Hong Kong TIN — HKID and Business Registration (BR) Number Guide

This post is also available in: Español

Hong Kong does not operate a standalone TIN system. Instead, the Inland Revenue Department (IRD) uses two pre-existing identifiers as the functional equivalents of a Tax Identification Number: the Hong Kong Identity Card (HKID) number for individuals and the Business Registration (BR) number for entities. Both are recognised as Hong Kong's TINs under the OECD's Common Reporting Standard (CRS) and AEOI frameworks.

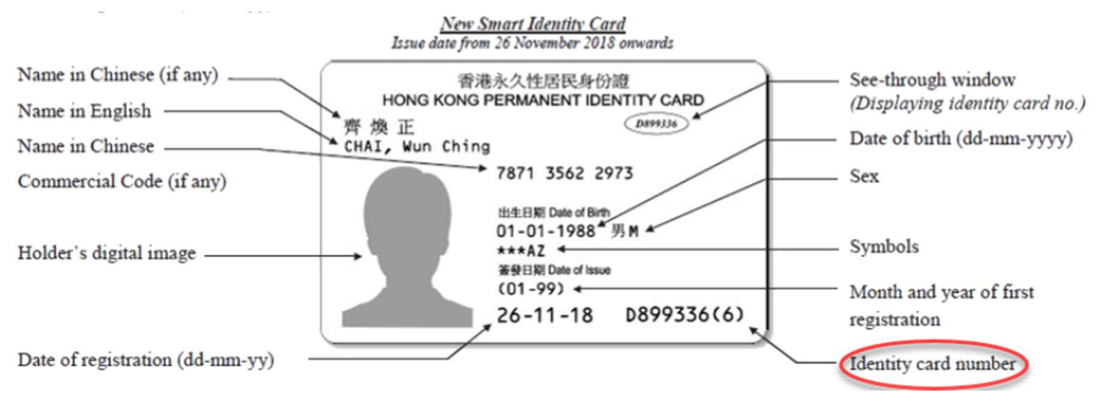

Hong Kong Identity Card (HKID) Number

The HKID is issued by the Immigration Department and is mandatory for all residents aged 11 and above, with limited exemptions. It functions as the individual TIN for salaries tax filings, CRS self-certifications submitted to banks, and all cross-border tax reporting.

Format

The HKID follows the pattern @123456(#):

@— one or two capital letters (prefix assigned by the Immigration Department based on issuance batch)123456— six digits(#)— a check character in parentheses; values range from0to9andA

When supplying your HKID as a TIN — for example, on a bank CRS form or a tax return — omit the parentheses and write it as a continuous string, e.g. X123456A. Including or omitting brackets is the most common input error.

Check-Digit Algorithm

The check character is calculated using a weighted-sum method:

- Convert each letter to its positional value (A = 10, B = 11 … Z = 35). A single-letter prefix is padded with a space, which maps to 36.

- Multiply each character by its weight (9 for the first position, down to 2 for the last digit before the check character).

- Sum the results. The check character is

(11 − (sum mod 11)) mod 11, where a remainder of 10 maps toAand 0 maps to0.

Multiple open-source implementations exist for developers; the Immigration Department also publishes a check-digit verifier at webb-site.com.

|

| HKID — individual TIN equivalent |

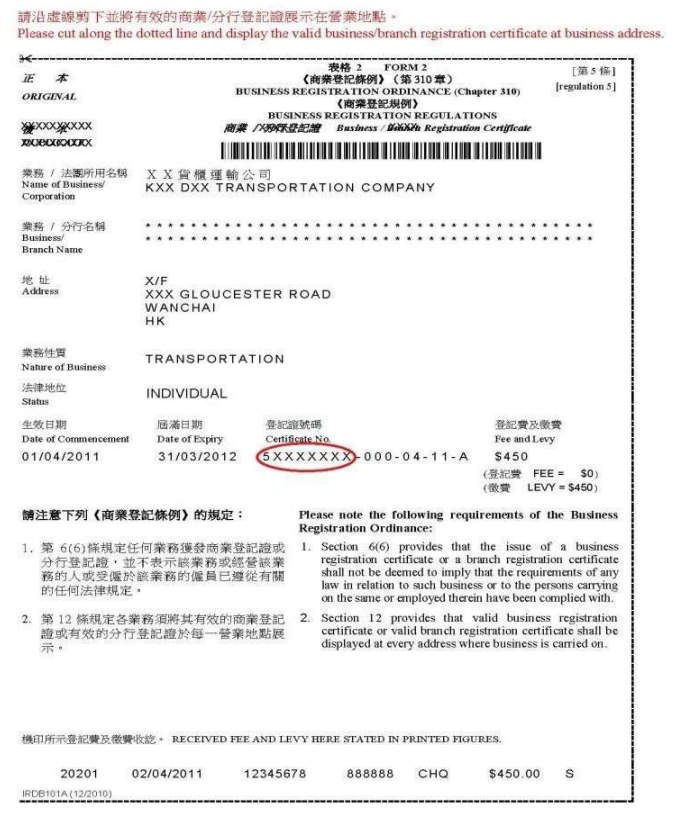

Business Registration (BR) Number

Every person who carries on a business in Hong Kong — including sole proprietors, partnerships, and incorporated companies — must register with the Business Registration Office of the IRD within one month of commencing operations and display a valid Business Registration Certificate at the place of business.

The BR number is the entity-level TIN equivalent, used for profits tax, employer returns, CRS entity self-certifications, and B2B invoice verification.

Format

The Business Registration Certificate number has the structure 99999999-&&&-&&-&&-&. The BRN (Business Registration Number) is solely the first 8 digits — a contiguous string of numerals with no letters or special characters (e.g. 12345678). The suffix segments encode renewal period and branch information and are not part of the TIN.

Unique Business Identifier (UBI) Reform — December 2023

From 27 December 2023, the Companies Registry replaced the former 7-digit Company Registration Number (CRN) with the BRN as the single Unique Business Identifier (UBI) across all government departments. Businesses incorporated before that date retain their existing 8-digit BRN; the CR number is no longer issued and older certificates showing a CRN are superseded. A mapping lookup between former CRN and current BRN is available via the Companies Registry e-Services Portal.

Online Verification

The IRD provides a free Business Registration Number Enquiry service via GovHK. Search by business name (English or Chinese) and location (Hong Kong Island, Kowloon, or New Territories) to retrieve the BRN. No login is required.

Official database — BR Enquiry

|

| BR number on business registration certificate — the 8-digit BRN is the entity TIN |

eTAX Login TIN vs. the Actual TIN

The IRD issues a separate "TIN (for eTAX login)" printed on individual tax returns and assessments. This number is only a portal credential — it is not valid for CRS/AEOI reporting or bank self-certifications. When a Hong Kong financial institution asks for your TIN, supply your HKID (individual) or BRN (entity), not the eTAX login TIN.

Internet and Digital Businesses

A person who conducts trading activities or provides services through the internet, where those activities are carried out in Hong Kong, must apply for business registration in the same way as a traditional business. The IRD assesses whether internet operations constitute "carrying on a business in Hong Kong" by examining procurement, promotion, delivery, and settlement activities. Non-compliance carries the same HKD 5,000 fine and up to one year's imprisonment as any other registration failure.

Frequently Asked Questions

Why does my HKID number get rejected when I enter it as my TIN on a bank CRS form?

The most common cause is including the parentheses around the check character. The HKID is physically printed as X123456(A) but must be entered without brackets — as X123456A — when used as a TIN on CRS self-certifications and tax forms. A second cause is accidentally using the "TIN for eTAX login" (printed on individual tax returns) instead of the HKID itself; the eTAX login TIN is a portal credential only and is not a valid CRS identifier. [1] [2]

What is the difference between the BR number and the old Company Registration Number (CRN) — which one do I use?

Since 27 December 2023, the 8-digit Business Registration Number (BRN) has replaced the former 7-digit Company Registration Number as the Unique Business Identifier (UBI) for all Hong Kong entities across government departments and registries. If your documents still show a CRN, use the Companies Registry's CR No./BRN Mapping lookup to find the corresponding BRN — that is the number to quote on tax filings, invoices, and CRS certifications. Do not use the old CRN for any new submissions. [1] [2]

Does a foreign company selling services online to Hong Kong customers need to register for business registration?

Yes, if the commercial activities — procurement, promotion, delivery, or settlement — are carried out in Hong Kong. The IRD applies a facts-and-circumstances test to internet businesses; operating a website hosted outside Hong Kong does not by itself exempt a business from registration if the substantive activities occur locally. A foreign company with no Hong Kong nexus is generally not required to register. There is no consumption-tax or GST/VAT system in Hong Kong, so there is no digital-services tax registration obligation analogous to those in the EU or Australia. [1] [2]

What is the penalty for missing the Business Registration renewal deadline in Hong Kong?

Failing to apply for business registration within one month of commencing operations, or failing to renew on time, is a criminal offence under the Business Registration Ordinance (Cap. 310). The maximum penalty is a fine of HKD 5,000 and up to one year's imprisonment. The IRD first adds a HKD 300 surcharge to an overdue demand note; persistent non-payment escalates to prosecution. The obligation to renew on time rests with the business owner regardless of whether the renewal notice is received. [1] [2]

Why does my Hong Kong company receive two large tax demands at the same time?

Hong Kong levies provisional profits tax — an advance payment based on the prior year's assessable profits — in addition to the final assessment for the preceding year. The provisional tax is split into two instalments: 75% is typically due in the final quarter of the tax year, and the remaining 25% is due three months later. This means a company can be required to pay the prior year's final tax and the current year's first provisional instalment (75%) simultaneously, creating a significant cash-flow burden. If current-year profits are expected to fall by more than 10%, a holdover application (Form IR1121) must be submitted at least 28 days before the payment due date to defer the provisional charge. [1] [2]

Can a Hong Kong MNE entity still claim offshore income exemption after the 2023 FSIE reforms?

Yes, but only if the entity satisfies additional substance tests introduced by Hong Kong's Foreign-sourced Income Exemption (FSIE) regime. From 1 January 2023, foreign-sourced interest, dividends, and IP income received in Hong Kong by a member of a multinational enterprise (MNE) group are chargeable to profits tax unless the entity meets the economic substance requirement (adequate staff, premises, and operating expenditure in Hong Kong), the participation requirement, or the nexus requirement for IP income. From 1 January 2024, the regime expanded to cover gains from disposal of all asset types. Entities that fail all three tests are taxed on the full amount of the in-scope income. [1] [2]

What withholding tax rate applies when a Hong Kong company pays royalties to a non-resident related party?

The rate depends on whether the Hong Kong payer has ever owned the intellectual property and whether the recipient is an associate. For an unrelated non-resident corporation, only 30% of the gross royalty is treated as assessable profit, giving an effective withholding rate of 4.95% (30% × 16.5%). If the Hong Kong payer has at any time wholly or partly owned the IP and the non-resident recipient is an associate, 100% of the royalty is deemed assessable profit — raising the effective rate to 16.5% on the full gross amount. The payer must remit the withheld tax to the IRD within one month using Form BIR54; missing this deadline triggers an automatic 5% surcharge. [1] [2]

When must an employer enroll a foreign employee in Hong Kong's MPF scheme if their visa is extended beyond 13 months?

Foreign employees who enter Hong Kong under Section 11 of the Immigration Ordinance for employment are exempt from MPF enrollment for up to 13 months, provided they are not already members of an overseas retirement scheme. The exemption is calculated cumulatively: if an employee's initial 9-month visa is extended by 6 months, the combined stay exceeds 13 months and the exemption ends on the first day after the 13th month. The employer must then enroll the employee in an MPF scheme within 60 days of that date. Failure to enroll on time carries a maximum penalty of HKD 350,000 and three years' imprisonment. [1] [2]

Related Resources

- Singapore TIN number guide — UEN and NRIC as TIN equivalents in a comparable regional financial hub

- China TIN number guide — USCC, Citizen ID, and Golden Tax system for Greater China context

- Macao TIN number guide — the other SAR TIN system

- Worldwide directory of VAT and tax ID names — local names and formats across 100+ countries

- VAT registration thresholds worldwide — understand where Hong Kong's no-VAT position sits globally

How Lookuptax can help you in VAT validation?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.