Andorra NRT Tax Number Guide

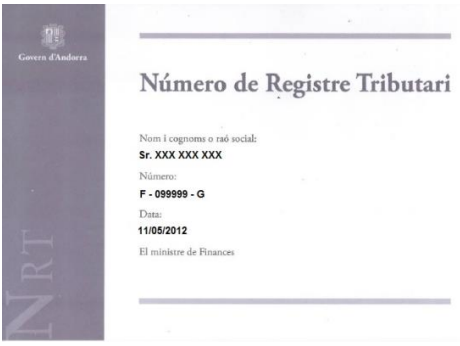

Número de Registre Tributari (NRT)

The Departament de Tributs i de Fronteres (Department of Taxes and Borders) issues a Número de Registre Tributari (NRT) to every legal entity, individual, and unincorporated body that carries out taxable activities in the Principality of Andorra — regardless of their residency status. The NRT functions as Andorra's primary tax identification number and appears on all IGI (Impost General Indirecte) declarations, corporate tax returns, customs documents, and commercial invoices.

The NRT is permanent: it does not change unless there is a modification in legal structure or nationality, as specified in Article 16 of the implementing Regulations.

NRT for Residents — NIA with "F" Prefix

For natural persons residing in Andorra, the NRT is the Número d'Identificació Administrativa (NIA) governed by Law 8/2007 of 17 May. The NIA for residents is prefixed with the letter F (Article 14 of the Regulations). Andorran residents receive this number automatically upon registration with the immigration and tax administration.

NRT for Non-Residents — NIA with "E" Prefix

Natural persons who are not resident in Andorra but have tax obligations there are assigned an NIA preceded by the letter E (Article 15 of the Regulations). Non-resident individuals must apply to the Departament de Tributs i de Fronteres directly, typically alongside their first taxable transaction or registration for IGI.

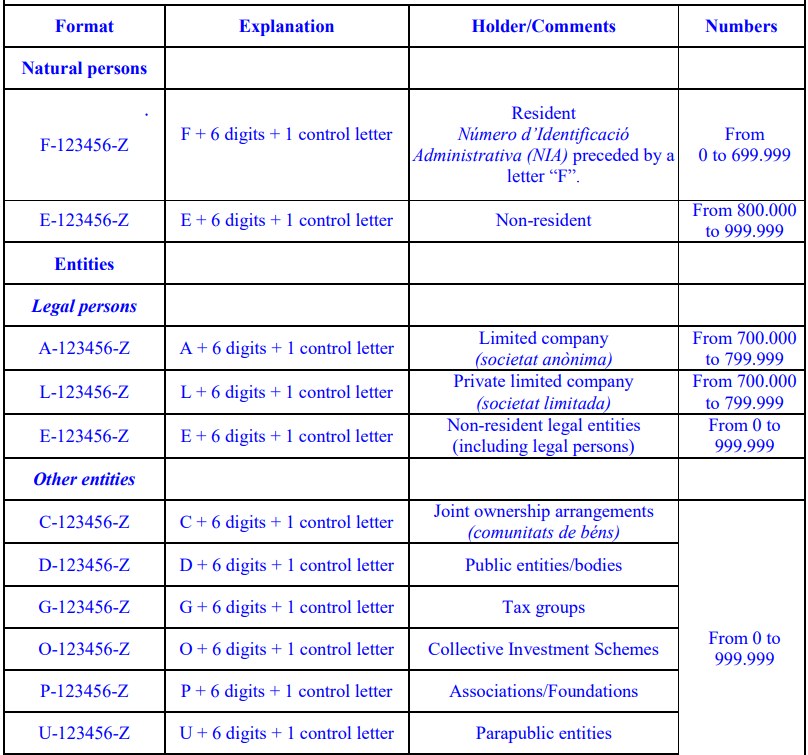

Format Specification

Every NRT follows a fixed 8-character structure:

[PREFIX LETTER] - [6 DIGITS] - [CONTROL LETTER]

Example: L-123456-A

Prefix Letter — Entity Type Codes

| Prefix | Entity Type |

|---|---|

| F | Resident natural person (NIA holder) |

| E | Non-resident natural person |

| A | Societat Anònima — joint-stock company (SA) |

| L | Societat de Responsabilitat Limitada — limited liability company (SL) |

| C | Cooperative |

| D | Foundation or association |

| G | Government entity |

| O | Other non-commercial bodies |

| P | Professional partnership |

| U | Temporary business group (UTE) |

Control Letter

The final character is a checksum letter calculated from the 6-digit numeric portion. Software libraries such as python-stdnum implement format and compact validation for NRTs; as of version 1.17, the library validates length and structure but notes that checksum verification of the control letter is not performed programmatically — meaning format-level validation alone does not guarantee an NRT is genuinely registered.

Regex Pattern

A format-only regex for NRT validation:

^[A-Z]-\d{6}-[A-Z]$

This matches the letter–6 digits–letter structure. Separators (hyphens or spaces) are optional in compact form: L123456A.

Format Reference Images

|

| NRT Format |

|

| NRT |

Issuing Authority

Departament de Tributs i de Fronteres Govern d'Andorra Portal: www.govern.ad / www.e-tramits.ad

The department handles NRT issuance, IGI registration, corporate income tax, and customs declarations. NRT applications can be submitted electronically via the e-tramits portal or in person at the department's offices in Andorra la Vella.

IGI (Impost General Indirecte) — Andorra's Indirect Tax

The IGI is Andorra's equivalent of VAT. Key rates:

| Category | Rate |

|---|---|

| Standard goods and services | 4.5% |

| Digital and electronic services | 4.5% |

| Reduced (food, medicine) | 1% |

| Exempt (education, health) | 0% |

The €40,000 annual turnover threshold determines mandatory IGI registration for both resident businesses and non-resident digital service providers. Below this threshold, registration is optional but permitted.

Cross-Border and Double Taxation Context

Andorra has signed double taxation agreements (DTAs) with Spain and France, both of which entered into force in January 2016. These treaties establish which country has taxing rights over different categories of income for individuals who split their time between Andorra and a bordering country. Unlike Spain's DTAs with France and Portugal (which contain specific cross-border worker provisions), the Andorra–Spain agreement does not have dedicated frontier worker provisions, meaning general residency rules apply.

Frequently Asked Questions

Can a foreign company with an NRT open an Andorran bank account without a resident director?

In practice, no — or at best with extreme difficulty. Although an NRT is issued upon incorporation, all three Andorran banks (Andbank, Creand, Morabank) apply strict KYC/AML compliance aligned with EU anti-money laundering standards. Their current policy makes it very difficult and often impossible for a foreign-owned company to open an account unless at least one shareholder or director holds an Andorran residency permit. Purely non-resident NRT entities routinely face rejection or multi-month delays. Engaging a local gestoria (administrative agent) before incorporation — rather than after — is the most reliable way to navigate these onboarding requirements. [1] [2]

Does holding an Andorran passive residency permit make me a fiscal resident for tax purposes?

Not automatically, and this distinction catches many newcomers. Andorra's passive residency (residència sense activitat lucrativa) requires only 90 days of physical presence per year, but fiscal (tax) residency requires either 183 days of actual presence in Andorra or having your principal center of economic and vital interests there. If you hold the permit but spend most of the year in Spain or France, those countries' tax authorities — which maintain dedicated units monitoring residents who claim to have relocated — may assert you remain tax-resident there under domestic rules or the relevant double-taxation agreement. The 90-to-183 day gap is a grey zone where your country of origin may demand taxes plus surcharges. [1] [2]

What do the prefix letters on an Andorran NRT actually mean, and why does my counterparty's prefix matter for invoice validation?

Every NRT follows the format X-999999-Y, where the first letter encodes the taxpayer category: F = resident natural person, E = non-resident natural person, A = joint-stock company (SA), L = limited liability company (SL), and other letters (C, D, G, O, P, U) cover cooperatives, foundations, government entities, and similar bodies. Andorra has no public real-time verification portal equivalent to EU VIES, so a mismatch between the NRT prefix and the entity type stated on an invoice typically surfaces only during a Departament de Tributs i de Fronteres audit. Issuing or accepting an invoice with an incorrect or mismatched prefix can trigger invoice rejection and IGI compliance issues. [1] [2]

Is Andorra still a banking-secrecy jurisdiction, and will my Andorran account be reported to my home tax authority?

No. Andorra fully abandoned banking secrecy under Law 19/2016, which entered into force on 1 January 2017 and implemented the OECD Common Reporting Standard (CRS) domestically. Since September 2018, Andorran banks have transmitted account-holder data — balances, interest, dividends, and gross proceeds — annually to the Ministry of Finance, which forwards it to the tax authorities of each account holder's country of fiscal residence. As of 2024, Andorra exchanges information automatically with all 28 EU member states under the 2016 Andorra-EU AEOI Protocol, plus an expanding list of over 73 jurisdictions via the OECD Multilateral Competent Authority Agreement. Non-disclosure of an Andorran account in your home-country tax return after 2017 constitutes a reportable omission. [1] [2]

When must a non-Andorran business register for IGI and obtain an NRT for digital or remote services sold to Andorran customers?

A non-resident business providing digital or electronic services to private individuals (B2C) in Andorra must register for IGI and obtain an NRT once annual turnover from Andorran customers exceeds €40,000. Below this threshold, no registration is required. The IGI rate on digital services is 4.5% — significantly lower than EU VAT rates. For B2B sales where the Andorran customer already holds an NRT, the reverse-charge mechanism applies: the Andorran business self-assesses the IGI and no registration obligation falls on the foreign supplier for those transactions. Non-established obligors that cross the threshold must appoint a tax representative resident in Andorra before filing their first declaration. [1] [2]

Related Resources

- France TIN number guide — neighboring country tax ID structure

- Liechtenstein TIN number guide — another small European microstate

- San Marino TIN number guide — comparable microstate tax framework

- How to verify EU VAT numbers (VIES) — why Andorra has no equivalent portal

- Worldwide VAT and tax ID name directory

How Lookuptax can help you ?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.