Estonia TIN number guide

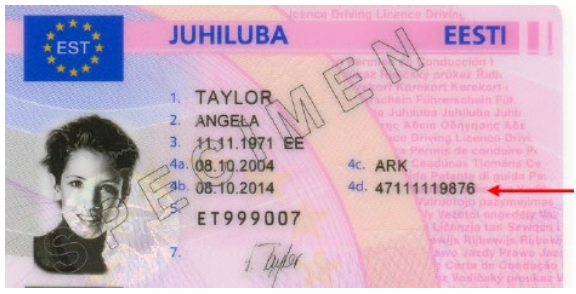

Isikukood

The "Isikukood" is the personal identification code used in Estonia. It is also commonly known as the "ID code" or "Estonian personal identification number." The Isikukood is a unique 11-digit identifier assigned to individuals in Estonia, including citizens and residents. The Isikukood includes information about the person's birthdate and gender, and it is widely used for identification purposes in both public and private sectors.

Format

An Estonian personal identification code comprises 11 digits, typically presented without any spaces or delimiters. The format is GYYMMDDSSSC, where G indicates the individual's sex and century of birth (odd number for male, even number for female; 1-2 for the 19th century, 3-4 for the 20th century, and 5-6 for the 21st century). YY represents the year of birth, MM is the month of birth, DD is the date of birth, SSS is a serial number differentiating individuals born on the same date, and C is a checksum.

The registration code for legal persons consists of 8 numbers. For entities like public limited companies, private limited companies, general partnerships, limited partnerships, and commercial associations, the code begins with the number 1. Non-profit associations start with the number 8, and foundations start with the number 9.

|

| Isikukood |

|  |

Käibemaksukohustuslase (KMKR)

"Käibemaksukohustuslane" is an Estonian term that translates to "Value Added Tax (VAT) taxpayer" in English. The abbreviation "KMKR" stands for "Käibemaksukohustuslase Registrinumber," which is the VAT registration number assigned to businesses or individuals obligated to pay value-added tax in Estonia.

Format - EE + 9 digits eg: EE100254507

Registrikood

"Registrikood" in Estonia refers to the registration code, often known as the registration number, assigned to legal entities for identification purposes. This code is essential for various administrative and business-related activities.

Format - 8 digits Eg: 10345833

Official database KMKR/Registrikood search

Frequently Asked Questions

Does my Estonian e-Residency company owe tax in my home country even though it is registered in Estonia?

Yes — this is the most misunderstood e-Residency trap. An Estonian company registered by an e-resident is a tax resident of Estonia and pays 0% corporate income tax on retained profits; however, e-Residency is not personal tax residency and does not exempt the company from foreign tax liabilities. If you manage the company exclusively from another country — signing contracts, negotiating prices, directing operations — that country may classify the company as a Permanent Establishment (PE) under its domestic law or the applicable tax treaty and impose its own corporate tax on those profits. EMTA's official guidance states explicitly: "e-Residency does not exempt companies from dual tax residency or foreign tax liabilities." [1] [2] Always obtain advice from a tax professional in your country of residence before distributing profits.

Why is EMTA now refusing KMKR (VAT) registration for e-Resident companies without Estonian economic substance?

Since August 2025, EMTA updated its VAT registration guidelines to require proof of a genuine economic connection to Estonia before granting a KMKR number. Companies that have no Estonian clients, suppliers, employees, or physical presence may be refused both mandatory and voluntary registration. EMTA's published criteria include: local business relationships, contracts with Estonian partners, or a registered office with actual operations — not merely a registered address via a service provider. This change has rendered VAT registration unavailable for many purely location-independent e-Residency companies. The practical consequence is that these companies cannot issue EU VAT-compliant invoices to EU business customers. You must apply through e-MTA and submit supporting documentation such as client contracts or supplier agreements demonstrating genuine Estonian economic activity. [1] [2]

How does the Estonian 22/78 distributed-profit tax work, and what happened to the 14% reduced dividend rate?

Estonia taxes corporate profit at 0% while it is retained inside the company, and applies tax only when profits are distributed. From 1 January 2025, the single rate is 22/78 of the net dividend paid. The formula means: to pay a net dividend of €1,000, the company owes €282.05 in income tax (1,000 × 22 ÷ 78), for a total gross cost of €1,282.05. Critically, the previously available 14/86 reduced rate for regularly paid dividends and the corresponding 7% personal withholding tax on dividends received by natural persons were both abolished from 1 January 2025. Transitional provisions still apply to dividend reserves that were taxed at the old 14/86 rate before 2025 — those can still be redistributed to a natural person with a 7% deduction. No further income tax is withheld at shareholder level when the company pays the 22/78 tax. [1] [2]

What VAT rate applies to Estonian invoices issued in mid-2025, and how does the 22% → 24% transition work?

Estonia raised the standard VAT rate from 22% to 24% on 1 July 2025 under an amendment to the Value Added Tax Act (Käibemaksuseadus § 15). The correct rate depends on the time of supply (käibe tekkimise aeg), not the invoice date. If the taxable supply occurred before 1 July 2025, the 22% rate applies even if the invoice is issued later; if the supply occurred on or after 1 July 2025, 24% applies. For continuous supplies or contracts that span the transition date, the portion of service delivered before 1 July 2025 is taxed at 22% and the remainder at 24%. Businesses must update accounting software, invoice templates, and OSS/IOSS registrations to reflect 24%. The previous increase from 20% to 22% took effect on 1 January 2024. [1] [2]

What is the KMD INF annex, and which VAT-registered businesses must file it?

Every VAT-registered person in Estonia — including non-resident businesses registered for Estonian VAT — must submit the KMD INF annex together with the monthly VAT return (KMD). The annex requires invoice-level reporting for all sales (Part A) and purchases (Part B) where the aggregate invoiced amount per transaction partner in the calendar month exceeds €1,000 excluding VAT. Required fields per invoice include: invoice date, invoice number, VAT rate, taxable amount, and trading partner name. Both the KMD and the KMD INF must be filed via e-MTA by the 20th day of the month following the taxable period, with VAT payment due on the same date. Failure to file the annex or filing with material errors can trigger EMTA audit queries and penalties under the Taxation Act (Maksukorralduse seadus). [1] [2]

Related Resources

- Worldwide directory of VAT and tax ID names

- VAT registration thresholds worldwide

- Global e-invoicing status tracker

How Lookuptax can help you ?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.