South Korea Tax ID Guide — RRN, BRN & CRN

This post is also available in: Español|中文

South Korea operates three distinct tax identification number systems managed by two separate authorities: the Ministry of the Interior (for individuals) and the National Tax Service (NTS) district tax offices (for businesses). Understanding which number applies to your situation — and where it must appear on official documents — prevents invoice rejections, withheld payments, and NTS filing errors. This guide covers all three systems: the Resident Registration Number (RRN), the Business Registration Number (BRN), and the Corporation Registration Number (CRN).

Resident Registration Number (주민등록번호)

The Resident Registration Number (RRN) is issued by the Ministry of the Interior to Korean citizens residing in the country. It serves as the primary individual tax identifier for income tax returns, transfer tax, inheritance tax, and gift tax filings. Employers also reference it when calculating and remitting withholding tax on wages and salaries. [1]

For Common Reporting Standard (CRS) reporting purposes, a Passport Number issued by the Ministry of Foreign Affairs is accepted as an alternative TIN for Korean nationals residing abroad or non-resident individuals without an RRN.

|

| Resident Registration Card |

Format and Structure

The RRN is a 13-digit number formatted as XXXXXX-XXXXXXX.

| Field | Detail |

|---|---|

| Total length | 13 digits |

| Format | DDMMYY-NSSSSSC |

| Digits 1–6 | Date of birth (YYMMDD) |

| Digit 7 | Gender and century code (1/2 = 1900s male/female; 3/4 = 2000s male/female; 5/6 = foreign nationals 1900s; 7/8 = foreign nationals 2000s) |

| Digits 8–12 | Region of registration and sequential serial number |

| Digit 13 | Check digit (Luhn-style weighted checksum) |

| Example | 850102-1234567 (male born 2 January 1985) |

The seventh digit encodes both gender and birth century, which is why "0" is never used — values run from 1 through 9, with higher values reserved for foreign nationals and overseas Koreans.

Privacy Restrictions

Since August 2014, the Personal Information Protection Act (PIPA) prohibits any person or entity from collecting or processing an RRN without an explicit statutory basis. Consent alone is not sufficient. For online identity verification, businesses must use surrogate methods such as IPIN, mobile carrier verification, or digital certificates instead of requesting an RRN directly.

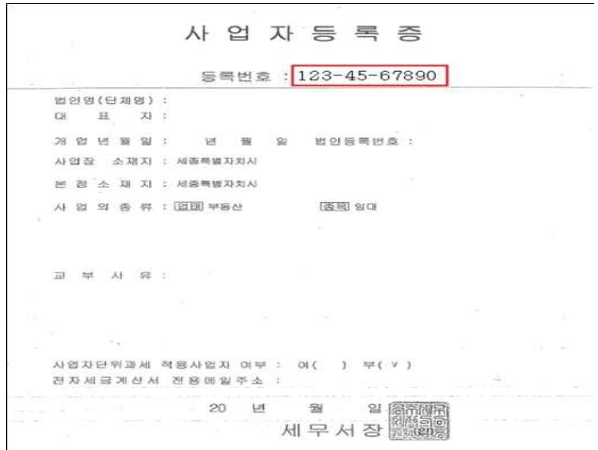

Business Registration Number (사업자등록번호)

The Business Registration Number (BRN) is issued by the head of a district tax office under the National Tax Service (NTS). It is the primary tax identifier for all NTS filings, including VAT returns, corporate income tax returns, and withholding tax submissions. Any entity starting a business in South Korea must register and obtain a BRN before commencing operations. [2]

|

| Business Registration Certificate (사업자등록증) |

Format and Structure

| Field | Detail |

|---|---|

| Total length | 10 digits |

| Format | XXX-XX-XXXXX |

| Digits 1–3 | District tax office code |

| Digits 4–5 | Business type code (01–79 = individual; 81–84 = corporation) |

| Digits 6–9 | Registration sequence number |

| Digit 10 | Check digit |

| Example | 123-45-67890 |

Verification

The NTS provides a free online BRN verification tool through the Hometax portal. You can confirm whether a BRN is active and matches a registered entity before issuing or accepting a tax invoice. This is essential for B2B transactions — an inactive or invalid BRN means the recipient cannot claim input VAT. [2]

Electronic Tax Invoice Obligations

Korean law requires VAT-registered businesses to issue electronic tax invoices (전자세금계산서) through the NTS Hometax system. Corporations have been subject to this requirement since 2011. For sole proprietors (개인사업자), the threshold has been progressively lowered: KRW 300 million (before July 2023), KRW 100 million (July 2023 – June 2024), and KRW 80 million (from July 2024). Any sole proprietor whose prior-year taxable supply value met or exceeded KRW 80 million must now issue electronic tax invoices for all VAT-liable supplies. [3]

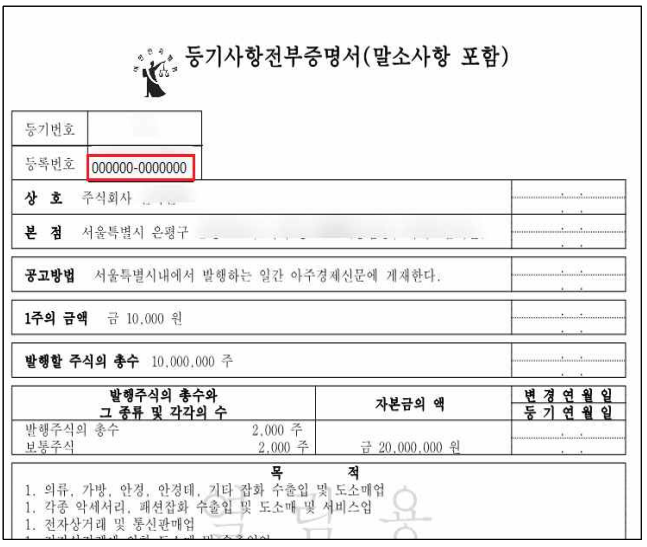

Corporation Registration Number (법인등록번호)

When a legal entity registers its foundation with the court, it receives a Corporation Registration Number (CRN) managed by the Supreme Court's registry. The CRN proves legal existence and is distinct from the BRN issued by the NTS. While the CRN is accepted as a TIN in CRS and FATCA reporting contexts, it is not a valid tax invoice identifier. [1]

|

| Certified Copy of the Corporation Registry |

Format and Structure

| Field | Detail |

|---|---|

| Total length | 13 digits |

| Format | XXXXXX-XXXXXXX |

| Issuing authority | Supreme Court Registry (법원) |

| Used on tax invoices | No — BRN required instead |

| Accepted as TIN in | CRS/FATCA reporting |

| Example | 110111-1234567 |

A newly incorporated foreign subsidiary often confuses these two numbers. The court registry extract shows the CRN; the NTS-issued Business Registration Certificate (사업자등록증) shows the BRN. Always request the BRN from the certificate, not the court document.

Which Number Goes Where

| Context | Required Number |

|---|---|

| Korean electronic tax invoice (전자세금계산서) | BRN |

| VAT return filing via Hometax | BRN |

| Corporate income tax return | BRN |

| Withholding tax on employee wages | RRN (employee) + BRN (employer) |

| CRS/FATCA financial account reporting | RRN or CRN or Passport Number |

| Court registry filings and legal existence | CRN |

Foreign Businesses and Korean VAT

Foreign companies without a Korean legal entity selling digital services (software, cloud, streaming, online advertising) to Korean consumers must register with the NTS under the Simplified Business Operator (간편사업자 등록) scheme. Korea applies a zero-threshold rule — registration is required before the first B2C sale. The VAT rate is 10%, with quarterly filing deadlines on the 25th of the month following each quarter. [4]

B2B supplies to Korean businesses that self-account under the reverse charge mechanism do not require the foreign supplier to register, but you must verify the Korean buyer's BRN to confirm B2B status.

For a broader overview of how VAT registration works across jurisdictions, see the VAT and GST registration guide. For comparison with a similar Asia-Pacific system, the Japan Tax ID Guide covers My Number and Corporate Number rules including the Qualified Invoice system.

Frequently Asked Questions

Can a Korean business legally collect my RRN (주민등록번호) for a routine commercial transaction?

No. Since August 2014, the Personal Information Protection Act (PIPA) prohibits any person or entity from collecting or processing a Resident Registration Number (RRN) without an explicit legal basis — consent alone is not sufficient. [5] Unauthorized collection carries a fine of up to KRW 30 million; failure to protect an RRN that was lawfully collected exposes the processor to a fine of up to KRW 500 million. Under February 2026 PIPA amendments, repeat or large-scale violations (affecting 10 million or more individuals, or within three years of a prior violation) now attract administrative fines of up to 10% of total annual revenue. [6] Businesses must instead use surrogate identification methods (IPIN, mobile verification, or digital certificate) for online identity checks. If a commercial vendor demands your RRN for a purpose with no statutory basis — such as a loyalty programme sign-up — you may refuse and file a complaint with the Personal Information Protection Commission (PIPC).

What is the difference between a Business Registration Number (BRN) and a Corporation Registration Number (CRN), and which one must appear on a Korean tax invoice?

These are two separate identifiers issued by different authorities. The Business Registration Number (사업자등록번호) is a 10-digit number (XXX-XX-XXXXX) issued by the district tax office under the NTS — it is the primary tax identifier for all VAT, corporate tax, and withholding filings. [2] The Corporation Registration Number (법인등록번호) is a 13-digit number (XXXXXX-XXXXXXX) issued by the court registry when a legal entity is incorporated; it proves legal existence and is accepted as a TIN in CRS/FATCA contexts, but it is not a tax invoice field. On Korean electronic tax invoices (전자세금계산서) and all NTS filings, only the BRN is valid. Entering only the CRN is a common error among newly incorporated foreign subsidiaries and will cause the recipient's input VAT claim to be rejected. Always obtain the BRN from the NTS-issued Business Registration Certificate (사업자등록증), not from the court registry extract. [1]

I run a foreign SaaS business with no Korean entity. Do I need to register for Korean VAT before my first B2C sale?

Yes — Korea applies a zero-threshold rule for non-resident digital service providers. There is no minimum turnover exemption: registration via the NTS Hometax "Simplified Business Operator" scheme (간편사업자 등록) is mandatory before the first B2C sale of electronic services (software, cloud, streaming, online advertising) to a Korean consumer. [4] Once registered, you charge 10% VAT and file quarterly returns by the 25th of the month following each quarter. A penalty of 1% of total supply value applies for failure to register on time, accruing up to the day simplified registration is completed — meaning a foreign provider who has been selling to Korean consumers for two years without registration faces significant back-penalties on top of uncollected VAT. B2B supplies where the Korean business self-accounts under reverse charge do not require the foreign supplier to register, but you must verify the buyer's BRN to confirm B2B status. From 1 July 2025, foreign digital intermediary platforms must also submit quarterly transaction-detail reports to the NTS under Article 75 of the VAT Law. [4]

My Korean sole proprietorship just crossed KRW 80 million in annual sales. Must I now issue electronic tax invoices, and what are the penalties for missing the transmission deadline?

Yes. Since July 2024, sole proprietors (개인사업자) whose previous-year supply value reached KRW 80 million or more must issue electronic tax invoices (전자세금계산서) for all VAT-liable supplies, regardless of whether they are general or simplified VAT taxpayers. [3] This threshold was progressively lowered from KRW 300 million to KRW 100 million (July 2023) and then to KRW 80 million (July 2024), so businesses that were exempt two years ago may be non-compliant today without realising it. Corporations have been subject to mandatory e-invoicing since 2011. Invoices must be transmitted to the NTS via Hometax on the day of issuance; a monthly bulk submission by the 10th of the following month is the absolute latest. Penalties are graduated: 2% of supply value for failing to issue any invoice; 1% of supply value for issuing on paper or failing to transmit to the NTS by the 10th. [7] Pre-enrol in the Hometax e-invoicing module before the obligation activates — enrolment takes several working days.

As a foreign employee in Korea, should I elect the 19% flat income tax rate during year-end settlement (연말정산), or use the progressive tax rates?

Foreign workers who began employment in Korea by 31 December 2026 may elect a flat income tax rate of 19% (plus 1.9% local income tax) on employment income in lieu of the standard progressive rates of 6%–45%. [8] The critical trade-off: electing the flat rate forfeits all other income deductions, tax exemptions, and tax credits — including the earned income deduction, dependent deductions, and insurance premium credits that Korean taxpayers use to reduce their effective rate. The flat rate is advantageous primarily for high earners whose marginal progressive rate exceeds 19%, and it is unavailable if the employee works for a related-party company (as defined by the tax authority). [8] The election must be submitted to the employer at the time of year-end settlement or to the NTS at annual return filing; the NTS publishes a multilingual Year-End Tax Settlement guide (available in English, Chinese, and Vietnamese) for foreign residents each January.

Related Resources

- Japan Tax ID Guide — My Number & Corporate Number — Japan's comparable dual-number system with Qualified Invoice compliance rules

- China TIN Guide — USCC, Citizen ID & Tax Registration — 18-character Unified Social Credit Code and individual resident ID

- Singapore TIN Guide — UEN and NRIC/FIN system for the region's major financial hub

- What is Reverse Charge? — How Korean B2B digital service transactions shift VAT liability to the buyer

- How to Register for VAT, Sales Tax, and GST — Country-by-country registration guide including Korea's Simplified Business Operator scheme

How Lookuptax can help you in VAT validation?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.