Liechtenstein Tax ID Guide — PEID, FL-Steuernummer, and MWST/UID Numbers

Liechtenstein uses three distinct tax identifiers that serve separate purposes — confusing them on invoices or tax filings is a common and costly mistake for both domestic businesses and foreign companies entering the market. This guide explains each identifier, its format, and when it is required.

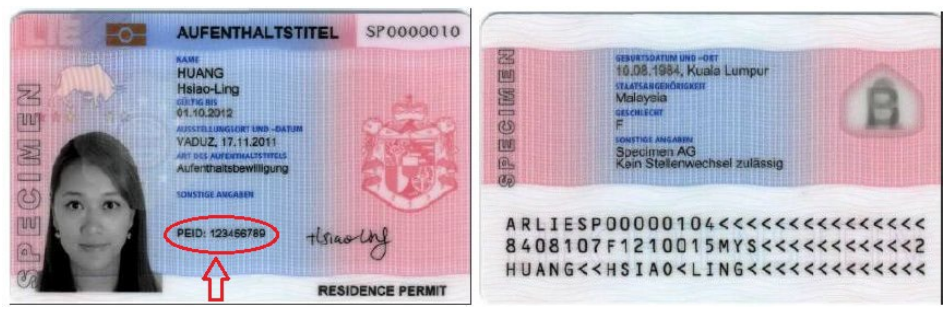

PEID Nummer (Personenidentifikationsnummer)

The PEID Nummer is the master tax identification number in Liechtenstein, used for both natural persons (individuals) and legal entities. "PEID" stands for Personenidentifikationsnummer — the person identification number. It is issued by the Liechtenstein Office of Statistics (Amt für Statistik) and serves as the primary identifier on income tax returns, payroll records, employer census reports, and AEOI (automatic exchange of information) submissions.

Format

The PEID Nummer is a purely numeric string of up to 12 digits. Leading zeros are omitted, which means the displayed length varies:

| Length | When it occurs |

|---|---|

| 12 digits | Full format: 999999999999 |

| 7 digits | Leading zeros stripped from shorter sequences |

| 4 digits | Shortest assigned block after stripping leading zeros |

There are no separators, no country prefix, and no check digit in the standard PEID format used domestically. On wage certificates (Lohnausweis) and employer reports, the employee's PEID must be entered in the designated field — omitting it causes rejection by the Liechtenstein Tax Administration (Steuerverwaltung).

Example: 999999999999

Official search database: PEID search — Handelsregister Liechtenstein

|

| Residence permit for foreigners |

|

| Residence permit for cross-border workers |

FL-Steuernummer (Individual Income Tax Number)

For individual income tax purposes, the Steuerverwaltung (STV) uses the PEID as the underlying identifier but refers to it in the context of personal tax filings as the FL-Steuernummer — literally the "FL tax number," where FL is Liechtenstein's ISO 3166-1 alpha-2 country code. It appears on personal tax assessment notices and is required when corresponding with the Steuerverwaltung about income tax matters.

Individuals filing the electronic Steuererklärung (tax return) via the STV's online portal must enter their PEID/FL-Steuernummer to authenticate. There is no separate issuance process — the PEID assigned at birth or registration serves as the FL-Steuernummer automatically.

FL-UID and MWST Number (VAT Identifier)

For VAT (Mehrwertsteuer / MWST) purposes, a registered business receives a separate FL-UID — a nine-digit identifier formatted as:

FL-XXXXXXXXX

This number is derived from the Swiss UID (Unternehmens-Identifikationsnummer) system, reflecting Liechtenstein's customs union and shared VAT territory with Switzerland. The FL-UID is:

- Mandatory on all VAT invoices issued by registered Liechtenstein businesses

- Required on the MWST certificate of registration

- The number used to query the official MWST register at mwstregister.li

- Different from the PEID — using the PEID in place of the FL-UID on a VAT invoice triggers invoice rejection by VAT-registered business customers

Liechtenstein's VAT rates (effective 1 January 2024):

| Rate | Applies to |

|---|---|

| 8.1% standard | Most goods and services |

| 2.6% reduced | Food, drugs, newspapers, books |

| 3.8% special | Accommodation (hotel) services |

The CHF 100,000 registration threshold applies to worldwide turnover, not Liechtenstein-only revenue. Non-established foreign businesses must appoint a fiscal representative domiciled in Liechtenstein before they can register.

eMWST Portal — Mandatory from January 2025

From January 2025, all VAT transactions must be processed through the eMWST portal at mwstportal.li. Paper submissions are no longer accepted. Access requires an eID.li credential — existing lilog accounts do not transfer. Foreign businesses relying on a fiscal representative must ensure their representative holds a valid eVertretung authorization tied to an active eID.li.

How Lookuptax can help you in VAT validation?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.

Frequently Asked Questions

Can I verify a Liechtenstein VAT number through EU VIES?

No. Although Liechtenstein is an EEA member, it is not an EU member state and is therefore excluded from the EU VIES system. Liechtenstein operates a shared VAT territory (MWST-Gebiet) with Switzerland under a customs-union treaty, and its VAT register is maintained separately by the Liechtenstein Tax Administration. To check whether a Liechtenstein VAT number (format: FL-XXXXXXXXX) is active, query the official MWST register at mwstregister.li directly — no third-party EU tool will return a result. Businesses that attempt VIES verification and receive a "not found" response should not interpret that as meaning the number is invalid. [1] [2]

Does a foreign digital-services company need a fiscal representative to register for Liechtenstein MWST?

Yes. A non-established business supplying digital or electronic services to Liechtenstein-resident consumers must register for MWST once its worldwide taxable turnover reaches CHF 100,000. Registration is not possible without first appointing a locally-based fiscal representative, who bears joint liability for all VAT obligations. The tax authority may also require a bank guarantee to secure the likely tax debt. Applications are submitted electronically through the eMWST portal at mwstportal.li — paper forms have not been accepted since 31 December 2024. Failure to register before reaching the threshold exposes the foreign supplier to back-taxes plus interest and a fine of up to CHF 10,000. [1] [2]

Does a Liechtenstein Stiftung (foundation) with Private Asset Structure status still need to report under CRS/AEOI?

Broadly, yes. Liechtenstein introduced AEOI under the CRS framework in 2016, and a Stiftung generally qualifies as a passive non-financial entity (NFE). The custodian bank — not the foundation itself — is the reporting financial institution, but the bank must collect and report to the Liechtenstein Tax Administration the identity of all controlling persons (founder, beneficiaries), total asset values, and payout amounts if any controlling person is a foreign tax resident. A Private Asset Structure (PAS) classification reduces the annual tax to a CHF 1,200 flat rate and removes the obligation to file annual income-tax returns, but it does not exempt the structure from CRS account reporting through its financial institution. [1] [2]

What corporate tax does a Liechtenstein Anstalt or Stiftung pay if it has no operating profit?

All Liechtenstein corporations, establishments (Anstalt), and foundations (Stiftung) are subject to a flat profit tax of 12.5%, but a mandatory annual minimum tax of CHF 1,800 applies regardless of profit for most entities — this amount is credited against any actual profit-tax liability. Entities whose total assets have not exceeded CHF 500,000 in each of the preceding three years are exempt from the minimum tax. A foundation that qualifies as a Private Asset Structure (PAS) pays a reduced minimum tax of CHF 1,200 per year instead and is not required to file an annual tax return, provided it conducts no commercial activity. [1] [2]

Is a Liechtenstein PEID the same number used for both tax returns and VAT — and where does the FL-UID fit in?

They are related but distinct. The PEID (Personenidentifikationsnummer) is the master identifier issued by the Office of Statistics; it is used on income-tax returns and as the underlying identifier for employers and employees. For VAT (MWST) purposes the tax authority issues a separate FL-UID — a nine-digit number formatted as FL-XXXXXXXXX — that appears on all VAT certificates and invoices. The FL-UID is built on the Swiss UID system and is mandatory on invoices for VAT-registered businesses; omitting it or using the PEID alone on a VAT invoice can trigger invoice-rejection by business customers and a fine of up to CHF 10,000 under the Liechtenstein VAT Act. [1] [2]

Do online marketplaces and platforms now bear VAT liability for sales into Liechtenstein?

Yes, from 1 January 2025. Under Liechtenstein Law No. 641.20, electronic platforms that facilitate the supply of goods or services to Liechtenstein customers are treated as the deemed supplier — meaning the platform, not the underlying seller, is liable for collecting and remitting MWST. This "deemed supplier" rule applies to marketplaces, portals, and apps. The CHF 100,000 global turnover threshold still triggers the registration obligation, but once crossed, VAT is owed on all qualifying sales through the platform — not only those made after the threshold is reached. Platforms that solely provide payment processing, advertising, or listing services without enabling direct seller-buyer contact are exempt from the rule. [1] [2]

Related Resources

- Switzerland UID number guide — the Swiss UID (CHE-XXX.XXX.XXX) underpins Liechtenstein's FL-UID; understanding both prevents cross-border invoice errors

- How to verify a Swiss UID number — step-by-step guide to the uid.admin.ch register, which also indexes FL-UIDs registered under the Swiss-Liechtenstein customs union

- Austria Tax ID guide — neighboring DACH-region country with its own ATU VAT format and fiscal representative rules

- Germany TIN number guide — German Steuer-ID and Umsatzsteuer-ID rules frequently consulted alongside Liechtenstein for DACH-region compliance

- EU VAT VIES verification guide — Liechtenstein FL-UIDs do not appear in VIES; this guide explains what VIES covers and when to use mwstregister.li instead