Indonesia NPWP Tax ID Guide — Format, NIK Integration & Compliance

This post is also available in: Español|中文|Deutsch|Português|Français

Nomor Pokok Wajib Pajak (NPWP)

Indonesia's Tax Identification Number is the Nomor Pokok Wajib Pajak (NPWP), administered by the Directorate General of Taxes (Direktorat Jenderal Pajak — DJP) under the Ministry of Finance. The NPWP is used for all tax filing, invoicing, withholding, and registration activities in the Indonesian tax system. Effective July 14, 2022, Indonesia began a phased transition from the legacy 15-digit NPWP to a unified 16-digit system that integrates with the national population database — a reform that reached its operational endpoint on July 1, 2024, when the 15-digit format was retired from all DJP administrative services.

The NPWP framework covers three taxpayer categories, each with its own identifier structure:

- Indonesian resident individuals — their NPWP is now identical to the 16-digit NIK (Nomor Induk Kependudukan) on their national identity card (KTP). No separate NPWP card is issued; the KTP itself serves as proof of taxpayer identity.

- Non-resident individuals, corporate taxpayers, and government agencies — assigned a 16-digit NPWP by the DJP. Entities registered before July 14, 2022 received their 16-digit NPWP automatically by prepending "0" to the existing 15-digit number.

- Branch-status taxpayers — identified from January 1, 2024 onwards by a NITKU (Nomor Identitas Tempat Kegiatan Usaha), a 22-digit code derived from the head office's NPWP, not a standalone NPWP.

Registration is mandatory under Article 2(1) of the General Provisions and Tax Procedures Law (Undang-Undang Ketentuan Umum dan Tata Cara Perpajakan — UU KUP) once a taxpayer meets both the subjective criteria (legal capacity as a person or entity) and the objective criteria (taxable income or activity). The DJP may also issue an NPWP ex officio where a taxpayer qualifies but has not self-registered.

Format

Resident individual taxpayers (Indonesian citizens and foreign nationals with Indonesia permanent residency status)

The NPWP equals the 16-digit NIK printed on the KTP. Format: NNNNNNNNNNNNNNNN (16 numerals). The NIK encodes birth-date and registration-office codes in specific positions and is validated against the Dukcapil (Directorate General of Population and Civil Registration) database.

|  |

| NPWP on the National Identity Card (KTP) | |

Non-resident individuals, corporate taxpayers, and government agencies

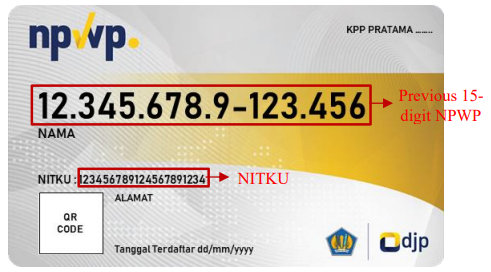

Format: NNNNNNNNNNNNNNNN (16 numerals). For entities registered before July 14, 2022, the 16-digit NPWP = 0 + original 15-digit NPWP. The 15-digit legacy format was structured as XX.XXX.XXX.X-XXX.XXX (two-digit registration-office code, six-digit serial, one check digit, three-digit KPP code, three-digit branch indicator).

|  |

| NPWP card for non-resident individuals and entities | |

Branch-status taxpayers (NITKU)

From January 1, 2024, each branch location is assigned a NITKU: [16-digit head-office NPWP][000001] (sequential 6-digit suffix; the head office itself carries 000000). NITKU is a location identifier only — all filing and payment obligations remain under the head-office NPWP.

|

| Nomor Identitas Tempat Kegiatan Usaha (NITKU) on NPWP card |

NIK–NPWP Matching Requirement

Indonesian resident individuals who held an older NPWP were required to complete the NIK–NPWP pemadanan (matching/activation) by December 31, 2024. Individuals who did not complete matching are treated by the DJP as not having a valid NPWP, and their payers (employers, clients) must apply a 20% surcharge on top of the standard withholding tax rates under Articles 21, 22, and 23 of the Income Tax Law. Matching is handled automatically where DJP data aligned with Dukcapil data; where discrepancies existed (address mismatch, name spelling differences), taxpayers needed to update their data at the relevant KPP (Tax Service Office) or via the Coretax DJP portal.

How to Verify an NPWP

The official NPWP lookup tool is at ereg.pajak.go.id/ceknpwp for the legacy e-Registration system. From January 2025, the DJP's new Coretax system (coretaxdjp.pajak.go.id) has been the primary platform for all taxpayer administration, including NPWP status checks. The lookup returns the taxpayer's name, NPWP/NIK, and active or Non-Effective (NE) status. An NE status means the NPWP is suspended in banking and e-Faktur systems until reactivated.

Married Women and Separate Taxation

By default, a married woman uses her husband's NPWP for joint tax filing. She may apply for a separate NPWP — enabling independent taxation — if she has a judge's decree of legal separation, an income/assets separation agreement, or submits a written request to exercise tax rights independently. Separate-NPWP elections are irrevocable within a tax year.

PMSE VAT (Digital Services Tax) for Foreign Providers

Indonesia imposes a 12% VAT on digital goods and services sold by foreign providers to Indonesian consumers (B2C) under the PMSE (Perdagangan Melalui Sistem Elektronik — Electronic Trading System Commerce) regime, effective April 1, 2020. Foreign providers must register as a PMSE VAT Collector (Pemungut PPN PMSE) once they exceed either of two annual thresholds: transaction value with Indonesian users above IDR 600 million, or total transactions/users above 12,000. Registration is typically initiated by a DJP appointment letter, but proactive registration is available via digitaltax.pajak.go.id. Once appointed, a simplified NPWP is issued; no Indonesian legal presence is required. The PMSE regime covers B2C sales only — B2B sales are subject to the standard reverse-charge mechanism. As of late 2025, over 254 providers have been appointed, including Netflix, Spotify, Google, and OpenAI. For regional context, similar digital services tax regimes apply in Malaysia and Singapore.

e-Faktur and the Coretax Transition

Indonesia's mandatory electronic invoicing system, e-Faktur, requires VAT-registered businesses (PKP — Pengusaha Kena Pajak) to issue tax invoices through the DJP's e-Faktur desktop application (version 4.0 from July 20, 2024) or the e-Faktur Web Base. Each invoice must include the buyer's valid 16-digit NPWP or NIK. Common rejection error codes include:

- ETAXSERVICE-20015: Buyer's NPWP not found in the DJP master database or has been revoked.

- ETAXSERVICE-40002: NPWP

000.000.000.0-000.000used in a context where the buyer intends to credit the input VAT (only permitted for final consumers who will not claim input VAT). - ETAX-40001: System error during the Coretax transition period.

From January 1, 2025, the DJP launched the Coretax system to replace DJP Online, consolidating NPWP registration, tax filing, e-Faktur, and e-Bupot into one platform. The rollout experienced documented instability — the DJP acknowledged at least 22 system issues, including NIK/NPWP data mismatch errors for foreign nationals holding certain passports, OTP delivery failures, and facial-verification errors for digital certificates. Per DJP Decree KEP-54/PJ/2025, the legacy system remains accessible in parallel until Coretax is fully stable.

For a broader ASEAN compliance comparison, see the Vietnam MST guide and the worldwide tax rates reference.

How Lookuptax can help you in VAT validation?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.

Frequently Asked Questions

My Indonesian partner sent me a 15-digit NPWP — is it still valid for invoices and contracts?

The 15-digit format was retired from all DJP administrative services on July 1, 2024. All tax services now require either the 16-digit NPWP (for non-resident individuals, companies, and government bodies) or the NIK (for Indonesian resident individuals). For resident individuals, the NIK is the NPWP — no separate number exists. For entities and non-residents registered before July 14, 2022, the 16-digit NPWP is the old 15-digit number with "0" prepended. If a counterparty still quotes a 15-digit number, ask for the full 16-digit version or their NIK; the 15-digit form triggers ETAXSERVICE errors in e-Faktur and is rejected in DJP systems. [1] [2]

As a foreign national working in Indonesia, when am I legally required to register for an NPWP?

NPWP registration is mandatory once you meet either a subjective or objective tax criterion. The most common trigger is the 183-day rule: more than 183 cumulative days of presence in Indonesia within any rolling 12-month period makes you a resident taxpayer. A second, earlier trigger is intent to reside: holding a KITAS (Limited Stay Permit), a VITAS valid for more than 183 days, or an employment contract exceeding 183 days is treated as evidence of intent, obligating registration even before day 183 is reached. Without a valid NPWP, your employer must apply a 20% surcharge on top of the standard Article 21 income tax withholding rate. Note that some DJP offices inconsistently refuse applications from foreigners who cannot demonstrate Indonesian-sourced income — if rejected, escalate to the regional DJP office (Kanwil) or apply via the Coretax portal. [3] [4]

My company pays royalties to a foreign licensor — why is 20% withheld even though there is a tax treaty?

Indonesia applies a default 20% Article 26 (PPh 26) withholding tax on royalties, interest, dividends, and service fees paid to non-residents. The treaty-reduced rate is not automatic — it applies only if the foreign recipient submits a valid Certificate of Domicile (SKD WPLN, also known as the DGT Form) before or at the time of payment. The DGT Form details must be entered into the e-SKD menu on pajak.go.id, generating a receipt that must be attached to the Article 23/26 withholding tax return (e-Bupot), due by the 20th of the following month. If the DGT Form is missing or submitted late, the full 20% applies retroactively — the non-resident must file a separate overpayment claim; the Indonesian payer cannot self-correct. Indonesia maintains tax treaties with over 70 countries; treaty rates vary by country and income type. [5] [6]

My foreign SaaS company has Indonesian customers — do I need to register for VAT (PPN) and get an NPWP?

Foreign digital service providers that exceed either of two thresholds must register as a PMSE VAT Collector: (1) transaction value with Indonesian users above IDR 600 million per year (or IDR 50 million per month), or (2) more than 12,000 transactions or users per year. The DJP typically issues a formal appointment letter, but proactive registration is available at digitaltax.pajak.go.id. Once appointed, you collect and remit 12% PPN on B2C sales to Indonesian users; no input-VAT deductions apply. A simplified NPWP is assigned for this purpose — no local legal presence or physical office is required. The PMSE scheme covers B2C only; B2B invoices to Indonesian PKP businesses use the domestic reverse-charge mechanism instead. [7] [8]

We operate branch offices in Indonesia — what happened to the branch NPWP, and what is NITKU?

Branch-level NPWPs were abolished effective January 1, 2024. Each branch location is now identified by a NITKU (Nomor Identitas Tempat Kegiatan Usaha), a 22-digit code: the head office's 16-digit NPWP plus a 6-digit sequential suffix (000001, 000002, etc.; the head office itself uses 000000). NITKU is required in all DJP administrative submissions and in e-Faktur tax invoices where a branch is the issuing or receiving location. Branches that had an old branch NPWP before December 31, 2023 were automatically assigned a NITKU during the transition; branches opened from January 1, 2024 must obtain a NITKU by updating taxpayer data at the relevant KPP. All filing and payment obligations remain centralised at the head-office NPWP — NITKU is a location identifier only, not a separate tax entity. [9] [10]

My NPWP shows "Non-Effective" (NE) status — why is my bank blocking my credit application?

An NPWP flagged as Non-Effective (WP NE) is invalid in banking applications, including business credit and KUR (government micro-lending). NE status is assigned automatically by the DJP when a taxpayer fails to file an Annual Tax Return (SPT Tahunan) for two consecutive years, or submits a written request for deactivation. The fastest reactivation path is to file any outstanding SPT — this automatically restores Active status in DJP systems. Alternatively, submit a reactivation request through the Coretax DJP portal (Portal Saya > Perubahan Status) with supporting documents. NE reactivation typically processes within one working day at the KPP once all outstanding obligations are cleared. Taxpayers in NE status are still subject to the 20% surcharge penalty on withholding tax transactions until the status is restored. [11] [12]

My NIK-to-NPWP matching keeps failing with a data-mismatch error on the DJP portal — what causes this?

NIK validation failures in the DJP/Coretax system occur when the data in the DJP's taxpayer register does not match the data held by Dukcapil (the Population and Civil Registration directorate). Common mismatch causes include an address registered at a previous residence, a name spelling that differs between the KTP and old NPWP card, or a family card (KK) number that has not been updated after marriage or household changes. To resolve: first update your data with the local Dukcapil office so the KTP reflects accurate information, then request a taxpayer data update (perubahan data) at your registered KPP or via the Coretax portal. For foreign nationals, additional friction arises from passport-name transliteration differences — the DJP acknowledged specific issues for Chinese-passport holders during the 2025 Coretax rollout, requiring manual resolution at the KPP. [13] [14]

Related Resources

- Malaysia TIN Guide — SST registration and e-Invoice mandate for comparison

- Singapore TIN Guide — UEN structure and GST digital services

- Vietnam MST Guide — ASEAN tax ID formats

- Worldwide Tax Rates — Indonesia PPN rate in global context