Lithuania Tax ID guide — Asmens Kodas, TIN & PVM number

Asmens Kodas (Personal Code)

The Asmens Kodas is Lithuania's national personal identification number, issued to all Lithuanian citizens and registered residents by the Population Register Service (Registrų centras). It serves as both the civil identification number and the individual TIN for all dealings with the State Tax Inspectorate (VMI) — no separate tax number is issued to residents.

Format: 11 digits, no spaces or delimiters

The code encodes four pieces of information in a fixed structure:

| Position | Length | Meaning |

|---|---|---|

| 1 | 1 digit | Gender and birth century: 1/2 = male/female born 1800–1899; 3/4 = male/female born 1900–1999; 5/6 = male/female born 2000–2099 |

| 2–7 | 6 digits | Date of birth in YYMMDD format |

| 8–10 | 3 digits | Serial number distinguishing persons born on the same date |

| 11 | 1 digit | Check digit for validation |

Example: 38503031234 — male (3), born 1985-03-03, serial 123, check digit 4.

|

| Asmens Kodas |

Juridinio Asmens Kodas (Legal Entity Code)

The Juridinio asmens kodas (company code) is a unique 9-digit numeric identifier assigned to every legal entity — UAB, MB, VšĮ, branches of foreign companies — at the moment of registration in the Register of Legal Entities (Juridinių asmenų registras, JAR) administered by Registrų centras.

Format: 9 digits, numeric only

The company code is public information. You can look it up free of charge via the JAR public search portal at registrucentras.lt/jar/p_en/. The code appears on incorporation certificates, official invoices, contracts, and all VMI filings.

The Juridinio asmens kodas is not the same as the PVM (VAT) number — a company can have a company code without being a VAT payer. Once VAT-registered, the company also receives a PVM mokėtojo kodas (see below), which is built from the company code but prefixed with "LT".

TIN (Taxpayer Identification Number)

For Lithuanian legal entities, the TIN used in VMI filings follows a specific algorithm. The TIN uses the format F || SEQ || K, where:

- F is a fixed prefix digit — either 6 or 9.

- SEQ is an 8-digit sequence of natural numbers (e.g., 00000001, 00000002).

- K is a control digit calculated as follows:

The 10-digit TIN N9N8N7N6N5N4N3N2N1K is validated by:

- Extract digits N9 to N1.

- Multiply each digit by 9, 8, 7, 6, 5, 4, 3, 2, 1 respectively and sum: A = Σ(Ni × i).

- Divide A by the two-digit number formed by N9N8: B = A mod N9N8.

- If B < 10, K = B. If B ≥ 10, sum the individual digits of B to get Z.

- If Z < 10, K = Z. If Z ≥ 10, repeat until result < 10 — that final value is K.

|

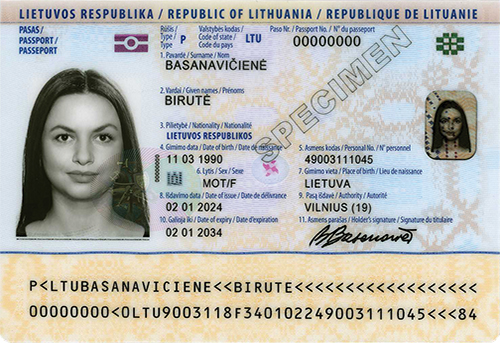

| Passport |

|

| Drivers license |

|

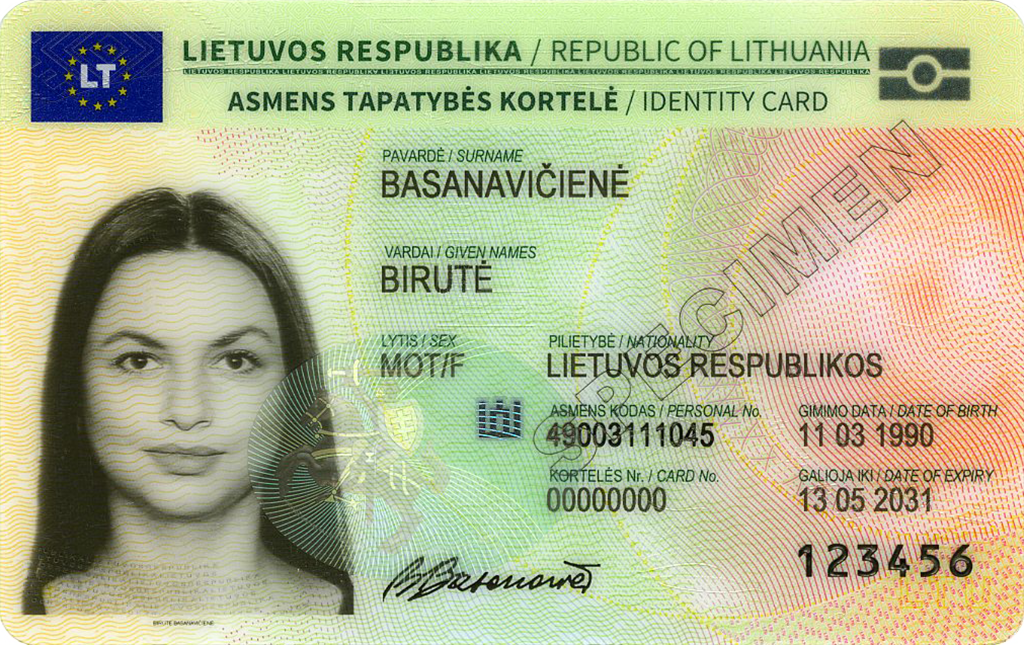

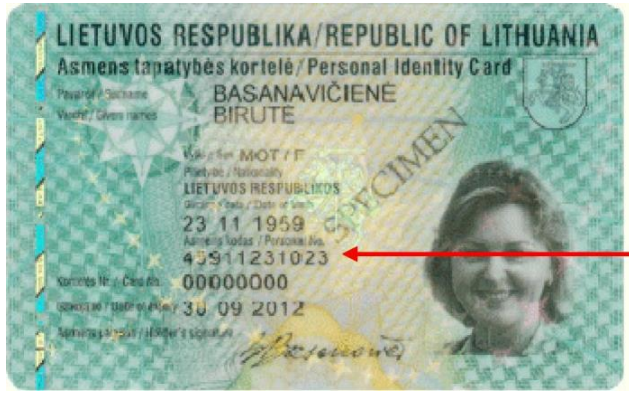

| ID card |

PVM Mokėtojo Kodas (VAT Number)

PVM stands for Pridėtinės vertės mokestis — Lithuania's value added tax. The PVM mokėtojo kodas is the VAT registration number assigned by VMI to businesses registered as VAT payers in Lithuania. It is also referred to as the KMKR (Kodo mokėtojo kodo registras) number in older documents.

Format: LT + 9 or 12 digits

| Format | Used for |

|---|---|

LT + 9 digits (e.g., LT100001738) | Standard legal entities — the 9 digits correspond to the Juridinio asmens kodas |

LT + 12 digits (e.g., LT100001738011) | Natural persons (sole traders / individual activity) and certain non-standard registrants |

The PVM number is verifiable through EU VIES (see how to verify an EU VAT number) or directly on the VMI portal. Lithuanian VAT-registered suppliers must print their PVM number on all issued invoices — omitting it can cause invoice rejection by B2B customers.

VAT Rate: The standard PVM rate is 21%. Reduced rates of 9% and 5% apply to specific goods and services (medicines, books, accommodation).

i.MAS — Lithuania's Mandatory Digital Tax Reporting System

Lithuania operates i.MAS (Intelektualinė mokesčių administravimo sistema — Intelligent Tax Administration System), a real-time digital tax infrastructure that every PVM-registered entity must use. The primary module relevant to most businesses is i.SAF (invoice register).

i.SAF Monthly Invoice Reporting

Every VAT-registered business in Lithuania — including foreign companies with a Lithuanian PVM number — must submit a structured XML invoice register (form FR0600) via i.MAS by the 20th of the month following each transaction month. The file must include all sales and purchase invoices processed under the Lithuanian VAT number. A nil report is mandatory even when no invoices were issued that month.

VMI cross-references i.SAF data against submitted PVM returns automatically. Discrepancies flag the account for audit. Late or missing submissions draw a warning or €200 fine for the first offence, rising to €390 for a repeat within 12 months.

Registration & Compliance Quick Reference

| Scenario | Action required |

|---|---|

| Domestic business, turnover > €45,000 | Register for PVM with VMI before threshold is crossed |

| Foreign EU company making first taxable supply in Lithuania | Register using form FR0388 via Mano VMI at least 3 days before first supply; no threshold |

| Foreign non-EU company | Register via FR0388 and appoint a Lithuanian fiscal representative |

| Small business (SVS, turnover < €45,000) selling B2B services to another EU state | Register for PVM solely for cross-border transactions (since 1 May 2025) |

| Construction subcontractor supplying to VAT-registered main contractor | Issue 0% PVM invoice with "Atvirkštinis apmokestinimas" notation |

For neighboring country comparisons, see the Latvia TIN guide and Estonia TIN guide. For cross-border EU VAT verification, use EU VIES.

Frequently Asked Questions

Does a non-resident company need to register for Lithuanian PVM before its first sale, even if revenue is zero?

Yes. Under Article 71 of Lithuania's Law on Value Added Tax, foreign taxable persons making supplies in Lithuania are subject to no turnover threshold — registration is mandatory before the first taxable transaction. EU companies apply directly to VMI using form FR0388 via the Mano VMI portal at least three days before their first supply. Non-EU companies must additionally appoint a locally resident fiscal representative who is jointly and severally liable for the company's PVM obligations. Failing to register before supplying goods or services triggers penalties of €200–€390 per violation plus interest on any underpaid tax. [1] [2]

From May 2025, when must a Lithuanian small business under the €45,000 SVS exemption register for PVM on cross-border EU services?

Since 1 May 2025, even businesses operating under Lithuania's small-business scheme (SVS) with domestic turnover below €45,000 must register as PVM payers if they supply services to VAT-registered customers in other EU member states or receive services — such as Google Ads or Meta advertising — from foreign suppliers. Registration is done through Mano VMI; the business obtains a PVM number solely for the cross-border transactions and retains its domestic SVS exemption as long as total EU-wide revenue stays below €100,000. This change catches many micro-businesses and freelancers off guard because domestic-only sellers below the threshold face no registration obligation. [3] [4]

Why does a construction subcontractor in Lithuania receive invoices with 0% PVM, and who must account for the VAT?

Lithuania applies a mandatory domestic reverse charge to construction and installation services under Article 96 of the Law on VAT. When a VAT-registered subcontractor supplies construction services to a VAT-registered main contractor in Lithuania, the subcontractor issues an invoice at 0% PVM and writes "Atvirkštinis apmokestinimas" (reverse charge). The main contractor self-accounts for the full 21% PVM as both output and (deductible) input tax. Issuing a standard 21% invoice for these supplies is an error — the recipient will reject it, and the tax authority can impose a penalty of €200–€390 plus require correction. The reverse charge does not apply to supplies to non-VAT-registered clients or to work performed abroad. [5] [6]

What is i.SAF, and what happens if a Lithuanian VAT-registered company misses the monthly submission deadline?

i.SAF is the invoice-register reporting module of Lithuania's i.MAS system. Every PVM-registered entity — including foreign companies registered in Lithuania — must submit an XML file (form FR0600) listing all issued and received VAT invoices by the 20th of the month following the transaction month. A nil report is required even when no invoices were issued. Late or missing i.SAF submissions constitute a tax-law violation: the first offence draws a warning or €200 fine; a second offence within twelve months raises the fine to €390. VMI cross-references i.SAF data against filed PVM returns, so discrepancies also flag accounts for audit. [7] [8]

Can a foreigner living in Lithuania use their Asmens Kodas as their tax identification number, or is a separate TIN required?

For Lithuanian residents and citizens, the Asmens Kodas — the 11-digit personal code issued by the Population Register Service — functions directly as the individual TIN with VMI; no separate tax number is issued. Foreigners who establish Lithuanian residence obtain an Asmens Kodas from Registrų centras and use it across all tax filings and official documents. Non-residents who have no Lithuanian personal code but receive Lithuanian-source income (dividends, rent, etc.) are assigned a separate 10-digit tax identification number by VMI. Banks in Lithuania require the Asmens Kodas to open a standard account; foreigners without one face significant friction, with electronic money institutions such as Paysera offering the main workaround while residence documentation is pending. [9] [10]

How Lookuptax can help you in VAT validation?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.