Denmark TIN — CPR and CVR number guide

This post is also available in: Español|中文|Deutsch|Português|Français

Central Person Registration Number (CPR Number)

Denmark uses the CPR and CVR/SE numbers as its tax identifiers, listed in the worldwide directory of VAT and tax ID names. For business VAT numbers, the 8-digit CVR or SE number is prefixed with "DK" for EU cross-border transactions. To verify a Danish CVR number online, use the CVR registry or the EU VIES system.

In the Danish Central Person Registration System (CPR), every individual is enrolled if they meet the following criteria:

- Born or migrated to Denmark and are registered in the country.

- Covered under ATP, a specific work-related pension scheme.

- Mandated by tax authorities to obtain a CPR number for tax-related procedures in Denmark.

The Danish CPR number plays a crucial role in virtually all interactions with public authorities, including tax affairs. It is prominently featured on official identification documents such as passports, driver's licenses, health security cards, etc. It is also known as "personnummer" in Danish.

Format

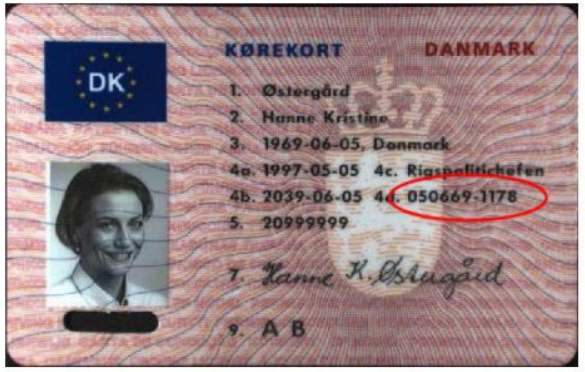

A CPR number follows the pattern DDMMYY-SSSC — 10 digits total with a hyphen after the sixth digit. The first six digits encode the birth date (day, month, two-digit year). The next three digits (SSS) are a sequence number that also encodes gender: an even final digit (C) indicates female; an odd final digit indicates male. Example: 010190-4321.

Modulus 11 check digit — The classic mod-11 validation uses weights 4 3 2 7 6 5 4 3 2 1 across all ten digits (hyphen excluded). However, since 1 October 2007, CPR numbers are issued that intentionally fail this check because valid sequences for certain birth dates were exhausted. Any system that hard-rejects a CPR for failing mod-11 is applying an obsolete rule and will block real Danish taxpayers.

Foreigners

In scenarios where an individual is not a resident in Denmark but is deemed taxable to the country by the Danish Tax Agency, such as in the case of employment, the Danish Customs and Tax Administration have the authority to provide a CPR number. The structure and format of this number mirror those issued by local municipalities. Non-resident workers on short stays (up to three consecutive months) receive a tax card instead — sufficient for payroll withholding but not for banking or public services.

|

| CPR on Driver's licence |

CVR Number or SE Number

Also known as "Momsregistreringsnummer" in Denmark, the Tax Identification Number (TIN) for non-natural persons or legal entities corresponds to the Danish CVR number. The issuance of the CVR number follows the guidelines of the CVR law and is overseen by the Danish Business Authority (Erhvervsstyrelsen), a division of the Ministry of Industry, Business, and Financial Affairs.

Corporations are required to apply for the CVR number during their establishment process. Non-natural persons and entities not classified as corporations have the option to delay CVR number application until they are obligated to register for VAT, excise duties, withheld tax on salaries, and similar obligations.

Format

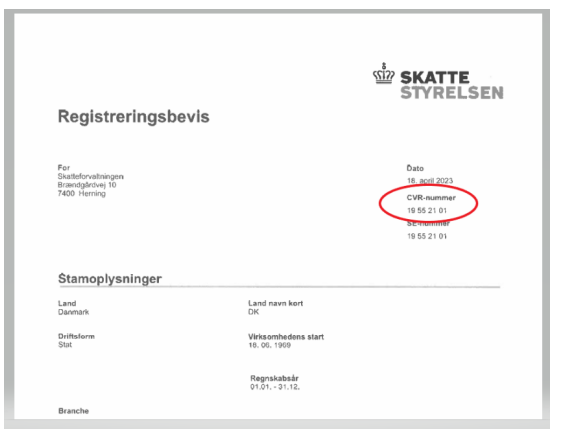

The CVR number consists of exactly 8 digits and satisfies a modulus 11 check using weights 2 7 6 5 4 3 2 1. The weighted sum of all eight digits must be divisible by 11 for the number to be valid. "CVR" or "SE" is frequently prefixed to the number — for instance, CVR 28866984 or SE 28866984. The EU VAT number is formed by prepending "DK": DK28866984. A common error in cross-border invoicing is using "DE" (Germany) or "SE" (Sweden) as the prefix — both cause VIES validation failures. In certain scenarios, a company may possess both a CVR number and a SE number.

Foreigners

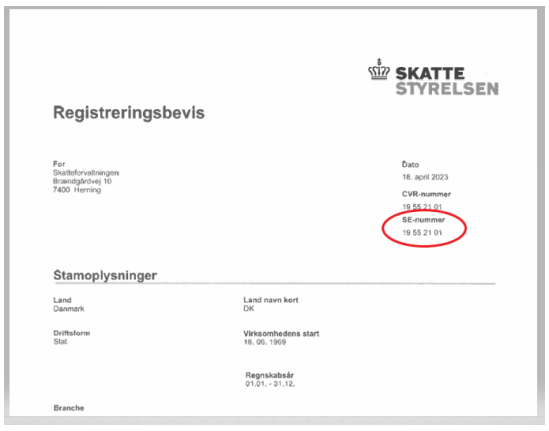

For foreign companies without a permanent establishment in Denmark registering for VAT, their TIN is represented by the Danish SE number. The SE number is issued in accordance with various tax, VAT, and excise laws and is managed by The Danish Tax Agency, which operates under the Ministry of Taxation. Foreign businesses with no Danish establishment must register via form 40.110 filed with Erhvervsstyrelsen and will receive an SE number that functions as their Danish VAT identifier. The DKK 50,000 annual turnover threshold for mandatory VAT registration applies to EU businesses; non-EU businesses with no Danish establishment must register from the first taxable supply.

|  |

| CVR number on Registration certificate | SE number on Registration certificate |

Frequently Asked Questions

Why do some Danish CPR numbers fail the modulus 11 check, and can they still be valid?

Yes, they remain fully valid. Since 1 October 2007, the Danish CPR authority issues numbers that do not satisfy the traditional modulus 11 check digit because valid sequences for certain birth dates were exhausted — January 1 is the default date assigned to immigrants whose exact birth date is unknown, and its sequences ran out first. Even numbers assigned to people born before 2007 can fail the check, because recently arrived immigrants may receive a post-2007 sequence regardless of their actual birth year. Any validation library, ERP system, or API integration that hard-rejects CPR numbers for failing mod-11 is using an obsolete rule and will incorrectly block real Danish taxpayers. Remove the hard-reject; treat mod-11 failure as a warning only. [1] [2]

I need a CPR number to open a bank account in Denmark, but landlords want a CPR number before they will rent to me. How do I break this cycle?

This circular dependency is the most frequently reported blocker for foreigners arriving in Denmark — and has become acute enough that international students resort to illegal address-registration arrangements to obtain CPR numbers. The legal path: EU/EEA citizens must first obtain an EU registration certificate from SIRI (the Danish Agency for International Recruitment and Integration); non-EU citizens must hold a Danish residence permit. Once residence documentation is in hand, register in person at International House Copenhagen or your local borgerservice centre — an employer letter or enrolment confirmation serves as proof of intended stay. Short-term workers (stays of three months or less) receive a tax card rather than a CPR, which covers payroll withholding but cannot be used for banking. [1] [2]

I am self-employed in Denmark and received a large unexpected tax bill in January. Why did this happen and how do I prevent it?

The cause is almost always an inaccurate forskudsopgørelse (preliminary income assessment). Skattestyrelsen publishes your assessment each November based on prior-year figures. If your B-income grew during the year but you did not update the assessment, B-skat instalments — paid in ten equal amounts between January and November — will have been too low, and the shortfall lands on your årsopgørelse (annual tax notice) in March. Outstanding tax paid after the 1 July deadline accrues interest at 3.7% per year from 1 January. The fix is to log into TastSelv and update field 221 (expected business profit) whenever your income changes materially. AM-bidrag (8%) is calculated first on gross B-income; income tax is then levied on the remaining 92%. [1] [2]

Does the 8% AM-bidrag (labour market contribution) apply to all freelance B-income, or only to salary?

AM-bidrag applies to all B-income from freelance work and self-employment, not only to salary paid by an employer. The contribution is calculated on your gross B-income before any business expense deductions, at a flat 8%. Income tax (B-skat) is then computed on the post-AM-bidrag amount — so your effective tax base is 92% of gross. Notable exemptions: SU (student grants), unemployment benefits (dagpenge), and pension payouts are not subject to AM-bidrag. Likewise, income earned before the calendar year you turn 18 is exempt. Confusing AM-bidrag with a deductible expense is a common error that causes freelancers to under-report their actual tax liability. [1] [2]

My business is VAT-registered in Denmark but not incorporated there — do I need to comply with the 2026 NemHandel e-invoicing mandate?

Yes, if your Danish VAT-registered net turnover exceeds DKK 300,000 in both 2024 and 2025. The Danish Bookkeeping Act (Act no. 700 of 24 May 2022) requires VAT-registered businesses — including foreign entities registered for Danish moms — to use a certified digital bookkeeping system capable of sending and receiving structured e-invoices. Accepted formats are Peppol BIS 3.0 and OIOUBL 2.1, routed via the NemHandel network or the interconnected Peppol network. Critically, only companies with a Danish CVR number can self-register in NemHandelRegisteret; foreign entities without a CVR must transact through an accredited Peppol access point. The B2B obligation took effect 1 January 2026 for most businesses (in-house systems had until 1 July 2026). Non-compliance penalties can reach DKK 1.5 million. [1] [2]

Why does my Danish partner's CVR number pass the VIRK registry check but fail EU VIES validation?

The CVR registry and EU VIES serve different purposes. A CVR number confirms that a Danish legal entity exists and is registered with the Danish Business Authority — but it does not prove VAT registration. To appear in VIES, a company must separately be registered for Danish moms (VAT) and hold an active SE number. The EU VAT identifier is always "DK" followed by the 8-digit CVR or SE number (e.g., DK28866984). A company may have a CVR number without any VAT obligation (for example, a holding company below the DKK 50,000 threshold). Always verify VAT status via VIES or Skattestyrelsen before zero-rating an intra-EU supply — a valid-looking CVR is not sufficient evidence of active VAT registration. [1] [2]

Related Resources

- How to verify a Danish CVR number online

- EU VIES VAT validation system

- Worldwide directory of VAT and tax ID names

- Norway TIN guide — Organisasjonsnummer and D-number

- Finland TIN guide — Y-tunnus and HETU

How Lookuptax can help you ?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.