India Tax ID Guide — PAN, TAN, and GSTIN Explained

India uses three distinct tax identifiers, each administered by a different authority and serving a different purpose. Businesses operating in India — or trading cross-border with Indian counterparties — routinely need all three:

| Identifier | Administered by | Used for |

|---|---|---|

| PAN — Permanent Account Number | Income Tax Department | Income tax filings, TDS credit, KYC |

| TAN — Tax Deduction and Collection Account Number | Income Tax Department | TDS/TCS deduction and remittance |

| GSTIN — Goods and Services Tax Identification Number | GSTN (GST Network) | GST returns, e-invoicing, input tax credit |

Permanent Account Number (PAN)

PAN is the primary income-tax identifier for any "person" in India. The legal basis is Section 139A of the Income Tax Act, 1961, with detailed procedure set out in Rule 114 of the Income Tax Rules, 1962. PAN is mandatory for any individual or entity with taxable income; it is not obligatory for those below the exemption threshold but is commonly required for financial transactions such as opening bank accounts, purchasing property, or filing import/export declarations.

Applications are processed through UTIITSL or Protean (formerly NSDL eGov) on behalf of the Income Tax Department. Once allotted, PAN never changes.

PAN Format

A PAN is a 10-character alphanumeric string. A typical example is AFZPK7190K.

| Position | Content | Meaning |

|---|---|---|

| 1–3 | Letters (e.g. AFZ) | Alphabetic series AAA–ZZZ |

| 4 | Letter (e.g. P) | Entity / holder type |

| 5 | Letter (e.g. K) | First character of the holder's surname (individuals) or entity name |

| 6–9 | Digits (e.g. 7190) | Sequential number 0001–9999 |

| 10 | Letter (e.g. K) | Alphabetic check character |

4th character — entity type codes:

| Code | Holder type |

|---|---|

| P | Individual |

| F | Firm (partnership) |

| C | Company |

| H | Hindu Undivided Family (HUF) |

| A | Association of Persons (AOP) |

| T | Trust |

| B | Body of Individuals |

| L | Local Authority |

| J | Artificial Juridical Person |

| G | Government |

Where to find PAN: On the PAN card or PAN allotment letter issued by the Income Tax Department.

|

| PAN card |

Tax Deduction and Collection Account Number (TAN)

TAN is a separate 10-character alphanumeric identifier issued under Section 203A of the Income Tax Act, 1961. It is mandatory for every person who deducts or collects tax at source (TDS/TCS) — including employers paying salaries, companies making contractor payments, and entities paying rent above threshold limits. TAN must be quoted on all TDS challans, returns, and certificates. Failure to quote TAN in required documents attracts a penalty of ₹10,000 under Section 272BB.

TAN Format

TAN follows the pattern ABCD12345E:

| Position | Content | Meaning |

|---|---|---|

| 1–3 | Letters | City or state of registration (e.g. MUM for Mumbai) |

| 4 | Letter | First character of the deductor's name |

| 5–9 | Digits | Sequential number |

| 10 | Letter | Alphabetic check character |

Applications are filed using Form 49B at Protean TIN Facilitation Centres or online at the Protean-TIN website. The fee is ₹55 plus GST, and no supporting documents are required.

Goods and Services Tax Identification Number (GSTIN)

GSTIN is the identifier assigned when a business registers under the Goods and Services Tax (GST) regime. GST replaced the fragmented indirect tax system (VAT, service tax, excise) across India on 1 July 2017. GSTIN is used for filing GST returns, claiming input tax credit, generating e-invoices, and B2B verification.

Registration thresholds: ₹40 lakh annual turnover for goods suppliers, ₹20 lakh for service providers in regular states (₹20 lakh / ₹10 lakh respectively in special category states). Mandatory regardless of turnover for inter-state suppliers, e-commerce operators, and certain other categories.

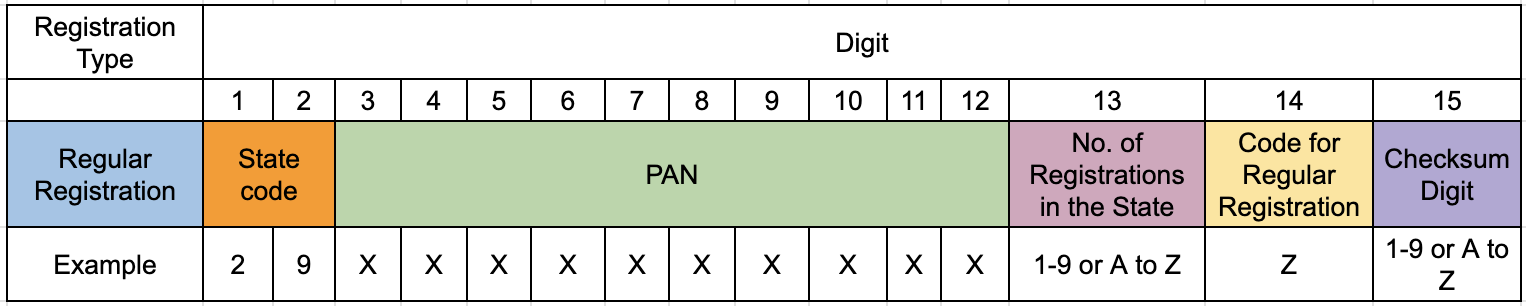

GSTIN Format

GSTIN is a 15-character alphanumeric code. Example: 27AABCU9603R1ZM

| Position | Content | Meaning |

|---|---|---|

| 1–2 | Digits | State code per Indian Census 2011 (e.g. 27 = Maharashtra) |

| 3–12 | 10 characters | PAN of the business entity (embedded verbatim) |

| 13 | Alphanumeric | Entity number: 1–9 for first 9 registrations under the same PAN in that state, then A–Z for further registrations |

| 14 | Always "Z" | Reserved character |

| 15 | Alphanumeric | Checksum digit (computed via a modified Luhn/modulo-36 algorithm) |

Because the GSTIN embeds the PAN, any mismatch between the embedded characters and the taxpayer's actual PAN triggers an immediate validation failure. The checksum character at position 15 independently verifies the full 14-character string.

Special state codes: Code 99 denotes "Other Country" (used for OIDAR foreign registrants) and code 97 denotes "Other Territory."

Official GSTIN Verification

Free public lookup is available at the GST portal — services.gst.gov.in/services/searchtp — without login. CAPTCHA completion is required. For programmatic verification at scale, see our guide on how to verify GSTIN in India.

How Lookuptax can help you?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.

Frequently Asked Questions

My company's PAN was flagged as inoperative even though we are a foreign entity — do we need to link Aadhaar?

No. Non-residents under the Income Tax Act and individuals who are not citizens of India are explicitly exempt from the PAN–Aadhaar linking requirement under Section 139AA. Foreign entities and NRIs whose PANs were wrongly marked inoperative after the June 30, 2023 deadline must submit their residential status proof — typically the last three years' ITR filed as non-resident, or a formal intimation — to their Jurisdictional Assessing Officer (JAO) to restore PAN operativity. Until restored, Indian payers will deduct TDS at the higher rate under Section 206AA/206CC, and pending refunds will be withheld. [1] [2]

A foreign company wants to supply goods at a trade exhibition in India for 60 days — what GSTIN do they need, and what is the advance tax trap?

A foreign company making occasional taxable supplies in India without a fixed place of business must register as a Non-Resident Taxable Person (NRTP) on the GST portal before commencing any supply. The registration is valid for up to 90 days (extendable once by 90 days). Critically, the GST portal will not generate an Application Reference Number (ARN) — and therefore no provisional GSTIN — until the applicant deposits advance tax equal to the estimated GST liability for the entire registration period. This upfront payment blocks many foreign exhibitors who are unaware of the requirement. NRTPs also cannot claim Input Tax Credit on inward supplies. [3] [4]

As a foreign SaaS or digital services company, do I need a GSTIN to sell to Indian customers, and is there a turnover threshold?

Yes — and there is no threshold exemption. Foreign companies supplying Online Information and Database Access or Retrieval (OIDAR) services (which includes SaaS, cloud computing, e-learning, digital content, and online advertising) to non-taxable Indian recipients must register under GST using Form GST REG-10, regardless of turnover. The applicable rate is 18% IGST. Registrants receive a GSTIN with state code "99" (Other Country) and must file Form GSTR-5A monthly by the 20th of the following month. No Input Tax Credit is available. India's 2% Equalisation Levy on digital e-commerce transactions was abolished effective August 1, 2024, and the 6% levy on online advertising was scrapped from April 1, 2025 — OIDAR GST is now the primary obligation. [5] [6]

Our Indian customer is withholding 20% TDS from our invoice even though a tax treaty gives us a lower rate — is that correct?

Not necessarily. Under Section 206AA of the Income Tax Act, an Indian payer must deduct TDS at 20% (or the applicable rate, whichever is higher) if the foreign recipient does not furnish a valid Indian PAN. However, when a Double Taxation Avoidance Agreement (DTAA) applies, the beneficial treaty rate prevails over the 20% domestic rate — even without an Indian PAN. To claim the lower DTAA rate, the foreign company must provide a Tax Residency Certificate (TRC) from its home country, a completed Form 10F, and declarations on beneficial ownership and absence of a Permanent Establishment in India. Without these documents, the 20% deduction stands and the excess can only be reclaimed via an ITR filing. [7] [8]

Our B2B e-invoice was rejected by the IRP with error code 2295 or 2150 — what does this mean and how do we fix it?

Both error codes indicate an Invoice Reference Number (IRN) conflict. Error 2150 means the exact invoice has already been registered on an IRP and an IRN exists — you cannot regenerate an IRN for the same invoice. Error 2295 means an IRN for the same invoice was registered on a different IRP portal. In both cases the original IRN remains valid; retrieve it from the e-invoice portal using your GSTIN and invoice number rather than re-submitting. A separate critical change from April 1, 2025 affects companies with Aggregate Annual Turnover (AATO) of ₹10 crore and above: the IRP will reject any invoice reported more than 30 days after the invoice date with no override available. [9] [10]

Does a foreign company need both PAN and TAN, or just one?

A foreign company needs both in different circumstances. PAN is required whenever the company has Indian-source income, acquires unlisted Indian shares exceeding ₹1 lakh, or wants to claim TDS refunds or DTAA treaty benefits (Form 10F requires a PAN or a formal declaration that none is required). TAN is required separately if the foreign company makes TDS-liable payments in India — for example, paying Indian employees, contractors, or rent from an Indian branch or project office. The two numbers serve entirely different purposes: quoting PAN on a TDS return where TAN is required (or vice versa) causes the return to be rejected by the ITD system. [11] [12]

Related Resources

- How to verify GSTIN in India — step-by-step GSTIN lookup on the official GST portal

- India IRP e-invoicing regulations — full IRN mandate, thresholds, and IRP portal guide

- Singapore TIN number guide — comparable Asian market with GST registration nuances

- Australia TIN number guide — ABN/TFN system for contrast with India's multi-ID approach

- Worldwide directory of VAT and tax ID names — local names and formats across 100+ countries