Ecuador RUC Tax ID Number — Format, Validation & Compliance Guide

This post is also available in: Español|中文|Deutsch|Português|Français

Registro Unico de Contribuyentes (RUC)

Ecuador's tax identification number is the Registro Único de Contribuyentes (RUC), administered by the Servicio de Rentas Internas (SRI). The RUC identifies every taxpayer — individuals, private companies, and public entities — for all tax-related obligations, from IVA filings to income-tax withholding remittances. It is also listed in the worldwide directory of VAT and tax ID names.

Registration is mandatory for any national or foreigner conducting economic activity in Ecuador, whether permanently or occasionally, as well as for holders of assets generating taxable income. Public entities, armed forces units, cooperatives, and foundations must also register regardless of profit intent. Foreign companies holding immovable property in Ecuador must obtain a RUC even if that property generates no taxable income — a requirement enforced at the point of notarial transfer.

One exemption applies: international organisations, embassies, consulates, and commercial offices of countries with diplomatic or consular ties to Ecuador are not obliged to register, but may do so voluntarily.

RUC Format

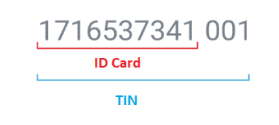

All RUC numbers are 13 digits. The structure varies by taxpayer category, but the final three digits are always 001 (indicating the principal establishment; branches use 002, 003, and so on).

Individuals (Natural Persons)

The first 10 digits are identical to the holder's national identity card (cédula de identidad) or citizenship card. The third digit is always between 0 and 5. The last three digits are always 001.

Example structure: [Province code (2)] [0–5] [Sequence (7)] [001]

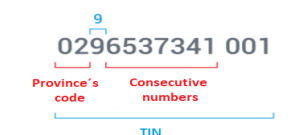

Private Companies (Legal Entities)

- Digits 1–2: Province code of RUC issuance

- Digit 3: Always 9

- Digits 4–9: Sequential number

- Digit 10: Check digit (verhoeff-style algorithm applied by SRI)

- Digits 11–13: Always 001

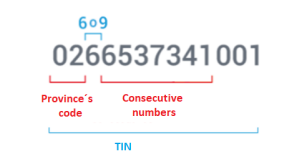

Public Entities

- Digits 1–2: Province code

- Digit 3: Always 6

- Digits 4–8: Sequential number

- Digit 9: Check digit

- Digit 10: Always 0

- Digits 11–13: Always 001

|  |  |

| Individuals | Private Companies | Public Companies |

RUC Registration Process

Registration is completed online at srienlinea.sri.gob.ec or in person at any SRI taxpayer service office. Ecuadorian citizens provide their cédula and proof of address (utility invoice or property tax receipt). Foreign residents must present a valid passport, current immigration document (visa, residency permit, or cédula de extranjería), and a proof of Ecuadorian address.

A RUC is assigned immediately upon successful submission. The SRI may suspend a RUC automatically if the taxpayer shows no registered economic activity for six consecutive months and has not requested authorisation to issue electronic sales receipts. A suspended RUC causes all pending electronic invoices issued under that number to be rejected by the SRI validation system. Reactivation requires attending an SRI office with updated documentation; online self-reactivation is only available to taxpayers who self-initiated the suspension.

Electronic Invoicing (Facturación Electrónica)

Ecuador mandates electronic invoicing for the majority of taxpayers. To issue electronic comprobantes, a taxpayer must hold an active RUC, register in the SRI online portal, obtain an authorisation to issue electronic vouchers, and use a valid digital signature certificate. The SRI validates each document in real time via XML submission; a "RECHAZADO" (rejected) status on the return XML means the invoice is fiscally void and the issuer must correct and retransmit within 24 hours.

The most frequent rejection causes are: inactive or suspended RUC, establishment listed as closed, missing electronic agreement acceptance, invalid digital signature, or a sequential invoice number already registered in the SRI database. Failure to deliver a valid comprobante de venta carries penalties of up to 30 basic salaries under SRI regulations.

RIMPE — Simplified Regime

The Régimen Simplificado para Emprendedores y Negocios Populares (RIMPE) divides small taxpayers into two sub-categories with distinct obligations.

| Category | Annual gross income | IVA rate charged | Invoice type | Accounting |

|---|---|---|---|---|

| Negocio Popular | Up to USD 20,000 | 0% | Pre-printed nota de venta or electronic | Income/expense log |

| Emprendedor | USD 20,001–300,000 | 15% | Electronic invoice only | Formal accounting required (from Aug 1, 2024) |

Misclassifying as Negocio Popular when income exceeds the USD 20,000 threshold triggers back-IVA assessments plus 3% monthly late-payment interest. RIMPE Emprendedor income tax is declared each March; Negocio Popular files in May.

IVA Rate

Ecuador raised IVA from 12% to 13% on 12 March 2024, then to 15% effective 1 April 2024, under emergency security legislation. Executive Decree 470 (published 10 December 2024) confirmed the 15% rate for 2025. A December 2025 SRI circular (NAC-DGECCGC25-00000006) confirmed the 15% rate also applies in 2026 absent a new executive decree. No reversion to 12% is currently scheduled.

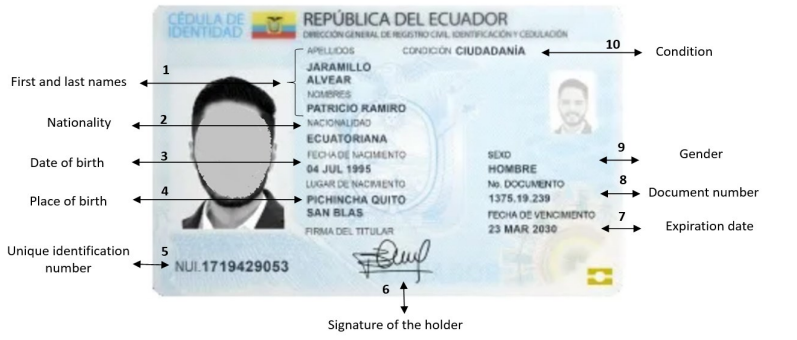

ID Card

The Organic Law for Identity and Civil Data Management designates the identity card as the primary identification document for both Ecuadorian and foreign individuals in Ecuador. The 10-digit card number is issued exclusively by the General Directorate of Civil Registry.

Format: 10 digits

|

| ID card Front side |

|

| ID card back side |

Frequently Asked Questions

Does my RIMPE category (Negocio Popular vs Emprendedor) change my IVA and invoicing obligations?

Yes, and the difference is significant. Negocio Popular applies to natural persons with gross annual income up to USD 20,000: they charge 0% IVA, are not required to file monthly IVA declarations, and may issue pre-printed notas de venta instead of electronic invoices. Emprendedor applies to those with annual income between USD 20,001 and USD 300,000: they must charge the standard 15% IVA, file monthly IVA returns, and issue electronic invoices via the SRI system. As of August 1, 2024, all Emprendedores must maintain formal accounting records. Misclassifying as Negocio Popular when your sales exceed the threshold triggers back-IVA assessments plus 3% monthly late-payment penalties. [1] [2]

Ecuador's IVA rose from 12% to 15% — is the 15% rate now permanent, and what triggered the change?

Ecuador raised IVA from 12% to 13% on March 12, 2024, then to 15% effective April 1, 2024, under emergency legislation (Ley Orgánica para Enfrentar el Conflicto Armado Interno) introduced to finance the internal security crisis. Executive Decree 470, published December 10, 2024, confirmed the 15% rate remains in force throughout 2025; a subsequent SRI circular confirmed the same rate applies in 2026. No reversion to 12% is currently scheduled. Foreign businesses issuing back-dated corrective invoices must apply the rate in effect on the original supply date — invoices corrected across the April 2024 boundary require a credit note at the old rate and a new invoice at 15%. [3] [4]

My Ecuadorian client is withholding 25% from my invoice — is that legal, and can a tax treaty reduce it?

Yes, it is legal. Payments made to non-residents for services rendered or used in Ecuador are subject to a 25% income-tax withholding at source, applied by the Ecuadorian payer who remits it directly to the SRI. This applies regardless of whether the foreign supplier holds a RUC. Treaty relief is available: Ecuador's treaties (Andean Community Decision 578, plus bilateral treaties with 20+ countries) can reduce or eliminate the rate. As of November 29, 2021, the payer may apply treaty benefits automatically without prior SRI authorisation. Without a treaty, the 25% is a final cost to the foreign supplier, not a credit. Verify treaty status via the SRI treaty register before invoicing. [5] [6]

Why does my SRI tax payment deadline vary each month, and how does the 9th digit of my RUC determine it?

Ecuador's SRI staggers filing deadlines by taxpayer to reduce system overload. The 9th digit of your RUC determines the monthly due date for IVA declarations, income-tax withholdings (retenciones), and other periodic obligations: digit 1 = 10th of the following month, digit 2 = 12th, digit 3 = 14th, digit 4 = 16th, digit 5 = 18th, digit 6 = 20th, digit 7 = 22nd, digit 8 = 24th, digit 9 = 26th, digit 0 = 28th. Missing your specific deadline triggers an automatic 3% monthly penalty on the unpaid amount — there is no grace period. New RUC holders are often unaware of this staggered system and incorrectly assume the last day of the month is the deadline. [5] [1]

As a foreign SaaS provider selling to Ecuadorian consumers, must I register for IVA, and does selling only B2B exempt me?

Since December 2024, Ecuador requires foreign digital service providers to self-register for IVA and charge 15% directly to Ecuadorian B2C customers — replacing the previous system where local payment processors withheld on your behalf. There is no registration threshold: even a single taxable sale to an Ecuadorian consumer triggers the obligation. The B2B exception is real but narrow: if your Ecuadorian customer is an IVA-registered business that will apply the reverse charge, you do not register. Registration is done entirely online via the SRI portal, does not create a permanent establishment, and requires monthly returns payable in USD. Taxable services include streaming, SaaS, online advertising, app downloads, and digital content. [3] [7]

My SRI electronic invoice was rejected as "RECHAZADO" — what are the most common causes and how do I fix it?

The SRI rejects electronic comprobantes in real time for several reasons: the issuer's RUC is inactive or suspended; the issuer's establishment is listed as closed in the RUC; the taxpayer has not accepted the electronic agreement (convenio de facturación electrónica) in SRIenLinea; the digital signature certificate is expired or invalid; or the access key (clave de acceso) on the XML has already been registered. When a rejection occurs, the issuer must correct the specific error field, generate a new XML with a fresh clave de acceso, and retransmit to the SRI within 24 hours. The original rejected document carries no fiscal value and must not be delivered to the customer as proof of transaction. Verify your RUC status at srienlinea.sri.gob.ec before assuming the problem is technical. [8] [5]

The SRI suspended my RUC automatically — can I reactivate it online, and what triggers automatic suspension?

The SRI suspends a RUC automatically (suspensión de oficio) when the taxpayer shows no registered economic activity for six consecutive months and has not requested authorisation to issue electronic or printed sales receipts, or has not issued any electronic receipts in that period. A suspended RUC blocks all new electronic invoice authorisations immediately. If you self-initiated the suspension through SRIenLinea, you can reactivate online by logging in, selecting RUC → Suspension/Restart, and entering a new activity start date. If the SRI initiated the suspension, online reactivation is not available — you must attend an SRI service office with updated documentation proving resumed activity, and in some cases submit a UAFE compliance certificate. Reactivation is typically processed the same day at the office. [8] [9]

Related Resources

- Peru Tax ID Guide — Peru's RUC uses the same name and a similar 11-digit structure under SUNAT

- Colombia Tax ID Guide — NIT format, factura electrónica rules, and PES obligations for digital providers

- Chile Tax ID Guide — RUT with mod-11 check digit and SII e-invoicing (DTE) requirements

- How to verify an CUIT in Argentina — Step-by-step AFIP portal verification for Andean trade partners

- Countries and VAT Names — Global directory of tax ID names including Ecuador's RUC

How Lookuptax can help you?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.