Isle of Man Tax Identification Number (TIN) Guide

This post is also available in: Español|中文|Deutsch|Português|Français

The Isle of Man is a Crown dependency in the Irish Sea — self-governing, with its own Parliament (Tynwald), its own tax authority (the Income Tax Division), and its own National Insurance Fund. It is not part of the United Kingdom, but it shares the UK's VAT territory and uses National Insurance numbers that look identical to UK NINOs. This guide covers every tax identifier issued on the island, including the critical distinctions from their UK counterparts that catch newcomers and foreign businesses off guard.

Tax Reference Number (TRN)

The Isle of Man Income Tax Division issues a Tax Reference Number (TRN) to every individual, company, trust, foundation, and partnership obligated to file a Manx tax return. It is the primary identifier for all interactions with the Division — filing returns, receiving assessments, and online services.

Format

A TRN follows a fixed structure: one letter + six digits + optional hyphen and two-digit suffix.

| Entity type | Prefix letter | Example |

|---|---|---|

| Individual | H | H111111-11 |

| Company / LLC | C | C333333-33 |

| Trust, Foundation, Partnership / LLP | X | X555555-55 |

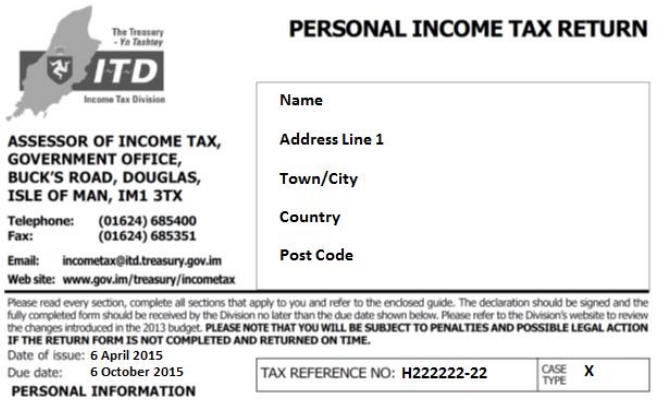

The two-digit suffix after the hyphen is optional. A number such as C222222 (without suffix) is fully valid. The TRN appears in the top-right corner of all correspondence from the Income Tax Division and on income tax return forms.

|

| TRN on Income Tax Return |

Who needs a TRN and how to register

Any person becoming Isle of Man tax resident must complete Form R25 (Registration for Manx Income Tax) and submit it to the Income Tax Division promptly after arriving — there is no grace period. Individuals with Isle of Man-source income who remain non-resident (employment income, rental income, or self-employment income derived from the island) must also register. A UK tax record or a UK Unique Taxpayer Reference (UTR) is not transferable — a separate Manx TRN is issued and must be used for all Isle of Man filings.

Non-residents are not entitled to a personal allowance; all taxable Isle of Man-source income is charged at a flat higher rate — 22% for 2024/25 (reduced to 21% from 6 April 2025). [1] [2]

Agent TRN

Agents (accountants and tax advisers) who act for multiple clients receive a separate 13-character alphanumeric Agent Tax Reference Number (format: C123456A01-12), confirmed by letter from the Division.

National Insurance Number (NINO)

Every employed individual in working age (16–65) must hold a National Insurance Number. The NINO is issued either by the Isle of Man Income Tax Division or by HMRC if the individual previously lived and worked in the UK before relocating to the Isle of Man.

Format

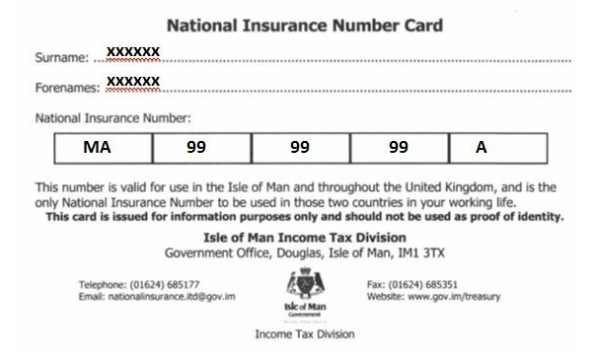

AA 999999 A — two letters, six digits, one suffix letter (A, B, C, or D). Example: MA999999A.

|

| National Insurance Card |

Isle of Man NI is separate from UK NI

Although the NINO format is identical to UK NINOs, the Isle of Man operates its own separate National Insurance Fund. Contributions paid in the Isle of Man build entitlement to a Manx state pension only — not the UK state pension. The full Manx State Pension from April 2025 is £251.30 per week, requiring 35 qualifying years. [3]

For 2025/26, Isle of Man Class 1 NI rates are set by Tynwald independently: employee rate 11% on earnings between £168 and £1,032 per week; employer rate 12.8% with no upper earnings limit for employers. [4]

VAT Registration Number

The Isle of Man forms a single VAT territory with the United Kingdom under the Customs and Excise Management Act. This means Isle of Man VAT numbers share the GB prefix format but are administered entirely separately by Isle of Man Customs & Excise — not HMRC.

Format

Isle of Man VAT numbers follow the same nine-digit structure as UK VAT numbers but are identifiable by the first two digits being 00:

GB 00X XXXX XX — for example, GB 001 2345 67

This differs from standard UK VAT numbers (where the first digits are not 00). See the United Kingdom TIN guide for a comparison of UK VAT number formats.

Registration

A business making taxable supplies on the Isle of Man must register directly with Isle of Man Customs & Excise using Form VAT1MAN. An existing UK HMRC VAT registration does not extend to the Isle of Man — they are separate registers. [5] [6]

The registration threshold mirrors the UK: £90,000 in taxable turnover from 1 April 2024 (deregistration threshold: £88,000).

Verification

Isle of Man VAT numbers cannot be verified through EU VIES (the Isle of Man is not in the EU VAT area) and do not appear in the standard HMRC "Check a VAT number" service for the UK register. Verification must be done directly via Isle of Man Customs & Excise or through a service such as Lookuptax. For how to verify UK VAT numbers, see the UK VAT verification guide.

Corporate Tax Overview

The Isle of Man's 0% standard corporate tax rate makes it attractive for holding structures, but three categories of income are taxed at higher rates:

| Income category | Rate |

|---|---|

| Standard company income | 0% |

| Banking business profits | 10% (15% for 2024/25 if in scope of Pillar 2) |

| Retail profits above £500,000 | 10% (15% for 2024/25 if in scope of Pillar 2) |

| Isle of Man land, property, and petroleum extraction | 20% |

The temporary 15% rate for 2024/25 is linked to the OECD Pillar 2 Global Minimum Tax initiative (consolidated group revenues exceeding €750 million). From 2025/26 the rate reverts to 10% for those categories unless further Tynwald action is taken. [7]

Economic Substance Requirements

Isle of Man companies earning income from any of nine "relevant sectors" must demonstrate genuine economic substance on the island for accounting periods starting on or after 1 January 2019. The relevant sectors are: holding, banking, insurance, fund management, shipping, intellectual property, headquarters, distribution and service centres, and financing and leasing.

Substance means adequate local employees, proportionate expenditure in the Isle of Man, a physical presence, and core income-generating activities (CIGA) actually conducted on the island. Failure triggers escalating sanctions: £10,000 for the first non-compliant period, £50,000 for the second, £100,000 for the third, and compulsory strike-off for continued failure — alongside automatic exchange of information with the beneficial owner's home tax authority. [8] [9]

Pure equity holding companies face a lighter-touch test (no CIGA requirement) but are not exempt from the substance rules.

OECD CRS and TIN Validity

For Common Reporting Standard (CRS) reporting, the TRN is the accepted TIN for Isle of Man individuals and entities. The OECD notes that Isle of Man VAT numbers (starting with 100-xxxx-xxx) are not accepted as TINs for CRS purposes — financial institutions must use the TRN. [10]

Frequently Asked Questions

Do new arrivals and non-residents need to register separately for Manx income tax, and what rate applies before they get a TRN?

Yes. Anyone becoming Isle of Man tax resident must complete Form R25 (Registration for Manx Income Tax) and submit it to the Income Tax Division as soon as possible after arriving — there is no grace period. [1] Until residence is confirmed, non-residents with Isle of Man-source income (employment, rental, or self-employment) are taxed at a flat rate with no personal allowance — 22% for 2024/25, reducing to 21% from 6 April 2025. [2] Individuals who have previously worked in the UK cannot simply use their UK tax record — a separate Manx Tax Reference Number is issued and must be used for all Isle of Man filings.

Why does an Isle of Man VAT number look like a UK VAT number, and does registering with HMRC cover Isle of Man supplies?

Isle of Man VAT numbers share the GB prefix and the same nine-digit format as UK VAT numbers, but are distinguished by the first two digits being "00" (for example, GB 001 2345 67). [5] Despite the shared format, the registers are completely separate: a business making taxable supplies in the Isle of Man must register directly with Isle of Man Customs & Excise using Form VAT1MAN — an existing UK HMRC registration does not extend to the Isle of Man. [6] Attempting to verify an Isle of Man number through the standard HMRC "Check a VAT number" service or EU VIES will fail because IoM numbers appear only on the Isle of Man register.

Do Isle of Man National Insurance contributions count toward a UK state pension, and how are employer obligations different?

No. Although workers use the same National Insurance number format on both islands, the Isle of Man operates its own separate National Insurance Fund. Contributions paid in the Isle of Man build entitlement to an Isle of Man state pension only — they do not count toward the UK state pension. [3] For employers, IoM NI rates are set independently by Tynwald: for 2025/26, the employer Class 1 rate is 12.8% and the employee rate is 11% on earnings between £168 and £1,032 per week. [4] A UK-based employer with workers on the Isle of Man must register and pay contributions to the Isle of Man Income Tax Division, not HMRC.

The Isle of Man standard corporate tax rate is 0% — which business activities are excluded and taxed at higher rates?

Three categories of income are carved out from the 0% standard rate. Banking business profits are taxed at 10%, rising to 15% for accounting periods in 2024/25 where the entity is in scope of the OECD Pillar 2 Global Minimum Tax (consolidated group revenues exceeding €750 million). [7] Retail businesses with annual Isle of Man taxable profits of £500,000 or more are also taxed at 10% (15% for 2024/25). Profits from Isle of Man land, property, and petroleum extraction activities are taxed at 20%. Companies that incorrectly assume their income falls under the 0% regime risk a substantial underpayment liability and late-payment interest when the Income Tax Division reclassifies the income. [7]

What happens to an Isle of Man holding company that fails to meet the economic substance test, and which activities trigger the requirement?

Isle of Man companies earning income from any of nine "relevant sectors" — including holding, banking, insurance, fund management, shipping, intellectual property, headquarters, distribution and service centres, and financing and leasing — must demonstrate genuine economic substance on the island for accounting periods starting on or after 1 January 2019. [8] Failure triggers escalating sanctions: a £10,000 fine for the first non-compliant period, £50,000 for the second, £100,000 for the third, and compulsory strike-off for continued failure — alongside automatic exchange of information with the beneficial owner's home tax authority. [9] Pure equity holding companies face a lighter-touch test but are not exempt.

Related Resources

- Guernsey TIN guide

- Jersey TIN guide

- United Kingdom TIN guide

- Northern Ireland TIN guide

- How to verify a UK VAT number

- Worldwide directory of VAT and tax ID names by country

How Lookuptax can help you in VAT validation?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.