Finland TIN number guide

Business ID (Business Identity Code)

The Business ID, also known as Y-tunnus, is a crucial identifier assigned to businesses and organizations by either the PRH or the Tax Administration. Comprising seven digits, a dash, and a control mark (e.g., 1234567-8), this code plays a pivotal role in business identification.

It's important to note that while the Business ID uniquely identifies a business, it doesn't provide information about whether the business is registered with the Tax Administration registers or the Trade Register. For specific details on registration status, it's advisable to conduct a thorough check through the BIS search, the PRH, or the Tax Administration.

Furthermore, companies listed in the Trade Register, VAT Register, Prepayment Register, or Employer Register are required to prominently display their Business ID on various documents, including invoices, business letters, and forms. This ensures transparency and compliance with regulatory standards. If you're looking for information on VAT registration, consider performing a thorough search using relevant keywords such as "vat number verification," "find vat number," or "vat number lookup" for comprehensive results.

The Business ID, a vital identifier for legal entities like companies, remains constant as long as the entity is operational. However, changes in company types defined by law may alter the Business ID. Private traders' Business IDs are personal, changing when operations transfer between private traders or when a company continues a private trader's business. New businesses receive their ID upon registering the start-up notification in the Business Information System (BIS), jointly managed by the PRH and the Tax Administration.

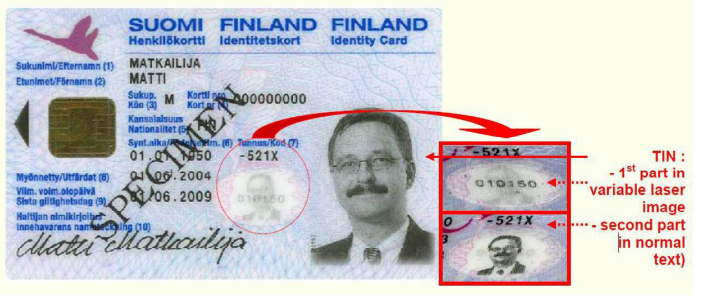

Henkilötunnus (HETU)

The HETU, also known as the Social Security number, is assigned at birth or immigration by the Population Register Centre of Finland. It comprises 11 characters for individuals, including 6 digits, 1 character (+, -, or A), 3 digits, and 1 alphanumeric character. The 7th character denotes the century of birth, with + indicating birth between 1800-1899, - for 1900-1999, and A for 2000-. This character is crucial, mandatorily recorded and reported in all records.

|

| Identity card (Henkilökortti) |

|

| Driving license |

Arvonlisaveronumero

The Finnish value-added tax is abbreviated as "alv." or "ALV" (without a period). The numeric representation is obtained from the LY code by incorporating the country code FI, and the hyphen between the last two digits is omitted. It is also known as "Mervärdesskattenummer"

For Example: FI01234567

When dealing with invoices, orders, cash sales receipts, and more, it's crucial to include the abbreviation "alv. rek." or "ALV rek." (signifying registered value-added tax liability) to indicate the entity's registered status for value-added tax liability.

Frequently Asked Questions

Which date determines the 24% vs 25.5% ALV rate when Finland's VAT changed on 1 September 2024?

The decisive factor is the date of delivery or service completion — not the invoice date or payment date. If goods were delivered or services completed before 1 September 2024, the 24% rate applies even if you invoice in September or later. Conversely, deliveries on or after 1 September 2024 attract 25.5%. One critical exception: if an advance payment was received before 1 September 2024, the 24% rate is locked in for that prepaid amount regardless of when the goods are delivered. Businesses that invoiced using the wrong rate for transitional-period transactions need to issue credit notes and corrected invoices. [1] [2]

Why does my Finnish counterpart's Y-tunnus fail EU VIES validation when I try to zero-rate an intra-EU sale?

VIES validates the Finnish VAT number (ALV-numero), not the Y-tunnus directly. The VAT number is formed by adding the prefix FI and dropping the hyphen: Y-tunnus 1234567-8 becomes FI12345678. However, having a Y-tunnus does not automatically mean the company is VAT-registered — a business can hold a Y-tunnus without enrolling in the VAT register (ALV-rekisteri). If VIES returns "invalid", check whether the supplier is actually registered for VAT via the Finnish Tax Administration's public register or the Business Information System (ytj.fi). Quoting a bare Y-tunnus on an intra-EU invoice, rather than the FI-prefixed VAT number, is a common invoice-rejection cause in Finnish B2B trade. [1] [2]

How do Finland's HETU reform separator characters affect payroll and tax-reporting software?

From 1 January 2023, the Henkilötunnus (HETU) century-separator character was expanded beyond the original three: for births in the 2000s, letters A–F are now valid (previously only A); for births in the 1900s, letters Y, X, W, V, U are valid alongside the traditional hyphen (-). The reform was necessary because codes for some high-frequency birth dates were nearing exhaustion due to immigration. Crucially, the separator is now part of the unique identity — stripping it when indexing persons will create duplicates. Any payroll, HR, or tax-filing system built to accept only +, -, or A must be updated. Existing codes remain valid without change; the expansion only applies to newly assigned codes. [1] [2]

When does construction reverse charge (käännetty arvonlisäverovelvollisuus) apply, and do foreign subcontractors need to register for Finnish VAT?

Finland's construction-sector reverse charge applies when two conditions are both met: the work involves construction services or construction-related staff leasing connected to real property in Finland, and the buyer is a business that regularly sells construction services or leases construction-sector employees on an ongoing basis. When these conditions are met, the seller invoices without VAT (noting "reverse charge" on the invoice), and the buyer self-accounts for the tax. A foreign subcontractor supplying construction services to a Finnish general contractor who regularly sells construction services does not need to register for Finnish VAT — the liability shifts to the Finnish buyer. Misapplying this rule and charging Finnish VAT results in double-taxation and requires a VAT refund claim. [1] [2]

Finland's small-business VAT threshold changed in 2025 — what happened to the old relief scheme for turnover under €30,000?

Effective 1 January 2025, Finland raised the mandatory VAT registration threshold from €15,000 to €20,000 annual turnover. At the same time, the previous graduated VAT relief (alennusjärjestelmä) — which reduced the effective VAT burden for businesses with turnover up to €30,000 — was abolished entirely. The result is a binary system: stay below €20,000 and owe no VAT; exceed it and pay full VAT on all taxable turnover. Businesses that relied on the old relief to smooth the threshold transition now face a cliff edge instead. Non-resident sellers remain unaffected by this threshold and must register immediately upon making any taxable supply in Finland. [1] [2]

Related Resources

- How to verify Finnish VAT numbers

- Finland e-invoicing (Finvoice) guide

- Worldwide directory of VAT and tax ID names

- VAT registration thresholds worldwide

How Lookuptax can help you ?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.