Cyprus TIN / TIC number guide

This post is also available in: Español

Tax Identification Code (TIC)

The Tax Identification Code (TIC) — locally known as Αριθμός Εγγραφής Φ.Π.Α. (Arithmós Engraphḗs phi.pi.a.) — is the single taxpayer identifier used by the Cyprus Tax Department for income tax, VAT, and all other tax obligations. Every individual and legal entity with a tax presence in Cyprus holds one TIC.

Format: 8 digits followed by one uppercase Latin letter (total 9 characters). Example: 99999999L.

Starting-digit conventions:

- Individuals (natural persons) — first digit is

0or9for pre-March 2023 TICs; all new TICs issued since 27 March 2023 begin with6(e.g.,60012345A). - Legal entities — first digit is

1.

The check character (the trailing letter) is derived from a MOD-26 lookup-table algorithm. Numbers beginning with 12 are reserved and should be treated as invalid.

The TFA change (27 March 2023): The Tax Department migrated all new registrations to the Tax For All (TFA) system and began assigning TICs from 60000000 onward under a revised check-character algorithm. Pre-existing TICs starting with 0 or 9 remain equally valid — only the assignment range and algorithm details differ. Validation tools built before 2023 commonly reject 6XXXXXXX numbers because they have not been updated.

VAT relationship: For entities registered for VAT, the VAT number is simply the TIC prefixed with the country code CY (e.g., CY99999999L). The VAT registration threshold for businesses established in Cyprus is EUR 15,600 of annual taxable turnover. Non-resident businesses have no threshold — liability arises from the first euro of taxable supply in Cyprus.

|  |

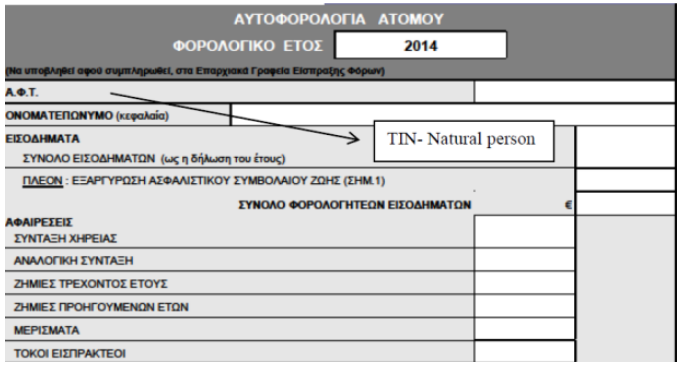

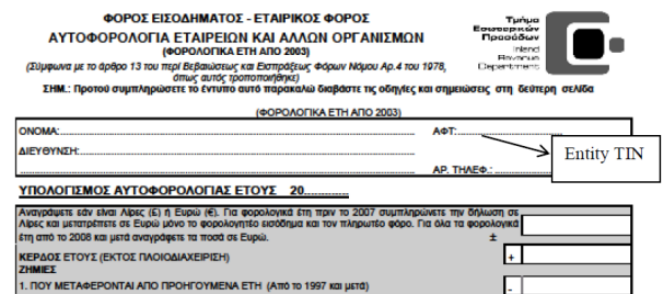

| TIN Individuals on income tax return | TIN Entities on tax assessment |

How to Register for a TIC

Registration is handled exclusively through the TFA Taxpayer Portal at taxforall.mof.gov.cy. Paper applications at district tax offices were discontinued in January 2024.

Residents must create a TFA account, then submit:

- Form T.D. 2001 (online)

- Certified copy of passport or national ID

- Proof of Cyprus address (utility bill, tenancy agreement, or property title deed)

Non-residents follow the same online process but instead of a Cyprus address document must supply:

- An official document from their home country showing their foreign tax code or national ID number

- A personal photo

- A letter explaining the reason for the Cyprus TIC request

Processing typically takes one to six weeks. The TFA Helpdesk can be reached at +357 22803803 (international) or [email protected].

Portal availability: The TFA platform has undergone several maintenance windows — including a nine-day full shutdown in August 2025 — during which new registrations are suspended. Always check the TFA announcements page before submitting time-sensitive applications. Since 22 August 2025, login requires a CY Login (formerly Ariadne) account.

TIC and Non-Dom Status

Cyprus offers a non-domiciled (non-dom) tax resident regime that exempts qualifying individuals from Special Defence Contribution (SDC) on dividends, interest, and rental income for up to 17 out of 20 consecutive years of Cyprus tax residency. Non-dom status is not automatic: Form TD624 must be filed with the district tax office in the first year passive income is received.

From 1 January 2026, the 60-day tax residency rule no longer bars applicants who are already tax resident in another country, following amendments enacted on 22 December 2025.

Corporate Tax Changes (2026)

Cyprus raised its headline corporate income tax rate from 12.5% to 15% from 1 January 2026 to comply with the OECD Pillar Two global minimum tax. The IP Box (2.5% effective rate) and Notional Interest Deduction on new equity remain in place. The deemed dividend distribution mechanism is abolished for profits earned from FY2026 onward.

Related Resources

- Greece TIN number guide — neighboring EU member, similar VIES validation workflow

- Malta TIN number guide — fellow small EU island jurisdiction, useful for comparison

- Guide to the VAT One Stop Shop (OSS) — how EU and non-EU digital sellers avoid separate Cyprus VAT registration

- VIES and INTRASTAT guide for EU traders — verifying Cyprus CY-prefixed VAT numbers via VIES

- Reverse charge mechanism explained — applies to B2B cross-border supplies into Cyprus

Frequently Asked Questions

Why does my Cyprus TIC starting with 6 get rejected by older validation tools?

Starting 27 March 2023, the new TFA system issues TICs beginning from 60000000 with a revised check-character algorithm. Older TICs began with 0 or 9 under a different scheme. Both formats are equally valid — only the assignment range and checksum logic differ. [1] [2] If a counterparty system rejects a TIC starting with 6, the root cause is an outdated regex or checksum library that has not been updated to recognise the 6XXXXXXX range. Ask your software vendor or API provider to update their Cyprus TIN validation rules to accept first digits of 0, 1, 6, and 9.

Can I register for a Cyprus TIC online if I have no Cyprus address?

Yes — non-residents can register entirely through the TFA portal without a Cyprus address. Instead of a utility bill or tenancy agreement, you supply an official document from your home country showing your foreign tax code or national ID, plus a letter stating the reason for registration. [3] [4] The most common reason accepted is property purchase in Cyprus (supported by a stamped sale-and-purchase agreement), employment by a Cyprus entity, or directorship of a Cyprus company. Processing takes one to six weeks; if rejected, you may appeal in writing to [email protected] or file a formal objection with the Commissioner of Taxation within 60 days.

The TFA portal was down when I needed to register — can I still meet my VAT deadline?

The Cyprus Tax Department extended deadlines (for example, the June 2025 VIES return was extended to 29 July 2025) to compensate for the July 2025 shutdown. [5] [6] When the TFA system is unavailable during a maintenance window, check the official announcements section at gov.cy/mof-tfa for any deadline extensions. If no extension is announced and your deadline is imminent, contact the TFA Helpdesk at +357 22803803 before the deadline to document that you attempted to comply — this can support a reasonable-excuse argument if a late-registration penalty of EUR 85 per month is later assessed.

Do non-resident companies selling digital services to Cyprus consumers need a local VAT registration?

There is no turnover threshold for non-established traders — VAT liability in Cyprus begins from the first euro of B2C taxable supply. [7] [8] However, EU-based sellers can avoid a direct Cyprus registration by using the Union OSS once EU-wide B2C digital sales exceed EUR 10,000 — reporting Cyprus VAT at 19% through a single return in their home member state. Non-EU businesses that register directly in Cyprus must appoint a locally resident fiscal representative who is jointly liable for all VAT, penalties, and interest. Failure to register before making the first taxable supply exposes the business to a EUR 85-per-month late-registration penalty.

My B2B customer says my CY VAT number is invalid on VIES — but the Cyprus Tax Department says it is active. Who is right?

The VIES system pulls data from national registers but is regularly overloaded during business hours and may return stale or unavailable data for Cyprus. [9] [10] An "invalid" VIES result does not mean the number is fraudulent — it may simply mean Cyprus has not yet synchronised the record or the VIES query timed out. Practical steps: retry the VIES check at off-peak hours; ask your customer to verify directly through the Cyprus Tax Department TFA portal; and keep a screenshot of the positive TFA result as documentary evidence of due diligence. For reverse-charge zero-rated sales you must make reasonable efforts to verify VAT status — a failed VIES query combined with a positive official-portal result is widely accepted as sufficient.

How do I claim non-dom status in Cyprus to exempt dividends and interest from Special Defence Contribution?

Non-domiciled status is not automatic — you must file Form TD624 with your district tax office in the first year you receive dividends, interest, or rental income in Cyprus. [11] [12] The exemption covers SDC on those passive income streams for up to 17 out of 20 consecutive years of Cyprus tax residency; General Healthcare System contributions still apply. From 1 January 2026, the former restriction that barred applicants who were already tax resident elsewhere was removed — you can now hold dual tax residency and still qualify for the 60-day Cyprus residency test. Retain documentary evidence of your domicile of origin (birth certificate, records of long-term residence abroad, foreign property ownership) as the Tax Department may request proof at any time.

How Lookuptax can help you ?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.