France TIN number guide

This post is also available in: Español|中文|Deutsch|Português|Français

Numéro d'identification fiscale (NIF)

The tax authorities in France assign a tax identification number (TIN) to individuals fulfilling their tax obligations. This unique and perpetual TIN is allocated during an individual's registration in the French tax administration databases. Referred to as numéro fiscal de référence or numéro SPI in French, this identifier ensures reliability and permanence. Stay informed about the numéro fiscal de référence or numéro SPI, vital for individuals navigating the French tax system. Understanding this distinctive identifier is essential for seamless compliance with tax obligations in France.

Format

The NIF comprises of 13 numerals in the format 99 99 999 999 999. The initial digit of the TIN is consistently 0, 1, 2, or 3.

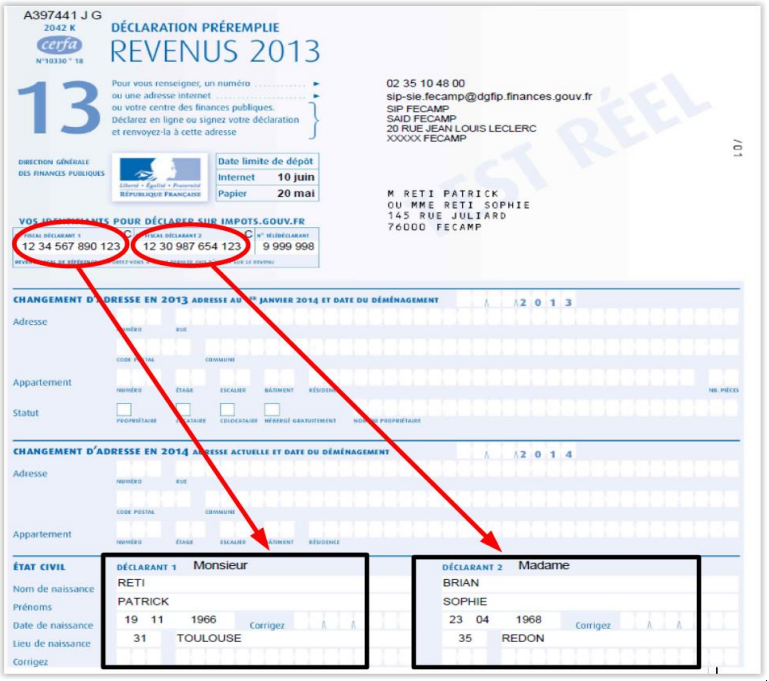

|

| Numéro fiscal on tax return |

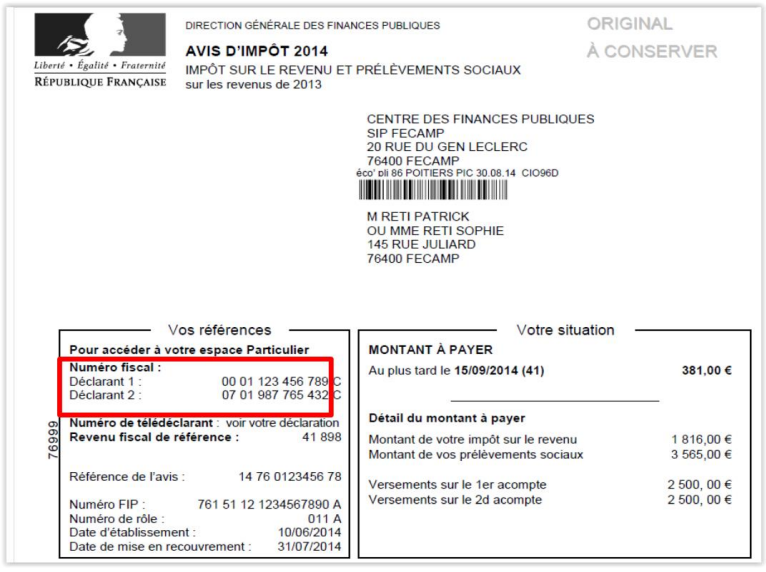

|

| Numéro fiscal on Notice of assessment |

SIREN

Upon establishment, French entities and individuals engaging in business activities are assigned an identification number by a governmental authority. This numéro SIREN serves various purposes, notably for taxation. Financial institutions like Fonds communs de placement (FCP) and Sociétés d'investissement à capital variable (SICAV) fall into this category. Unlike FCP, SICAV does not possess a tax identification number. Notably, the collection of tax identification numbers is not mandatory for entities classified as financial institutions (FIs)

Format

The SIREN number comprises 9 numerals in the format 999 999 999.

Official database - SIREN Search

Taxe sur la Valeur Ajoutee (TVA)

Format - FR (country code) + 2 digits + SIREN

Country code + 11 characters. May include alphabetical characters (any except O or I) as first or second or first and second characters.

Example - 12345678901, X1234567890, 1X123456789, XX123456789

SIRET

The SIRET (Système d'Identification du Répertoire des Entreprises et de leurs Établissements) is a unique identification number assigned to businesses in France. It consists of 14 digits and serves to identify specific establishments of a business. The SIRET number is crucial for business registration, tracking, and compliance purposes. It is part of the broader French business registration system, including the SIREN (Système d'Identification du Répertoire des Entreprises).

The SIRET number, a 14-digit identifier, comprises the SIREN number along with an extra five-digit component representing the specific location or establishment of the business. Consequently, the SIRET number offers more granular details about the physical location of the business within France.

|

| SIRET |

Frequently Asked Questions

My invoice was rejected because I put SIREN instead of SIRET — what is the legal requirement, and what is the penalty?

French commercial law (Article L. 123-237 of the Code de commerce) requires the SIRET number — not just the SIREN — on invoices issued by a business to another business. SIRET is the 14-digit identifier (SIREN + 5-digit NIC) that pinpoints the specific establishment issuing the invoice. Putting only the SIREN (9 digits) is a missing mandatory mention. Under Article 1737 of the Code général des impôts, the penalty is €15 per missing or inaccurate mention per invoice, capped at 25% of the invoice amount. A first-time error corrected within 30 days of a tax authority notice is not penalised. The client's SIRET also becomes a mandatory field on e-invoices from September 2026. [1] [2]

When does a French auto-entrepreneur have to start charging TVA, and did the thresholds change in 2025?

The franchise en base de TVA (VAT exemption) for micro-entrepreneurs survives a 2025 reform attempt that would have cut thresholds to €25,000 — that reform was abandoned by law no. 2025-1044 of November 3, 2025. The 2026 thresholds remain €37,500 (services) and €85,000 (goods). However, the triggering rule changed from January 1, 2025: exceeding the basic threshold during the year now means TVA becomes due from January 1 of the following year (the old two-year grace period is gone). Exceeding the tolerance threshold (€41,250 for services / €93,500 for goods) still triggers TVA immediately, retroactive to the first day of that month. Once TVA-liable, you receive a TVA intracommunautaire number based on your SIREN. [1] [2]

New micro-entrepreneurs are surprised by a CFE bill in year two — is the first year really exempt?

Yes. Micro-entrepreneurs (auto-entrepreneurs) are fully exempt from Cotisation Foncière des Entreprises (CFE) in the calendar year of business creation — no bill arrives at all. The shock hits in year two: a CFE notice appears based on the minimum cotisation for your municipality, and in year three the tax can jump again because the base switches to rental values from year N-2 without the 50% reduction that applied in year two. Micro-entrepreneurs with annual revenue below €5,000 are also exempt from the minimum CFE contribution regardless of how long they have been operating. To avoid the surprise, file the initial CFE declaration (form 1447-C) before December 31 of your creation year even though you owe nothing. [1] [2]

How does a non-resident foreigner obtain a French NIF (numéro fiscal) without physically visiting France?

Non-residents who need a French NIF but have never filed a French tax return can request one entirely online via impots.gouv.fr without travelling to France. The process: go to the "Votre espace particulier" section, click "Vous n'avez pas encore de numéro fiscal ?" and submit your civil status, a French postal address (a friend's address or your accountant's is acceptable), and a copy of your identity document. DGFiP typically assigns the 13-digit NIF within one week and notifies you by email. Non-residents with French-source income must direct paper requests to the Service des Impôts des Particuliers Non-Résidents (SIPNR), 10 rue du Centre, TSA 10010, 93465 Noisy-le-Grand Cedex. [1] [2]

Which companies must comply with France's e-invoicing mandate by September 2026, and do micro-enterprises get extra time?

France's mandatory B2B e-invoicing reform (originally planned for 2024 and delayed twice) sets a two-tier deadline. From September 1, 2026, all VAT-registered businesses must be able to receive e-invoices, and large enterprises (grandes entreprises) and mid-sized companies (ETI) must also issue them. From September 1, 2027, SMEs (PME) and micro-enterprises must issue e-invoices as well. Invoices must flow through a certified Plateforme de Dématérialisation Partenaire (PDP) for B2B transactions or through Chorus Pro for public-sector (B2G) invoicing. The SIREN and SIRET of both issuer and recipient are mandatory data fields in the electronic invoice. Non-compliance with the issuance obligation will trigger financial penalties under the 2026 Finance Law amendments to Article 1737 of the Code général des impôts. [1] [2]

Related Resources

- France VAT country guide

- How to verify French TVA numbers

- How to verify French SIREN numbers

- How to verify French SIRET numbers

- How to verify French EORI numbers

- France e-invoicing (Chorus Pro) guide

- Worldwide directory of VAT and tax ID names

- VAT registration thresholds worldwide

How Lookuptax can help you ?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.