Turkey TIN number guide

National Identification Number

Since July 1, 2006, the National Identity Number serves as the unique identifier for Turkish citizens, and all Tax Identification Numbers (TINs) for citizens have been aligned with their National Identification Numbers in the tax database system. Foreigners residing in Turkey for more than six months are also mandated to acquire a TIN. If available, foreign nationals can alternatively utilize their Foreign Identity Numbers instead of a TIN.

The issuance of the Tax Identification Number is based on identification information obtained through central taxpayer registry files. TINs are provided to legal entities, legal entities with no tax liability, foreign nationals lacking a Foreign Identity number, and foreign legal entities.

National Identity Number consists of 11 digits different than the 10 digit TIN.

|

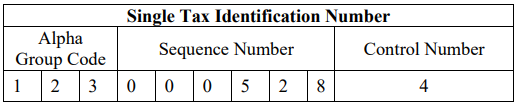

| NIN Format |

Alpha Group Code: For individuals: Code including their surname and name (between 001-999) For legal entities and ordinary partnerships: Code including their title (between 001-999)

Sequence Number: Sequence number of Alpha Group Code in Türkiye

Control Number: Check-digit of 9 characters consisting of Alpha Group Code and Sequence Number

Vergi Kimlik Numarası

"Vergi Kimlik Numarası" is Turkish for "Tax Identification Number".

It is a unique number assigned by the Revenue Administration to individuals and entities for identification in tax-related affairs in Turkey. Some key points about Vergi Kimlik Numarası:

- It consists of 10 digits - first digit is always 9 for companies, and starts with 1, 2, 3, 4 for individuals

- Companies must register for a Vergi Kimlik Numarası within 30 days of incorporation

- Required for paying taxes, on invoices, for government procedures like tenders etc

- Displayed on tax returns, tax payment forms

- Links a person or company to all their tax affairs and records with the Revenue Administration

- Helps government track tax compliance

So in essence, it serves a similar purpose as VAT registration numbers in Europe or Tax ID numbers in the USA - unique identification for tax administration purposes.

Frequently Asked Questions

My MERSIS company registration keeps failing — the Trade Registry rejects my foreign shareholder's passport data. Why?

MERSIS performs a strict character-by-character match between the data you enter and official identity documents. For non-Turkish shareholders, the most common rejection cause is a mismatch involving Turkish dotted characters: the system treats "I" (ASCII) and "İ" (Turkish dotted capital I) as different characters, so a passport name with "I" typed on a standard keyboard fails if the underlying identity record expects "İ". Every field — full legal name, nationality, foreign tax number, address, and shareholding percentage — must be an exact copy of the passport's machine-readable zone (MRZ). A single character error suspends the entire application and requires resubmission from scratch, blocking your ability to open a bank account or issue invoices until the VKN is issued. [1] [2]

Do foreign B2C digital service providers need to register for KDV in Turkey even without a local entity?

Yes, with no minimum revenue threshold. Turkey has required non-resident providers of electronic services to Turkish consumers (B2C) to register with GİB's dedicated Digital Services VAT Office since 2018. There is no registration threshold: the obligation applies from the first sale to a Turkish consumer, regardless of your company's size or location. Registration is done entirely online at the dedicated portal without obtaining a full VKN. B2B sales where the Turkish customer accounts for VAT via the reverse-charge mechanism (KDV-2) are excluded, but mixed B2C/B2B sellers must register for the B2C portion. Failure to register exposes you to back-taxes, interest, and penalties collected through digital platform intermediaries. [3] [4]

Is withholding tax (stopaj) deducted from payments Turkey makes to foreign software and SaaS vendors?

Yes. Under Article 94 of the Income Tax Law (GVK) and Article 30 of the Corporate Tax Law, Turkish companies must withhold 20% stopaj on payments for professional services — including software licences, SaaS subscriptions, and technical consultancy — made to non-resident entities. The Turkish payer remits the tax directly to GİB and pays the foreign vendor only 80% of the invoiced amount. If your country has a Double Taxation Agreement (DTA) with Turkey, the treaty rate (often 10% or 0% for royalties/services) overrides the domestic 20%, but only if you supply a current Certificate of Tax Residence before payment is made. Without this certificate your client is legally obligated to apply the full domestic rate. [5] [6]

Which companies are legally required to switch to e-Fatura (and e-Arşiv), and what is the current turnover threshold?

Under VUK General Communiqué No. 509 (as amended by Communiqué No. 573, Official Gazette 32720, November 2024), companies whose gross revenue in the 2024 fiscal year exceeded TRY 3 million must join the e-Fatura system by 1 July 2025. A lower threshold of TRY 500,000 applies to e-commerce operators, real estate traders, and motor vehicle dealers. Companies not yet required to issue e-Fatura must still issue e-Arşiv invoices for any single invoice exceeding TRY 5,000 or when total daily invoices to a single recipient exceed TRY 30,000. Issuing a paper invoice where e-Fatura is mandatory exposes the taxpayer to a "special irregularity penalty" (özel usulsüzlük cezası) under VUK Article 355. [7] [8]

Can a non-resident foreign company reclaim Turkish input VAT (KDV) it paid on local purchases?

Only in limited circumstances governed by reciprocity. Turkey allows VAT refunds to foreign businesses under KDV Law Article 9 and related regulations, but only if the company's home country grants equivalent refund rights to Turkish businesses. In practice, very few countries meet Turkey's reciprocity test. Even where reciprocity applies, refundable expenses are restricted to a defined list: trade-fair participation costs, fuel, vehicle spare parts, maintenance, and motorway tolls. General operating costs — hotels, consultancy, equipment — are not refundable. A foreign company that has registered for Turkish VAT and has a local VKN cannot use this route; it must offset input VAT on its periodic KDV returns in the normal way. Non-residents with no Turkish registration and in non-reciprocal countries cannot recover input VAT at all. [9] [10]

How Lookuptax can help you ? Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.