Canada Tax ID Guide — SIN, BN, ITN, GST/HST & QST Formats

This post is also available in: Español

Canada operates a multi-identifier tax system administered primarily by the Canada Revenue Agency (CRA). Individual taxpayers use the Social Insurance Number (SIN); non-residents who cannot obtain a SIN use the Individual Tax Number (ITN); businesses are identified by a Business Number (BN), which serves as the root of all CRA program accounts. Provincial tax registrations — most notably Quebec Sales Tax (QST) — are separate obligations administered by Revenu Québec, not the CRA.

Social Insurance Number (SIN)

Every Canadian resident with income tax filing responsibilities must possess a Social Insurance Number. SINs are vital for tax reporting and must be provided to financial institutions and employers upon request. The number remains confidential and must not be requested by organisations that have no legal basis to collect it.

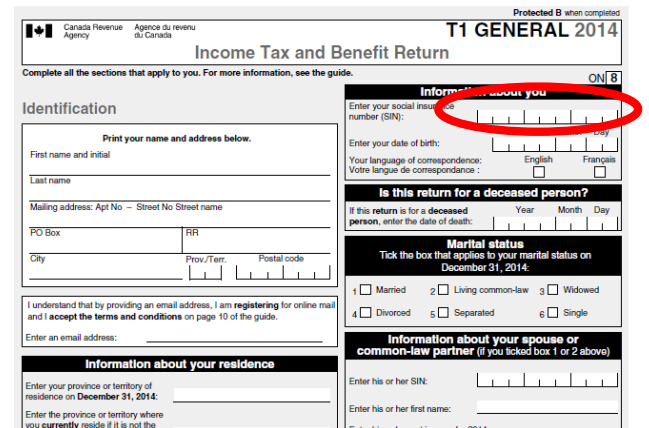

Format: A SIN is a nine-digit number validated using the Luhn algorithm (mod 10 checksum). Starting digits carry meaning:

- 1–8: Permanent residents, citizens, and most temporary residents

- 9: Temporary residents (visitors, permit holders, refugees) — these SINs carry an expiry date matching the immigration document that authorised work

SINs beginning with 9 expire when the underlying work authorisation expires. The CRA still recognises an expired temporary SIN for the purpose of filing a return for the period in which the income was earned — you do not need an active SIN to file historically, but you must renew before taking new employment.

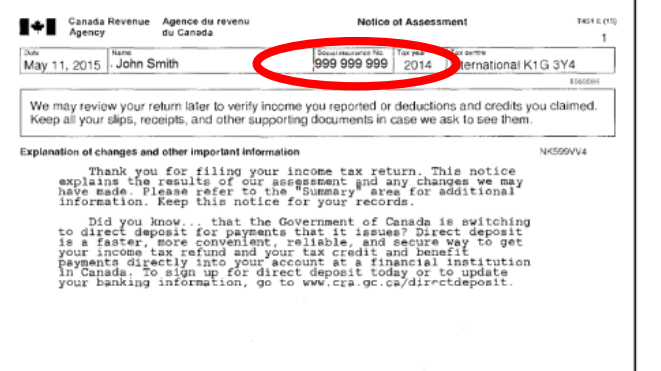

|  |

| SIN on income tax return | SIN on notices of tax assessment |

Individual Tax Number (ITN)

Non-residents who do not hold a SIN and have Canadian tax obligations — rental income, capital gains on Canadian property, or Canadian employment — must obtain an ITN by filing Form T1261 with the CRA's Sudbury Tax Centre. Processing takes six to eight weeks. The ITN is critical for non-resident real estate disposals: without one on file, the buyer is required to withhold 25% of the gross sale price under Section 116 of the Income Tax Act until a clearance certificate is issued.

Business Number (BN)

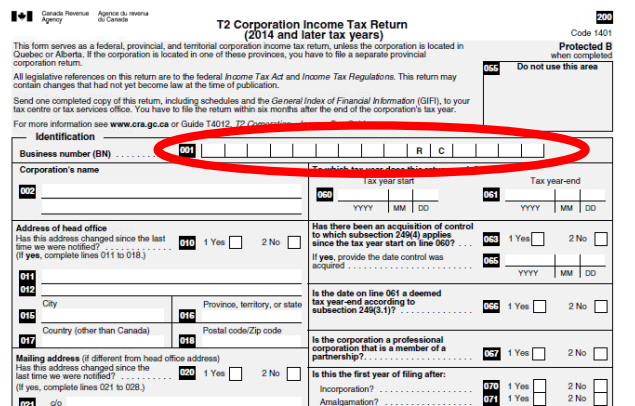

For businesses, the Canada Revenue Agency issues a nine-digit Business Number (BN) that serves as the unique root identifier. The BN itself is not a tax account — it is the anchor for one or more CRA program accounts appended to it.

Format: XXXXXXXXX (9 digits)

Program account suffixes extend the BN into specific tax obligations:

| Suffix | Program | Example |

|---|---|---|

| RT | GST/HST (goods and services / harmonised sales tax) | 123456789 RT 0001 |

| RP | Payroll deductions | 123456789 RP 0001 |

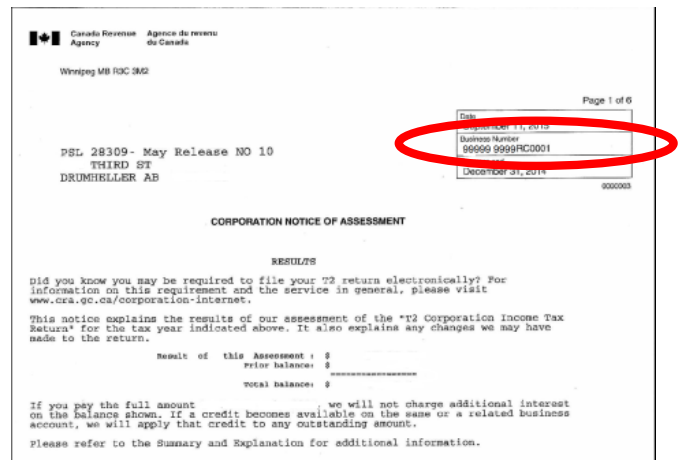

| RC | Corporation income tax | 123456789 RC 0001 |

| RR | Registered charities | 123456789 RR 0001 |

Each program account must be registered separately — having a GST/HST account (RT) does not automatically create a payroll account (RP). The four-digit reference number at the end (e.g., 0001) distinguishes multiple accounts of the same type under one BN.

Registration change (November 2025): As of November 3, 2025, the CRA no longer accepts BN or program account registrations by phone. All new registrations must be completed through Business Registration Online (BRO), which issues the BN and any requested program accounts instantly. Businesses owned by other businesses remain an exception and must register by paper.

|  |

| BN on income tax return | BN on notices of tax assessment |

Non-resident BN registration: Non-residents can register for a BN and GST/HST account entirely online without a Canadian physical presence. The digital-economy rules (effective July 1, 2021) require non-residents supplying digital services to Canadian consumers to register once Canadian sales exceed C$30,000 in any rolling 12-month period.

Goods and Services Tax / Harmonised Sales Tax (GST/HST)

The GST/HST account number is the BN followed by the RT suffix and a four-digit reference number: XXXXXXXXX RT 0001. On invoices, this is commonly written without spaces as 123456789RT0001. The CRA provides a free GST/HST Registry lookup where a buyer can confirm a supplier's registration status — see how to verify GST in Canada.

Invoice requirements: Invoices above C$30 must include the supplier's GST/HST registration number to allow the buyer to claim an Input Tax Credit (ITC). Missing or invalid registration numbers are the single most common cause of ITC disallowance at CRA audit.

Official Database — GST/HST search

Quebec Sales Tax (QST) Registration Number

The QST is a separate tax administered by Revenu Québec, independent of the CRA. Businesses operating in Quebec — including non-residents supplying digital services to Quebec consumers — must register separately with Revenu Québec. The QST registration obligation for non-resident digital-service providers has applied since January 1, 2019, predating the federal GST/HST digital-economy rules by more than two years.

Format: A QST account number is a unique 10-digit number issued by Revenu Québec, typically followed by TQ 0001.

Official Database — QST search

See also: how to verify QST in Canada and how to verify PST in Canada.

Harmonised Sales Tax (HST)

The HST is the merged federal/provincial sales tax applied in Ontario, Nova Scotia, New Brunswick, Newfoundland and Labrador, and Prince Edward Island. Businesses use the same BN + RT program account for both GST and HST — there is no separate HST registration number.

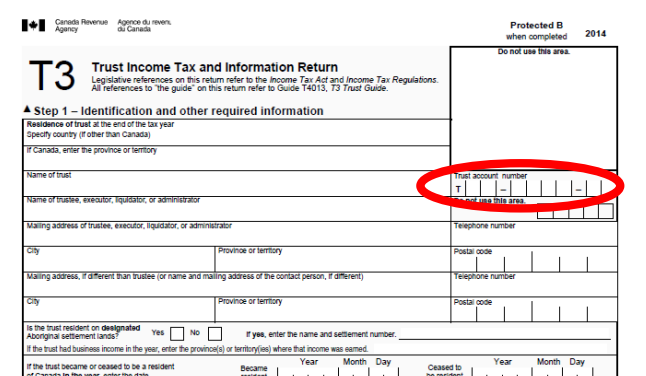

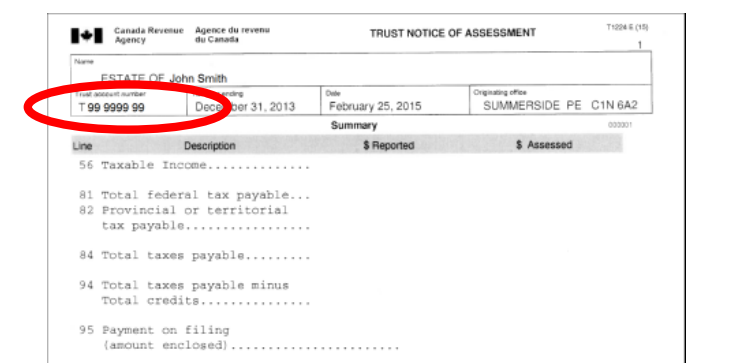

Trust Account Number

For trusts, the CRA issues an eight-digit trust account number prefixed by the letter T, e.g., T12345678. Canadian-resident trusts with income tax reporting responsibilities are required to hold this number.

|  |

| Trust Account Number on income tax return | Trust Account Number on notices of tax assessment |

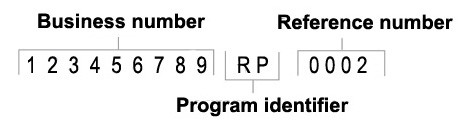

CRA Program Accounts — Full Structure

|

| CRA program account number |

A CRA program account number has three parts:

- The nine-digit BN identifying the business

- A two-letter program identifier code (RT, RP, RC, RR, etc.)

- A four-digit reference number identifying an individual program account (businesses can hold more than one account of the same type)

Related Resources

- How to verify GST/HST in Canada

- How to verify QST in Canada

- How to verify PST in Canada

- United Kingdom TIN guide — comparable multi-identifier system (UTR, NI, VAT)

- Australia TIN guide — ABN and TFN parallel structure

How Lookuptax can help you?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.

Frequently Asked Questions

I exceeded C$30,000 in sales without registering for GST/HST — am I liable for all the tax I never collected?

Yes. The moment your worldwide taxable revenues exceed C$30,000 in a single calendar quarter or across four consecutive calendar quarters, you cease to be a small supplier and are deemed a registrant under the Excise Tax Act from that date forward — including on the very sale that breached the threshold. You must register within 29 days of that triggering supply and owe all GST/HST that should have been collected from the date registration was required, plus CRA prescribed interest. Because you did not file returns during the unregistered period, you also cannot claim Input Tax Credits for expenses in that window. [1] [2]

Can my landlord or a business demand my Social Insurance Number as a condition of service?

No. The SIN Code of Practice issued by the Office of the Privacy Commissioner of Canada states that no private-sector organisation is legally authorised to require a SIN from customers for purposes other than income reporting. A landlord checking your credit does not need your SIN — credit bureaus can match on name and date of birth. Your employer is the clear statutory exception: under federal income tax and CPP legislation, employers must collect your SIN to issue T4 slips and Records of Employment, and you must provide it within three days of beginning employment. When any other party asks, you may refuse; they cannot lawfully deny you their product or service solely on that basis. [3] [4]

As a non-resident selling digital services to Canadians, do I register under the simplified GST/HST regime or the normal regime — and does it matter?

It matters significantly. Non-residents supplying cross-border digital products or services (streaming, SaaS, downloads) to Canadian consumers must register once Canadian sales exceed C$30,000 in any rolling 12-month period (effective July 1, 2021). The simplified regime requires no Canadian nexus and is faster to set up online, but it bars you from claiming any Input Tax Credits on Canadian expenses. The normal GST/HST regime allows ITC recovery but requires a fuller registration process. If you incur meaningful Canadian costs (servers, staff, offices), the normal regime may yield better cash economics — consult a Canadian tax adviser before choosing. [5] [6]

Does registering for federal GST/HST also cover my obligation to collect Quebec Sales Tax?

No. QST is a completely separate tax administered by Revenu Québec, not the CRA, and requires its own registration. Non-residents supplying digital services to Québec consumers have faced a QST registration obligation since January 1, 2019 — more than two years before the federal digital-economy rules took effect. The threshold is also C$30,000 in specified taxable supplies to Québec consumers. Businesses that registered for GST/HST after July 2021 but overlooked QST are exposed to back-assessed QST, interest, and penalties on all Québec sales since 2019. [7] [8]

As a non-resident, do I need an Individual Tax Number before selling Canadian real property — and what happens if I skip it?

Yes. Non-residents who do not hold a SIN must obtain a CRA Individual Tax Number by filing Form T1261 before disposing of taxable Canadian property. The ITN application must be mailed to the CRA Sudbury Tax Centre; allow six to eight weeks for processing. If you skip this step, the buyer or their lawyer is legally required to withhold 25% of the gross sale price (or a treaty-reduced rate) and remit it to the CRA until you file a Section 116 clearance certificate using Form T2062. Filing late or without an ITN delays the release of withheld funds and triggers interest charges. Submit Form T1261 well in advance of closing to avoid holdbacks. [9] [10]

My B2B customer says they cannot claim an Input Tax Credit because my GST/HST number is missing from my invoice — who is at fault?

You are. CRA invoice rules require that any invoice on which GST/HST is charged must include the supplier's 15-character GST/HST account number (9-digit BN + RT + 4-digit reference) for transactions above C$30. If the number is absent, incomplete, or does not match the CRA registry, the buyer's ITC claim is disallowed at audit. The buyer must repay the credit plus interest; they typically recover this from the supplier via contract or by withholding future payments. You can verify your own registration and correct the number at the free CRA GST/HST Registry before reissuing the invoice. [11] [12]

I tried to register my BN by phone after November 2025 — why was I redirected online?

As of November 3, 2025, the CRA no longer accepts new BN or CRA program account registrations by telephone. All new registrations must be completed through Business Registration Online (BRO), accessible via the CRA's My Business Account portal. BRO issues the BN and any requested program accounts (GST/HST, payroll, corporation income tax) instantly and is available 21 hours a day, 7 days a week. The only exceptions where a paper or phone process still applies are businesses owned by another business (e.g., subsidiaries) and certain complex multi-account situations. [13] [14]