Czechia TIN / DIČ Complete Guide — Format, Registration & Compliance

This post is also available in: Español|中文|Deutsch|Português|Français

Daňové identifikační číslo (DIČ)

The Daňové identifikační číslo (DIČ) is the Czech tax identification number issued by the Czech Financial Administration (Finanční správa). It is listed in the worldwide directory of VAT and tax ID names and appears on tax returns, VAT filings, and cross-border EU invoices. Understanding the DIČ is complicated by two common sources of confusion: it differs by entity type (individuals vs. companies), and it is not the same as VAT registration.

Format by Entity Type

| Entity type | DIČ structure | Digits after CZ |

|---|---|---|

| Legal entity (s.r.o., a.s.) | CZ + IČO | 8 |

| Individual / OSVČ (born ≥ 1954) | CZ + rodné číslo | 10 |

| Individual / OSVČ (born before 1954) | CZ + rodné číslo | 9 |

Format notation: 999999/999 or 999999/9999 (the slash is part of the rodné číslo but is omitted in the CZ-prefixed DIČ used for EU purposes, e.g. CZ8501015432).

For businesses registered for VAT, the CZ-prefixed DIČ functions as the Czech VAT number verifiable through the EU VIES system. To verify a Czech DIČ online, use the MOJE DANĚ portal operated by the Czech Financial Administration.

IČO vs. DIČ — The Critical Distinction

IČO (Identifikační číslo osoby) is the 8-digit business identification number, assigned when a company or trade licence is established. It is used on invoices, contracts, and the commercial register and is always 8 digits with no country prefix.

DIČ is the tax ID and is built on top of the IČO for companies (CZ + IČO) or on top of the rodné číslo for individuals. A business can have an IČO without a DIČ if it has not registered for any tax. From 1 January 2024, income tax registration — and therefore automatic DIČ assignment — is no longer mandatory for new sole traders. Freelancers without a Czech birth number, and all businesses that need a DIČ for VAT or other filings, must apply voluntarily.

Rodné číslo — The Individual's Underlying Identifier

The rodné číslo (birth number) encodes date of birth and sex in the format YYMMDD/XXXX. For women, the month is increased by 50 (so January = 51). Because the DIČ for individuals is simply CZ + rodné číslo, it exposes the holder's date of birth and sex on every invoice. Since 2021, individuals may request the Finanční správa to assign an alternative identifier (not based on the birth number) to protect this personal data — the procedure is described in methodology guidance No. 79651/20/7700-10123-010450.

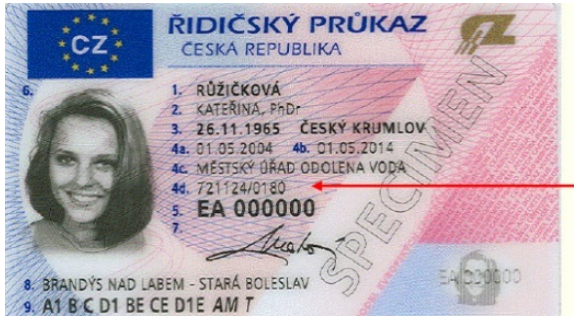

|

| TIN on Identification card |

|  |

VAT Registration Thresholds (2025)

The Czech VAT Act was amended effective 1 January 2025 with two distinct registration triggers for domestic businesses:

- Threshold 1 — CZK 2,000,000: Registration required from 1 January of the following calendar year.

- Threshold 2 — CZK 2,536,500: Immediate registration required the day after this threshold is exceeded.

Non-resident businesses face no threshold at all: VAT registration is required from the first taxable supply in Czechia where reverse charge does not apply. All non-resident registrations go through the Tax Office for the Moravian-Silesian Region.

"Light VAT" (identifikovaná osoba) is a partial registration category for Czech businesses that do not exceed the domestic threshold but receive services from EU suppliers (e.g. Google Ads, cloud platforms) or make B2B service supplies to EU clients. Failure to register as an identifikovaná osoba when required carries a penalty of up to CZK 500,000.

Where to Find Your DIČ

- Individuals: On your tax assessment notice, or in the Daňová Informační Schránka (DIS) taxpayer portal.

- Businesses: In the ARES registry (Ministry of Finance business register) by searching the company's IČO.

- VAT payers: Verifiable via the MOJE DANĚ portal or the EU VIES portal.

Frequently Asked Questions

Why does my DIČ appear valid on VIES but my German customer's ERP still rejects it?

The VIES database reflects active VAT registration status, not merely DIČ issuance. A Czech DIČ prefixed with "CZ" is only added to VIES after the business completes a separate VAT registration — holding a DIČ for income tax purposes does not automatically enroll the number in VIES. [1] Additionally, VIES data is pulled from national registers with a lag; a newly approved Czech VAT registration may take 24–48 hours to propagate to VIES. If the number is genuinely VAT-active and still fails, request a dated confirmation letter (rozhodnutí o registraci) from the Finanční správa and supply it to your customer as proof. [2]

Since January 2024, DIČ registration is "no longer mandatory" — does that mean I can skip it even for invoicing EU clients?

No. The 2024 consolidation package removed the obligation for new sole traders (OSVČ) to register for income tax as a standalone step, meaning a DIČ is no longer automatically assigned at trade-licence registration. However, if you supply B2B services to clients in other EU member states, you are still legally required to register as an identifikovaná osoba (light VAT), which does assign a DIČ. [1] Registration must occur within 15 days of your first intra-EU B2B service supply. Without it, Czech VAT law treats your cross-border services as unaccounted supplies, exposing you to backdated VAT and penalties. Foreign freelancers without a Czech rodné číslo should proactively apply for a DIČ regardless of the 2024 change. [2]

My DIČ is based on my rodné číslo, which reveals my date of birth — can I get a different number?

Yes. A 2021 amendment to the Tax Code introduced a right for individuals to request an alternative identifier that replaces the birth number within their DIČ. The request is submitted to your local tax office and the replacement identifier is assigned under methodology guidance No. 79651/20/7700-10123-010450. [1] This matters in practice because the rodné číslo embedded in a DIČ discloses the holder's sex and full date of birth on every issued invoice — information protected as sensitive personal data under GDPR and Act No. 110/2019 Coll. Only authorised entities (employers, banks, tax authorities) may lawfully process the rodné číslo; routine B2B invoice recipients generally do not meet that threshold. [2]

What are the exact penalties for late filing of the VAT Control Statement (kontrolní hlášení)?

The kontrolní hlášení is Czechia's transaction-level VAT reporting obligation and carries automatic fines with no grace period. Filing late without a summons: CZK 1,000. Filing after an official tax authority summons: CZK 10,000. Failing to file even after a summons: up to CZK 50,000. In egregious cases the authority can impose up to CZK 500,000 if intentional non-compliance is established. [1] From January 2023, first-time violations in a given calendar year may be waived on application under Section 101j of Act No. 235/2004 Coll. Even minor mismatches between the control statement and your VAT return trigger a mandatory correction notice from the tax authority. [2]

What is the joint liability risk when buying from a Czech supplier listed as an "unreliable VAT payer" (nespolehlivý plátce)?

Under Section 106a of Act No. 235/2004 Coll., if you purchase from a supplier whose unreliable VAT payer status was publicly listed at the date of supply, you become jointly liable for the VAT they fail to remit to the tax authority. [1] The same joint liability applies if you pay to a bank account not registered in the Czech Financial Administration's published account register — regardless of the supplier's reliability status. Suppliers are classified as unreliable after accumulating a VAT undercharge of CZK 500,000 or more over at least three consecutive months. Always check every supplier's DIČ at the MOJE DANĚ registry and confirm the payment account before each transaction. [2]

Do non-EU companies making B2C digital sales into Czechia need to register immediately?

Yes — there is no turnover threshold for non-established foreign businesses making taxable B2C supplies in the Czech Republic where reverse charge does not apply. Registration is required from the first taxable supply. [1] EU-based sellers of B2C digital services can use the EU One Stop Shop (OSS) until their EU-wide B2C digital sales reach EUR 10,000. Non-EU businesses have no OSS option and must register directly with the Tax Office for the Moravian-Silesian Region, file returns in Czech, and — since January 2025 — appoint an authorised representative for service of documents. [2]

When does a payment to a non-resident trigger Czech withholding tax, and at what rate?

Czech tax residents must withhold tax on payments for services physically performed in the Czech Republic by non-residents, royalties, dividends, and interest under Act No. 586/1992 Coll. on Income Taxes. The standard rate is 15% for residents of EU/EEA states and countries with which Czechia has a Double Tax Treaty (DTT) or Tax Information Exchange Agreement. [1] For residents of countries with no treaty relationship with Czechia, the rate rises to 35%. EU/EEA residents who had withholding applied at 15% may file a Czech income tax return to recover excess tax above their actual liability. Non-resident invoices to Czech clients should document the applicable treaty exemption or reduced rate before payment. [2]

Related Resources

- How to verify a Czech DIČ online — step-by-step MOJE DANĚ portal guide

- EU VIES and INTRASTAT — a guide for EU traders — how VIES validation works and why numbers sometimes fail

- Slovakia TIN guide — neighbouring country with a similar DIČ naming convention but different rules

- Germany TIN guide — frequent Czech cross-border trading partner

- EU One Stop Shop (OSS) explained — how EU B2C digital sellers can avoid direct Czech registration

- Reverse charge mechanism explained — when it applies and when it shifts the Czech registration obligation

How Lookuptax can help you?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.