when not supplying through mobile networks, the location of the customer’s fixed landline when not used for service delivery, and other commercially relevant information that reasonably indicates customer location.

The requirement for non-contradictory evidence means that the two pieces must point to the same member state. If a customer provides a French billing address and uses a credit card issued by a French bank, these pieces are non-contradictory and establish France as the customer location. However, if the billing address indicates Germany while the credit card is issued by an Italian bank, the evidence is contradictory and additional considerations apply.

Evidence Rebuttal Rights and Tax Authority Limitations

The EU framework grants businesses significant flexibility in how they apply location evidence. Businesses are not required to accept presumptions if they have stronger evidence pointing elsewhere. If you have three pieces of non-contradictory evidence establishing that a customer is located in a different member state than indicated by the applicable presumption, you can rebut that presumption and use the three-piece evidence instead.

For example, imagine a customer connects through a German IP address triggering a location presumption for Germany, but provides a Swedish billing address, uses a Swedish bank account for payment, and the transaction metadata shows Swedish language preferences. The three pieces of evidence pointing to Sweden would allow you to rebut the IP-based presumption and charge Swedish VAT instead of German VAT.

Critically, businesses are not obligated to investigate beyond collected evidence or rebut presumptions. Even if you suspect that two pieces of evidence might not reflect the customer’s actual location, you can rely on the presumption without further investigation. This protection shields businesses from liability for customer fraud or misrepresentation, provided the business applied reasonable evidence collection procedures.

Tax authorities face more restrictions on rebuttal. Unlike businesses that can rebut presumptions based on three pieces of contradictory evidence, tax authorities can only rebut presumptions where they can demonstrate indications of misuse or abuse by the supplier. This might include situations where a business systematically collects evidence in ways designed to artificially establish location in low-tax member states, or where evidence collection procedures are so lax that they cannot reasonably support location determinations.

The VAT Mini One Stop Shop (MOSS) System for Simplified Compliance

The Mini One Stop Shop mechanism, which evolved into the broader One Stop Shop system in July 2021, represents the EU’s most significant simplification for digital services taxation. Without this system, a business selling to customers across all twenty-seven EU member states would need to register for VAT in each state, file periodic returns in each state’s required format and language, make payments to each state’s tax authority, and maintain compliance with each state’s specific invoicing and record-keeping requirements.

The MOSS system eliminates this complexity by allowing businesses to register in their own member state and file a single quarterly return covering all EU sales through a web portal. The business declares total sales by destination member state, applies the appropriate VAT rate for each state, calculates total VAT due per state, and submits one payment to their home tax authority. That authority then distributes the collected VAT to the appropriate member states based on the return information.

For businesses not established in the EU, the non-Union OSS scheme allows registration in any member state of choice, providing a single portal for all EU compliance obligations. This particularly benefits non-EU businesses that might otherwise face registration requirements across multiple member states from their first sale.

The OSS quarterly return must be submitted within twenty days after the end of each calendar quarter. Returns for January through March are due by April twentieth, returns for April through June are due by July twentieth, returns for July through September are due by October twentieth, and returns for October through December are due by January twentieth of the following year. Payment must accompany the return by the same deadline.

Critically, the OSS system does not eliminate the requirement to collect and retain location evidence. Businesses must still determine customer location accurately, collect appropriate evidence, maintain records for ten years, and be prepared to defend their location determinations during audits conducted by member state tax authorities. The OSS simply consolidates the administrative processes of registration, filing, and payment—it does not simplify the underlying compliance obligations around location evidence and tax calculation.

United States Sales Tax Location Requirements

The United States presents perhaps the most complex compliance landscape for digital sales globally, not because any individual state’s rules are particularly sophisticated, but because businesses must simultaneously comply with over ten thousand different tax jurisdictions across fifty states, each with different product taxability rules, varying tax rates at state and local levels, different nexus thresholds, and different location determination requirements.

Economic Nexus and the Post-Wayfair Era

The 2018 Supreme Court decision in South Dakota v. Wayfair, Inc. fundamentally transformed sales tax compliance for all businesses but particularly for digital sellers. Prior to Wayfair, states could only require sales tax collection from businesses with physical presence such as offices, warehouses, or employees within the state. This physical presence standard meant that online-only businesses could sell to customers across the United States while collecting sales tax only in states where they had physical operations.

Wayfair overturned this precedent, allowing states to impose sales tax collection obligations based on economic activity within the state even absent physical presence. Within eighteen months of the decision, every state with a sales tax had implemented economic nexus rules creating collection obligations for remote sellers meeting specified thresholds.

Most states adopted thresholds of either one hundred thousand dollars in sales or two hundred transactions within the state during the current or previous calendar year. However, variations abound. California requires five hundred thousand dollars with no transaction count threshold. Texas uses five hundred thousand dollars in sales. Alabama counts each individual item sold as a separate transaction, dramatically lowering the effective threshold for businesses selling low-priced items. Some states measure thresholds based on the current calendar year, others based on the previous twelve months, and still others based on the current or previous calendar year, whichever creates nexus first.

US State Economic Nexus Thresholds for Digital Sales (2026)

| State | Sales Threshold | Transaction Threshold | Measurement Period |

|---|---|---|---|

| California | $500,000 | None | Prior or current calendar year |

| Texas | $500,000 | None | Preceding 12 months |

| New York | $500,000 | 100 transactions | Immediately preceding 4 quarters |

| Florida | $100,000 | None | Prior calendar year |

| Illinois | $100,000 | 200 transactions | Preceding 12 months |

| Pennsylvania | $100,000 | None | Previous 12 months |

| Ohio | $100,000 | 200 transactions | Current or prior calendar year |

| Georgia | $100,000 | 200 transactions | Current or previous calendar year |

| North Carolina | $100,000 | 200 transactions | Previous or current calendar year |

| Michigan | $100,000 | 200 transactions | Previous calendar year |

Digital Product Taxability Variations Across States

Beyond nexus thresholds, the taxability of digital products varies dramatically across states, creating complexity in determining when sales tax applies at all. Some states tax all digital products as tangible personal property under their existing sales tax statutes. Others have created specific categories for digital goods and services, some of which are taxable while others remain exempt. Still other states maintain that digital products are intangible services and therefore not subject to sales tax designed for tangible goods.

States that broadly tax digital products include South Dakota, which taxes electronically delivered software, music, books, and other digital goods. Vermont taxes prewritten software accessed remotely including SaaS platforms. Washington State taxes digital goods including digital audio works, digital audio-visual works, and digital books, and separately taxes digital automated services and digital codes. Pennsylvania taxes software including software as a service and treats many digital products as taxable.

States with partial taxation create the most complexity. Texas taxes data processing services, which can include some SaaS offerings, but exempts information services, creating difficult line-drawing exercises. Colorado exempts computer software delivered electronically but taxes services related to developing or modifying custom software. Massachusetts taxes software delivered electronically but exempts vendor-hosted software accessed remotely, creating critical distinctions between downloaded programs and cloud-based access. New York taxes software delivered electronically but provides exemptions for software used in certain business processes, requiring detailed product classification.

States that broadly exempt digital products include California, which does not tax software or digital goods unless transferred on tangible media. Florida generally exempts software as a service and digital products. Oregon has no sales tax. New Hampshire has no sales tax. Montana has no sales tax. Alaska has no state sales tax though some local jurisdictions impose local sales taxes. Delaware has no sales tax.

Location Evidence Requirements for US Sales Tax

Unlike the EU’s formalized two-piece evidence requirement, US states generally require businesses to maintain reasonable documentation supporting the customer location used for tax determination. What constitutes reasonable documentation depends on the specific circumstances and type of product sold.

For most digital sales, businesses rely primarily on the billing address provided by the customer during checkout. This billing address determines which state’s tax rate applies and whether the business has nexus requiring collection. Payment processors typically validate billing addresses against credit card issuer records, providing some assurance of accuracy. The IP address from which the customer accessed the service provides secondary evidence supporting the billing address or potentially flagging inconsistencies.

For software as a service and other ongoing subscriptions, the location at which the customer uses the service can become relevant, particularly for business-to-business transactions where the customer might have locations in multiple states. In such cases, businesses should collect information about where the service will be used and apply tax based on that usage location rather than merely the billing address.

Record retention requirements vary by state but typically range from three years to seven years. Texas requires four years. California requires three years but recommends keeping records longer for transactions involving exemption certificates. New York requires three years. Florida requires three years. Most states reserve the right to audit transactions within the statute of limitations period, during which all supporting documentation must be available for examination.

Asia-Pacific Digital Tax Requirements

The Asia-Pacific region has rapidly implemented digital services taxation frameworks, with most major economies now requiring foreign digital service providers to register and collect tax on sales to local consumers. While these frameworks generally follow principles similar to the EU model, each jurisdiction has implemented unique thresholds, evidence requirements, and compliance procedures.

Australia GST on Imported Digital Services

Australia implemented its Goods and Services Tax on imported digital services effective July 1, 2017, making it one of the first jurisdictions outside Europe to require foreign digital service providers to register and collect tax. The ten percent GST applies to telecommunications services, broadcasting services, and electronically supplied services supplied to Australian consumers.

Non-resident businesses must register for GST when their annual sales of digital services to Australian consumers exceed seventy-five thousand Australian dollars. This threshold is measured based on annual turnover, not calendar year, allowing businesses to track on a rolling twelve-month basis. Once the threshold is exceeded, registration is required, and GST must be collected on all subsequent sales.

Australia’s location evidence requirements closely mirror the EU approach, requiring two pieces of non-conflicting evidence to establish that a customer is located in Australia. Acceptable evidence includes the customer’s billing address, the customer’s Internet Protocol address or geolocation information, the location of the customer’s bank or credit card issuer, the country code of the customer’s SIM card, other commercially relevant information that reasonably supports the customer’s location.

The Australian Taxation Office accepts presumptions similar to the EU framework. When services are supplied through a fixed line, the customer is presumed located at that line’s address. When supplied through mobile networks, the SIM card’s mobile country code determines location. When neither presumption applies, businesses use the general two-piece evidence approach.

Australian businesses must file GST returns quarterly unless they have elected monthly filing. The return must be lodged electronically within twenty-eight days after the end of each quarter. Businesses must maintain records supporting their GST calculations, including location evidence, for five years from the date of transaction or when the GST return was lodged, whichever is later.

New Zealand GST on Remote Services

New Zealand implemented its GST on remote services framework effective October 1, 2016, requiring non-resident businesses supplying digital services to New Zealand consumers to register for GST when annual supplies exceed sixty thousand New Zealand dollars. The GST rate is currently fifteen percent, higher than Australia’s ten percent.

Location evidence requirements parallel Australia and the EU, requiring two pieces of non-conflicting information to establish customer location in New Zealand. The acceptable evidence list includes billing address, usual residential address, Internet Protocol address, bank or credit institution address, mobile country code, customer’s own statement of location, other information that reasonably determines the customer is in New Zealand.

New Zealand operates a unique trust-based system for non-resident registration. When registering, businesses declare their expected annual turnover of remote services to New Zealand and begin collecting GST. There is no advance verification or approval process. Businesses file returns every two months and remit collected GST. Inland Revenue conducts post-registration compliance reviews and audits to verify proper collection and remittance.

Records must be retained for seven years, longer than Australia’s five-year requirement. This extended retention period means businesses must maintain detailed location evidence for a substantial period after transactions occur.

Singapore GST on Imported Services

Singapore implemented its GST on imported services effective January 1, 2020, with a unique dual-threshold approach. Non-resident businesses must register when they exceed both a global turnover threshold and a Singapore-specific threshold. Global annual turnover must exceed one million Singapore dollars, and the value of digital services supplied to Singapore customers must exceed one hundred thousand Singapore dollars.

Only when both thresholds are met does the registration obligation arise. This approach targets larger businesses while providing relief to smaller operators who might exceed a single threshold but have minimal Singapore presence.

The current GST rate is nine percent, having increased from eight percent on January 1, 2024. Further increases may occur as Singapore adjusts its tax policy.

Singapore requires businesses to collect sufficient evidence to establish customer location but does not prescribe a specific number of evidence pieces or provide detailed presumption rules like the EU. The guidance indicates businesses should consider billing address, IP address, bank or payment details, SIM card country code, and other relevant information that reasonably establishes Singapore location.

Returns are filed quarterly, due within one month after the quarter end. Businesses must maintain records for five years to support their GST reporting and location determinations.

Japan Consumption Tax on Digital Services

Japan requires foreign businesses supplying digital services to Japanese consumers to register for consumption tax purposes when supplying business-to-consumer digital services regardless of sales volume. There is no registration threshold for business-to-consumer supplies, meaning tax obligations begin with the first sale.

However, Japan provides a registration threshold of ten million yen (approximately ninety thousand US dollars) for the current or preceding calendar year. Businesses below this threshold may elect simplified reporting and compliance procedures.

The consumption tax rate is currently ten percent, comprising a national consumption tax rate of 7.8 percent and local consumption tax rate of 2.2 percent applied to the national tax base.

Japan requires appropriate evidence to support customer location determinations. While not prescribing specific evidence requirements or piece counts, guidance suggests collecting customer address information, IP address location, credit card issuing country, and other relevant indicators of Japanese location.

Returns are filed annually for most foreign suppliers, though businesses can elect monthly or quarterly filing. Annual returns are due by March thirty-first of the following year for calendar year filers. Records must be retained for seven years from the date of the transaction.

South Korea VAT on Digital Services

South Korea implemented VAT on digital services supplied by foreign businesses effective July 1, 2015, making it one of the earliest adopters of destination-based digital taxation. The VAT rate is ten percent, and registration is required for all foreign businesses supplying business-to-consumer digital services to Korean consumers regardless of sales volume. There is no threshold, making South Korea one of the strictest jurisdictions for foreign supplier obligations.

Location evidence requirements focus on verifying that customers are located in South Korea. While specific evidence requirements are not formally codified, businesses typically collect customer address, payment card issuing country, IP geolocation, and customer declarations to establish Korean location.

Returns are filed quarterly, due by the twenty-fifth day of the month following the quarter end. South Korea requires foreign businesses to appoint a tax agent or representative to handle VAT filings and communications with tax authorities, adding cost and complexity compared to jurisdictions allowing direct foreign registration.

Records must be retained for five years, and South Korea conducts regular audits of foreign suppliers to verify compliance with registration and collection obligations.

India GST on Online Information and Database Access or Retrieval Services

India requires foreign suppliers of online information and database access or retrieval services to register for GST and collect eighteen percent GST on all supplies to non-business consumers in India. There is no threshold—registration and collection are required from the first sale to an Indian consumer.

The definition of online information and database access or retrieval services is quite broad, covering most software-as-a-service platforms, digital content subscriptions, cloud storage, online advertising services targeting Indian consumers, and many other digital business models.

Location evidence must demonstrate that the customer is located in India and is not a registered business. Evidence typically includes billing address in India, IP address geolocating to India, payment through Indian financial institutions, and customer declarations of non-business status.

Returns are filed monthly through a simplified online portal specifically designed for foreign suppliers. The return is due by the twentieth of the following month, and payment must be made electronically through the portal.

India requires records to be maintained for six years from the end of the relevant financial year, creating retention obligations similar to other major jurisdictions.

Operational Guide: Collecting and Validating Location Evidence

Understanding regulatory requirements provides the foundation for compliance, but operational success requires implementing systems and processes that collect, validate, store, and manage location evidence at scale. For businesses processing thousands or millions of transactions annually, automation and systematization are not optional—they are the only viable path to compliance.

Categories of Acceptable Location Evidence

Before diving into collection processes, it helps to understand what types of evidence tax authorities across different jurisdictions consider acceptable. While specific requirements vary, most jurisdictions recognize several broad categories of evidence that businesses can rely upon when determining customer location.

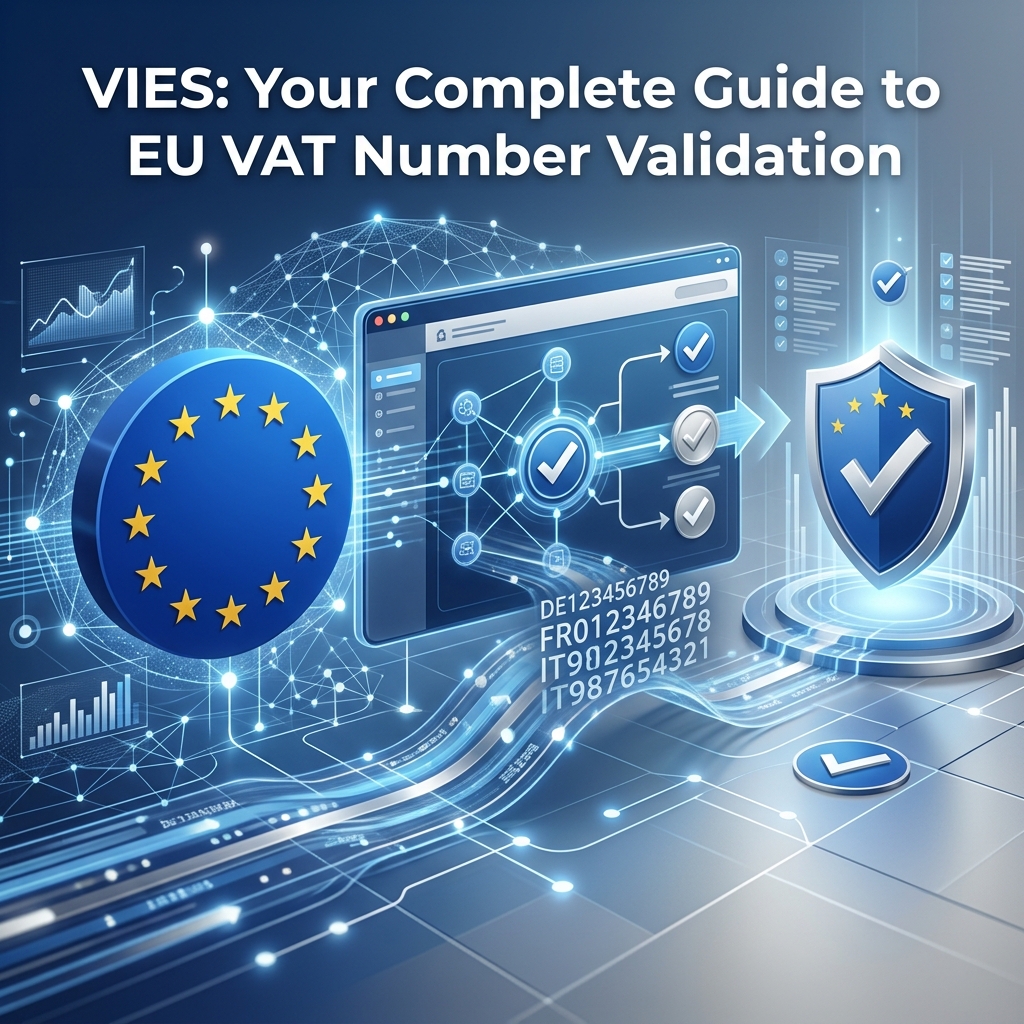

Tax registration numbers and business identifiers represent the single most important and reliable piece of evidence for business-to-business transactions. When a customer provides a valid VAT identification number in the European Union, a GST registration number in Australia or New Zealand, a GST or HST number in Canada, an Australian Business Number, or a resale certificate in the United States, this evidence serves dual critical purposes. First, it conclusively establishes the customer’s status as a registered business entity rather than a consumer, which fundamentally changes the tax treatment in most jurisdictions. Second, in the vast majority of cases, providing a valid business registration number triggers reverse charge mechanisms where the responsibility for assessing and remitting tax shifts from the supplier to the business customer.

The importance of properly validating these tax registration numbers cannot be overstated. The European Union operates the VAT Information Exchange System, commonly known as VIES, which allows businesses to validate VAT numbers in real-time across all twenty-seven member states. When you enter a VAT number into the VIES system, it immediately confirms whether that number is currently valid and active, and it provides the registered company name and address associated with that number. This validation must be performed at the time of each transaction or at minimum on a regular schedule for ongoing customer relationships. Simply collecting a VAT number without validation provides no protection during audits—tax authorities expect businesses to demonstrate that they actively verified the number’s validity and obtained confirmation before applying reverse charge treatment.

Similar validation systems exist in other jurisdictions. Australia provides the Australian Business Number Lookup service where businesses can verify ABN registrations and confirm GST registration status. New Zealand offers online verification of GST registration numbers. Singapore maintains registries of GST-registered businesses. The United States presents more complexity because each state issues separate resale certificates, but businesses should at minimum verify that the certificate document appears legitimate, contains all required information for that particular state, and matches the customer’s registered business information.

The critical error many businesses make is accepting customer self-declarations of business status without requiring and validating actual tax registration numbers. During audits, tax authorities will reclassify these transactions as taxable consumer sales if proper business documentation was not collected and validated, potentially assessing back taxes plus penalties on the full transaction value going back several years. The lesson is clear: for business-to-business transactions, always collect the customer’s tax registration number, always validate it through official channels, and always retain documentation proving that validation occurred at the time of transaction.

Billing addresses represent the most commonly used evidence type for consumer transactions. This is the address the customer provides for billing purposes, and it typically corresponds to the address where their credit card statement or bank statement is sent. Billing addresses have significant practical advantages that explain their widespread use. Customers routinely provide this information as part of the normal checkout process, so collection requires no additional steps or forms. Payment processors including Stripe, PayPal, Braintree, and others perform address verification services where they check the provided billing address against the address on file with the card-issuing bank. When addresses match, this provides reasonable assurance that the customer actually corresponds to that location. When addresses do not match, payment processors typically flag the transaction as higher risk or may decline it entirely, providing built-in validation.

However, billing addresses have limitations that businesses must understand. Some customers maintain billing addresses in one jurisdiction while actually residing in another—expatriates, students studying abroad, or digital nomads often continue using home country credit cards and addresses. More problematically, sophisticated customers seeking to avoid higher tax rates can potentially provide false billing addresses, particularly when using payment methods that do not perform strict address verification. This is why billing addresses should generally be corroborated with at least one additional piece of evidence rather than used in complete isolation, particularly for higher-value transactions where the incentive for misrepresentation is greater.

IP address geolocation offers a technical method of determining the customer’s location based on the Internet Protocol address from which they accessed your service or completed their purchase. Every device connecting to the internet is assigned an IP address by their internet service provider or mobile network, and large commercial databases track which IP addresses correspond to which geographic regions. Modern geolocation databases maintained by companies like MaxMind, IP2Location, and Digital Element achieve country-level accuracy exceeding ninety-nine percent for most IP addresses worldwide. This makes IP geolocation highly reliable for determining whether a customer accessed services from within a particular country for VAT or GST purposes.

The accuracy of IP geolocation decreases when attempting more granular location determinations. City-level accuracy typically ranges from sixty-five to eighty-five percent depending on the specific database, the region being evaluated, and the type of internet connection. For United States sales tax purposes where you need to determine not just the state but potentially the specific city or county to apply the correct local tax rate, IP geolocation provides reasonable state-level accuracy but should be supplemented with other evidence like billing addresses for local jurisdiction determination.

The most significant limitation of IP geolocation is that virtual private network services, proxy servers, and Tor networks allow users to mask their true location by routing connections through servers in other countries. The explosive growth of commercial VPN services means millions of users now routinely appear to connect from countries other than their actual residence. A customer in Australia might use a VPN service routing through Singapore, making their IP address geolocate to Singapore despite their actual Australian location. While this complicates location determination, businesses that collect multiple pieces of evidence remain protected. If that Australian customer provides an Australian billing address and uses an Australian credit card despite the Singapore IP address, the two pieces of customer-provided evidence validated by financial institutions should reasonably control over the VPN-obscured IP location.

Payment method details and banking information provide another category of valuable evidence. Credit and debit cards contain country codes that identify the issuing country, and payment processors can provide this information through their APIs as part of transaction responses. When a customer pays using a credit card issued by a French bank, this suggests the customer has connections to France even if other evidence might point elsewhere. Bank account locations for customers paying via bank transfer or direct debit similarly indicate customer location, as opening bank accounts typically requires proof of residence in that jurisdiction.

Financial institutions’ know-your-customer requirements and identity verification processes make payment method evidence relatively reliable compared to customer-provided information that may not be independently verified. Banks verify customer identities and addresses before issuing payment cards or opening accounts, and they maintain these records subject to regulatory oversight. This institutional validation provides confidence that payment method evidence reflects actual customer circumstances rather than fabricated information.

That said, customers may legitimately maintain payment methods in countries other than their current residence. Expatriates often retain home country credit cards and bank accounts for years after relocating. International businesses may use payment methods from their headquarters country even when purchasing for use in branch locations. These legitimate scenarios mean payment method evidence should be evaluated in context alongside other available evidence rather than treated as definitively determinative by itself.

Mobile Country Codes from SIM cards provide specific evidence particularly valuable for services delivered through or primarily consumed via mobile networks. Every SIM card contains an International Mobile Subscriber Identity which includes a Mobile Country Code identifying the country of the mobile network operator that issued the SIM. For telecommunications services, mobile applications, and other services delivered to mobile devices, the SIM card’s Mobile Country Code provides strong evidence of customer location because customers typically obtain SIM cards in their country of residence and use domestic mobile networks.

Mobile Country Code evidence has particular value for mobile app purchases, in-app subscriptions, mobile streaming services, and telecommunications offerings. When your service knows the customer is accessing through a mobile device, extracting and logging the Mobile Country Code provides reliable location evidence that is difficult for customers to manipulate without physically obtaining a SIM card from a different country.

Physical location evidence applies in specific circumstances where customers must be physically present at a particular location to receive the service. Wi-Fi hot spots in cafes, airports, hotels, and public spaces provide internet access that customers consume at that specific physical location. Internet kiosks and terminals require customers to be physically present at the device. The customer’s physical presence at a known location provides definitive evidence of their location at the time of service delivery.

The European Union explicitly recognizes this through presumptions allowing suppliers to deem customers located where services are physically supplied when the customer’s physical presence is required. This applies not only to fixed locations like internet cafes but also to transportation—when services are supplied on aircraft, ships, or trains, the location is deemed to be the point of departure for the transportation service. This provides clear determination rules for scenarios where pinpointing customer residence would be difficult but physical location at time of service is unambiguous.

Step-by-Step Evidence Collection Process

Effective location evidence collection begins at the earliest point of customer interaction. During account creation or the first purchase, your system should capture the customer’s billing address through the checkout form, IP address of the device accessing your service through server logs, payment method details provided by payment processors, email domain for potential geographic indicators, language preference selected by the customer, and currency preference if offered.

Modern e-commerce platforms and payment processors provide APIs that automatically capture most of this information. Stripe, PayPal, Braintree, and other payment gateways include geographic information in their transaction responses, including the billing address verified against the card issuer’s records, the country of the bank issuing the payment card, the IP address from which the payment was initiated, and risk scores that may indicate location misrepresentation.

For subscription services and ongoing customer relationships, evidence collection should not stop at signup. Periodic revalidation helps ensure that location evidence remains current, particularly for customers who might relocate to different jurisdictions. Best practices suggest revalidating location evidence at least annually for ongoing subscriptions, whenever a customer updates their payment method or billing information, when IP addresses show consistent patterns from a new country over extended periods, and when customers explicitly update their account information including addresses.

Implementing Geolocation Technology for IP Address Evidence

IP address geolocation provides a valuable secondary piece of evidence that can corroborate or flag potential conflicts with customer-provided information. However, geolocation accuracy varies significantly based on the database used, the type of IP address being resolved, and the level of granularity required.

Commercial geolocation databases such as MaxMind GeoIP2, IP2Location, Digital Element NetAcuity, and Neustar IP Intelligence provide country-level accuracy exceeding ninety-nine percent for most IP addresses worldwide. This high accuracy makes them reliable for determining whether a customer is located within a particular country for VAT or GST purposes.

However, accuracy decreases substantially when attempting to determine location at more granular levels. City-level geolocation accuracy typically ranges from sixty-five percent to eighty-five percent depending on the database and region. Address-level geolocation remains unreliable for most IP addresses. For US sales tax purposes where you need to determine state and potentially city or county location, IP geolocation provides reasonable state-level accuracy but should not be relied upon exclusively for local jurisdiction determination.

The proliferation of VPN services, Tor networks, and proxy servers means that some IP addresses will not reflect the user’s actual physical location at all. Commercial VPN services allow users to route their connections through servers in other countries, making it appear they are accessing services from those countries. While this creates challenges for location determination, businesses are generally protected when they collect multiple pieces of evidence. A customer using a VPN might show a German IP address, but if they provide a Swedish billing address and use a Swedish credit card, the two pieces of customer-provided evidence should control over the VPN-obscured IP address.

For high-risk or high-value transactions, businesses can implement additional verification steps. Device fingerprinting examines characteristics of the user’s browser and device to detect inconsistencies or suspicious patterns. Time zone analysis compares the time zone setting on the user’s device against claimed location. Behavioral patterns including typical access times and patterns can indicate whether claimed location aligns with usage behavior. Velocity checks can flag accounts that appear to access services from implausibly distant locations within short time periods.

Handling Conflicting Evidence Scenarios

Real-world commerce frequently generates conflicting location evidence, and businesses must establish clear decision rules for resolving these conflicts consistently and defensibly. The European Union’s requirement for two pieces of non-contradictory evidence provides helpful guidance even for jurisdictions without such formal requirements.

When multiple pieces of evidence agree, location determination is straightforward. French billing address plus French bank plus French IP address clearly indicates a French customer. Apply the appropriate VAT rate and document the evidence.

When evidence conflicts, establish a hierarchy of evidence reliability. Most businesses treat customer-provided billing address validated by payment processors as the most reliable evidence, since financial institutions verify this information and customers face payment processing complications if they provide fraudulent addresses. Payment card issuing country represents another highly reliable indicator, as financial institutions conduct extensive identity verification. IP geolocation provides supporting evidence but ranks lower in the hierarchy due to VPN usage and mobile connectivity that may not reflect permanent residence.

A reasonable decision rule might prioritize in the following order: first, billing address validated by payment processor, second, payment card issuing country from processor, third, IP geolocation from commercial database, and fourth, customer language or currency preferences. When evidence from levels one and two agree, apply that location regardless of conflicting evidence from level three or four. When evidence from levels one and two conflict, conduct additional investigation or verification before processing the transaction.

Document these decision rules formally in your tax compliance procedures. During audits, tax authorities will examine not just whether you collected evidence but whether you applied consistent, reasonable logic to determine customer location. Well-documented procedures demonstrate good faith compliance efforts even when individual determinations might be challenged.

Special Handling for Business-to-Business Transactions

Business-to-business digital sales create different location evidence requirements compared to consumer transactions. In most jurisdictions, business customers self-assess and remit tax through reverse charge mechanisms, relieving suppliers of collection obligations. However, this favorable treatment requires validating that the customer is indeed a business and obtaining their tax registration number.

For European Union transactions, businesses must collect and validate the customer’s VAT number using the VIES VAT Information Exchange System. This online database allows real-time validation of VAT numbers issued across all EU member states. When a valid VAT number is provided, you can apply the reverse charge mechanism and avoid charging VAT, but you must retain documentation showing that you validated the number and received confirmation of its validity.

Best practices include validating VAT numbers at the time of each transaction or at least monthly for ongoing subscriptions, storing screen captures or API responses showing successful validation, requiring business customers to confirm their registered business address, and collecting business names that should match VIES validation results.

For transactions outside the EU, requirements vary by jurisdiction. Australia requires businesses to obtain the customer’s Australian Business Number and verify the customer is GST registered. New Zealand requires obtaining evidence that the customer is registered for GST. Singapore requires confirming the customer is GST registered for business-to-business exemptions to apply. The United States requires obtaining resale certificates or exemption certificates when customers claim business exemptions, with requirements varying significantly by state.

Many businesses make the mistake of accepting customer self-declarations of business status without requiring registration numbers or validation. This exposes businesses to audit risk, as tax authorities may reclassify unvalidated business-to-business transactions as taxable consumer sales, assessing back taxes and penalties on the full transaction value.

Record Retention Architecture and Best Practices

Record retention represents one of the most underestimated compliance challenges for digital businesses. The requirement to maintain detailed, transaction-level location evidence for up to ten years creates substantial data management obligations that many businesses discover only when facing their first audit.

Effective record retention architecture requires several key components. A comprehensive data warehouse must store transaction details including customer identifier, transaction date and time, product or service description, transaction value, tax jurisdiction determined, tax rate applied, tax amount collected, payment method and details, and all pieces of location evidence collected. This warehouse must support efficient retrieval by various criteria including customer, date range, jurisdiction, or transaction identifier.

Location evidence documentation for each transaction should include the billing address as provided, IP address and geolocation result, payment method details including issuing country, validation timestamp and results, decision logic applied when evidence conflicted, and any customer communications relevant to location determination.

Jurisdictional assignment documentation should maintain tax rate applied, jurisdiction determined, applicable exemptions or reduced rates, threshold calculations if relevant, and registration status in the jurisdiction at time of transaction.

The system must maintain metadata about rate changes, showing when tax rates changed in each jurisdiction, which transactions were affected, and documentation supporting the rate applied. This becomes critical during audits when examiners question why different transactions on different dates showed different tax treatments.

Technical implementation should leverage modern cloud data warehouses such as Amazon Redshift, Google BigQuery, Azure Synapse Analytics, or Snowflake Data Cloud. These platforms provide several advantages including virtually unlimited scalability to handle growing transaction volumes, efficient querying capabilities enabling rapid audit response, long-term storage economics optimized for infrequently accessed historical data, and built-in redundancy and disaster recovery protection.

Data should be partitioned intelligently to optimize both storage costs and query performance. A typical partitioning strategy might organize data by transaction year and month, allowing efficient archival of older data to lower-cost storage tiers while maintaining recent data in high-performance storage for active reporting and analysis.

Documentation should include not just raw transaction data but also context about business processes and system configurations at the time of each transaction. When responding to audits examining transactions from three years prior, you need to explain not just what location evidence was collected but which version of which systems were in use, what decision rules were applied, and what regulatory requirements were in force at that time.

Building Your Location Evidence Technology Stack

The complexity and scale of location evidence requirements mean that manual processes fail at even modest transaction volumes. A business processing one hundred transactions daily generates thirty-six thousand transactions annually, each requiring location evidence collection, validation, documentation, and retention. Manual processes cannot keep pace while maintaining the accuracy and consistency compliance demands.

Building an effective location evidence technology stack requires integrating several categories of tools and platforms, each addressing specific aspects of the compliance challenge.

Core Tax Determination and Compliance Platforms

Tax determination engines form the foundation of any compliance technology stack. These platforms maintain databases of tax rates across all relevant jurisdictions, determine applicable rates based on customer location and product characteristics, calculate tax amounts to be charged, and provide APIs for real-time integration with e-commerce and billing systems.

Leading platforms serving digital businesses include Avalara AvaTax, which offers comprehensive coverage of United States sales tax including economic nexus monitoring, product taxability determination, and returns filing services, plus international VAT and GST support. Vertex Cloud provides global indirect tax determination covering VAT, GST, and sales tax with strong support for complex product classifications and multi-jurisdictional businesses. TaxJar, now part of Stripe, specializes in e-commerce sales tax with particularly strong United States state coverage, economic nexus tracking, and integration with major e-commerce platforms. Sovos offers global tax determination with particular strength in VAT compliance and electronic invoicing requirements. Thomson Reuters ONESOURCE Determination provides enterprise-scale tax determination with robust reporting and audit support capabilities.

These platforms typically charge based on transaction volume processed, with pricing tiers starting around one hundred dollars monthly for small businesses processing thousands of transactions and scaling to thousands of dollars monthly for enterprise customers processing millions of transactions.

When evaluating platforms, assess jurisdiction coverage to ensure the platform supports all locations where you currently operate or plan to expand. Examine product classification capabilities to verify the platform can correctly determine taxability for your specific products. Evaluate API quality and documentation to ensure smooth integration with your existing systems. Consider economic nexus monitoring to get alerts when approaching registration thresholds in new jurisdictions. Look for threshold tracking that monitors multiple threshold types across different jurisdictions. Assess evidence collection capabilities to ensure automatic capture and storage of location evidence meeting regulatory requirements. Review historical rate accuracy to ensure the platform maintains accurate records of rate changes over time for audit support. Examine reporting and analytics to support internal compliance review and audit response.

Geolocation Services and IP Intelligence

While tax determination platforms often include basic geolocation capabilities, businesses handling high volumes or high-risk transactions may benefit from dedicated geolocation services providing enhanced accuracy and additional context about IP addresses.

MaxMind GeoIP2 offers industry-leading accuracy for country-level geolocation, with databases updated weekly to reflect IP address reassignments and network changes. The service provides both database downloads for on-premise integration and web services for real-time lookup. Pricing starts around two hundred dollars annually for database subscriptions.

IP2Location provides similar capabilities with competitive accuracy and several pricing tiers based on database granularity and update frequency. Their offerings include specialized databases for detecting proxy and VPN usage, helping identify when IP addresses may not reflect actual customer location.

Digital Element NetAcuity targets enterprise customers with requirements for high accuracy and low latency at scale. Their service is particularly strong for applications requiring city-level or neighborhood-level accuracy.

IPQualityScore combines geolocation with fraud detection, providing proxy detection, VPN detection, Tor exit node identification, connection type classification, and abuse velocity tracking. This integration helps businesses identify suspicious transactions where location evidence may be manipulated.

For most digital businesses, the geolocation services included in major tax platforms suffice for basic compliance. Dedicated geolocation services become valuable when high transaction values justify additional verification costs, fraud risk is elevated requiring enhanced detection, business models depend on accurate location determination beyond tax compliance, or when serving jurisdictions with particularly aggressive enforcement and audit practices.

Payment Processor Integration and Data Extraction

Payment processors provide critical location evidence through their transaction data, but extracting and storing this information requires proper integration and data pipeline architecture.

Stripe provides comprehensive transaction metadata through its API including billing address verification results, card country of issuance, IP address of transaction initiation, risk scores indicating potential fraud, and three-dimensional secure authentication results. Stripe’s API is well-documented and supports webhooks for automated data extraction as transactions occur.

PayPal similarly provides transaction location data including billing address, country of account registration, IP address, and payer verification status. PayPal’s Instant Payment Notification system enables real-time data extraction.

Braintree, Square, Adyen, and other processors provide similar capabilities with varying data structures and integration methods. Businesses should implement data extraction pipelines that automatically capture all available location evidence from payment processor responses and store it in their compliance data warehouse.

Key implementation considerations include capturing raw API responses from payment processors for documentation purposes, extracting structured location fields for evidence validation, storing transaction timestamps from payment processor records, documenting processor-side validation results, and implementing webhook handlers for asynchronous transaction updates.

Automated Evidence Collection and Validation Systems

Beyond tax platforms and payment processors, businesses benefit from implementing custom evidence collection and validation logic that orchestrates information from multiple sources and applies business-specific decision rules.

A typical evidence collection system architecture includes a checkout integration layer that captures customer-provided information during purchase, a payment processor connector that extracts evidence from transaction responses, a geolocation service integration that resolves IP addresses to locations, an evidence validation engine that checks consistency across evidence pieces, a decision engine that applies business rules to resolve conflicts, and a documentation generator that creates audit-ready records of evidence and decisions.

This system should operate in real-time during checkout, determining tax obligation, calculating amounts, and completing the transaction seamlessly while simultaneously documenting all evidence and decisions for compliance purposes.

For subscription businesses, the evidence collection system should also include scheduled jobs that periodically revalidate location evidence for ongoing customer relationships, triggering location updates when evidence changes and adjusting future billing accordingly.

The Role of AI and Machine Learning in Location Evidence Management

Artificial intelligence and machine learning are increasingly valuable for managing location evidence at scale, identifying patterns that indicate potential issues, and continuously improving evidence collection processes.

Automated product classification using natural language processing can analyze product descriptions, categorize them according to tax rules across jurisdictions, and maintain accurate classifications even as product catalogs expand. This reduces manual classification work and improves consistency.

Anomaly detection algorithms can identify transactions where evidence patterns suggest potential fraud or error. Machine learning models trained on historical transaction data can flag unusual combinations such as billing addresses in one country with consistently different IP countries, payment methods from different countries than billing addresses, transaction patterns that differ significantly from established customer behavior, or multiple accounts sharing suspicious similarities.

Predictive compliance alerts can forecast when businesses will exceed registration thresholds in various jurisdictions. By analyzing historical sales patterns, growth rates, and seasonal variations, machine learning models can predict with reasonable accuracy when a business will trigger nexus in specific states or countries, providing lead time to prepare for registration and compliance.

Natural language processing systems can monitor regulatory changes by scanning tax authority websites, regulatory databases, and legal publications for relevant updates. These systems can extract key information, classify changes by jurisdiction and topic, and alert compliance teams to updates requiring system or process changes.

Automated audit response capabilities can compile evidence and documentation for specific audit requests. Rather than manually searching through records, AI-powered systems can interpret audit information requests, identify relevant transactions, extract applicable evidence and supporting documentation, and generate comprehensive response packages.

Building Versus Buying: Strategic Considerations for Technology Investment

Many businesses face the question of whether to build custom compliance technology or purchase commercial platforms. This decision should consider both immediate costs and long-term total cost of ownership.

Commercial platforms offer several compelling advantages including immediate access to comprehensive tax rate databases maintained by specialized teams, continuous updates reflecting regulatory changes without internal development work, established integrations with major e-commerce and billing platforms, and vendor support for implementation questions and compliance guidance.

The disadvantages of commercial platforms include ongoing subscription costs that may become substantial at scale, potential vendor lock-in creating switching costs, limited customization for unique business requirements, and dependency on vendor responsiveness for feature requests and bug fixes.

Custom development provides maximum flexibility to address unique requirements, complete control over system architecture and data models, freedom from vendor lock-in and ongoing subscriptions, and ability to integrate deeply with proprietary business systems.

However, custom development imposes substantial costs including ongoing maintenance of tax rate databases across jurisdictions, continuous monitoring of regulatory changes requiring system updates, opportunity cost of engineering resources focused on compliance rather than core product, risk of errors in tax determination logic that commercial platforms have tested extensively, and delayed access to new features that vendors provide to all customers simultaneously.

For most small and mid-sized digital businesses, commercial platforms offer superior economics and lower risk. The specialized expertise required to maintain accurate tax rates, the continuous compliance monitoring burden, and the costs of errors make purchasing established platforms prudent.

Large enterprises with substantial engineering resources and highly specialized requirements may justify custom development, but even these organizations increasingly prefer commercial platforms for core tax determination while building custom integration layers connecting tax compliance into their specific business processes.

A hybrid approach often works best: leverage commercial platforms for tax determination and rate management while building custom systems for evidence collection, validation, and storage tailored to specific business needs and risk tolerances.

Future-Proofing: Preparing for Evolving Requirements

Tax compliance requirements for digital sales continue evolving rapidly as jurisdictions refine their systems, expand enforcement capabilities, and respond to new business models. Businesses must design compliance systems not merely for today’s requirements but with flexibility to adapt to tomorrow’s regulatory changes.

Emerging Trends Reshaping Digital Tax Compliance

Several clear trends are reshaping the digital tax landscape globally, and businesses should prepare systems to accommodate these changes.

Expanded scope of taxable digital services: Historical distinctions between different types of digital services are eroding. Services involving significant human interaction, previously excluded from electronically supplied services definitions, increasingly fall within scope as jurisdictions recognize that meaningful human involvement can coexist with automated delivery. Live instructor-led webinars, coaching services delivered through digital platforms, and hybrid automated-plus-human services all face expanding taxation.

Declining or eliminated registration thresholds: Early digital services tax regimes often included substantial thresholds focusing enforcement on larger players. As tax authorities gain experience and improve systems, many are reducing or eliminating these thresholds. Countries including Russia, India, South Korea, and Saudi Arabia now require registration from the first sale, eliminating safe harbors that thresholds previously provided. This trend will likely continue as jurisdictions seek to capture revenue from smaller suppliers.

Platform and marketplace taxation shifts: Initially, digital platforms like app stores and content marketplaces bore primary tax collection responsibility. However, jurisdictions increasingly require individual sellers using platforms to register and report directly, or require platforms to collect tax on behalf of sellers. The European Union’s platform economy VAT changes exemplify this shift. Businesses selling through platforms should anticipate increased direct compliance obligations even when platforms collect tax.

Real-time reporting and electronic invoicing: Many jurisdictions are implementing real-time or near-real-time transaction reporting requirements. Rather than periodic returns summarizing past transactions, these systems require businesses to report each transaction or invoice shortly after occurrence. Italy, Hungary, Poland, France, and numerous other countries have implemented or announced electronic invoicing mandates. This trend demands more sophisticated system integration and automation than traditional periodic reporting.

Enhanced information exchange between tax authorities: The OECD’s Common Reporting Standard and similar initiatives enable extensive information sharing between tax authorities globally. This reduces opportunities for non-compliance through jurisdictional arbitrage and increases likelihood that violations will be detected even when individual jurisdictions have limited enforcement resources.

AI-powered enforcement and audit selection: Tax authorities worldwide are deploying artificial intelligence and advanced analytics to identify non-compliant businesses, detect fraud patterns, and select audit targets. Greece’s Independent Authority for Public Revenue uses AI analyzing both structured financial data and unstructured information from social media and public sources. Sweden’s Tax Agency employs machine learning for risk assessment and audit selection. This trend means businesses should expect more sophisticated enforcement and higher detection rates for errors or omissions.

Standardization of evidence requirements: While jurisdictions currently employ varying location evidence requirements, trends suggest potential standardization around the EU’s two-piece evidence approach. Organizations including the OECD are developing guidelines for digital services taxation that may promote convergence. Businesses designing evidence collection systems should anticipate that additional jurisdictions will adopt formalized evidence requirements similar to the EU model.

Architectural Principles for Future-Proof Compliance Systems

Given these evolving requirements, businesses should design compliance technology and processes following specific architectural principles that enable adaptation to regulatory changes.

Modular architecture with loosely coupled components: Design systems where tax determination engines, evidence collection modules, filing mechanisms, and data storage operate as distinct components communicating through well-defined APIs. This enables replacing or upgrading specific components as requirements change without redesigning entire systems.

Configuration-driven behavior rather than hard-coded logic: Implement systems that permit configuring new evidence types, tax rates, jurisdictions, or validation rules through administrative interfaces rather than requiring software development. When a new jurisdiction implements location evidence requirements, configuration changes should suffice rather than requiring code modifications and testing cycles.

Comprehensive audit trails logging all decisions: Store not just transaction outcomes but complete decision processes including evidence collected, validation results, decision logic applied, rules evaluated, rates determined, and any manual overrides or interventions. This documentation proves essential for audit defense and for troubleshooting when apparent errors are discovered.

Scalable data architecture supporting growth: Design data systems that accommodate both growing transaction volumes and extended retention requirements. Cloud-based solutions with elastic scaling capabilities often provide better economics than fixed-capacity infrastructure. Implement data lifecycle policies that automatically move aging data to lower-cost storage while maintaining accessibility.

Regular compliance reviews embedded in business processes: Rather than reactive compliance triggered by audit notices, implement proactive periodic reviews assessing compliance across all active jurisdictions, validating system functionality, identifying threshold approaching in new jurisdictions, reviewing recent regulatory changes for applicability, and testing evidence collection for accuracy and completeness.

Strategic advisor relationships for expert guidance: While technology provides operational capabilities, interpreting complex regulations and planning strategic responses benefit from human expertise. Cultivate relationships with tax advisors specializing in digital services taxation who can provide jurisdiction-specific guidance, early warning of regulatory changes, interpretation of ambiguous requirements, and strategic planning for market expansion.

Continuous staff training and knowledge development: Invest in training teams on both operational requirements and underlying regulatory principles. As regulations change, trained staff can make appropriate implementation decisions rather than blindly following outdated procedures. Cross-train multiple team members on compliance processes to avoid single points of failure.

Why Specialized Advisors Like LookupTax Provide Critical Value

The complexity of location evidence requirements and digital tax compliance more broadly creates natural opportunities for specialized service providers. Organizations like LookupTax that focus specifically on indirect taxation including VAT, GST, and sales tax across global markets bring several distinct advantages that businesses navigating this landscape cannot easily replicate internally.

Deep Specialized Expertise Across Jurisdictions