United Kingdom VAT number guide

This post is also available in: Español|Deutsch

VAT Number

In the UK, the tax identification number is referred to as the VAT number. It typically consists of either 9 or 12 numbers, occasionally preceded by 'GB,' such as 123456789 or GB123456789. Validating a UK VAT number can be done through the official HMRC site website or a VAT validation service provider like Lookuptax.

Unique Taxpayer Reference (UTR)

"UTR" stands for Unique Taxpayer Reference. The UTR is a 10-digit code that is unique to each taxpayer or entity registered with His Majesty's Revenue and Customs (HMRC). It is used to identify individuals, partnerships, and companies for tax purposes. The UTR is an essential component when communicating with HMRC, filing tax returns, and managing various tax-related matters. It's important to keep the UTR secure and readily accessible, especially when engaging in activities that involve taxation in the UK

Where to find UTR ?

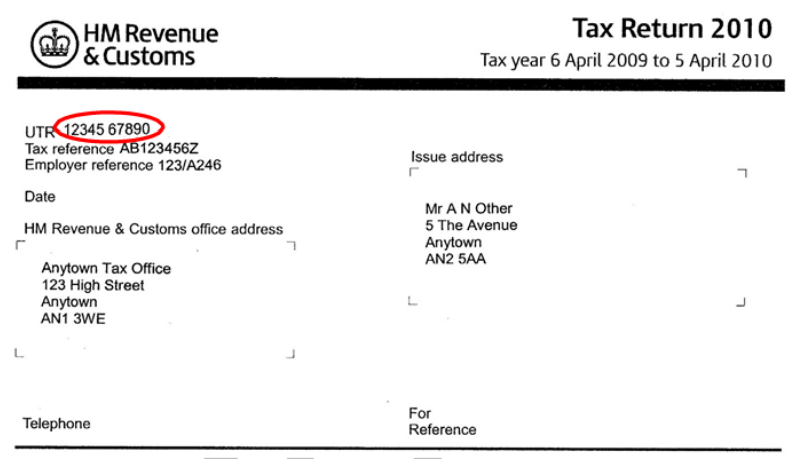

The UTR may be found on the front page of the tax return (form SA100 or CT600) as shown in the example below. The UTR may also be found on a "Notice to complete Tax Return" (form SA316 or CT603) or a Statement of Account. Depending on the type of document issued the reference may be printed next to the headings "Tax Reference", "UTR" or "Official Use".

|

| UTR on tax return form |

National Insurance Number (NINO)

A National Insurance Number (NINO) is composed of two letters, six numbers, and a suffix letter (such as A, B, C, or D, for instance, DQ123456C). All individuals residing regularly in the United Kingdom are either assigned or can receive a NINO. Young people living in the UK are automatically granted a NINO as they approach the age of 16. This identifier appears on various official documents, and individuals are informed of their NINO through an official letter from the Department for Work and Pensions or HM Revenue and Customs.

It's important to note that this letter explicitly states, "This is not proof of identity," and therefore cannot be utilized for identity verification. While the NINO can be cited as the tax reference number on certain official documents from HM Revenue and Customs, it does not serve as proof of identity.

Where to find NINO ?

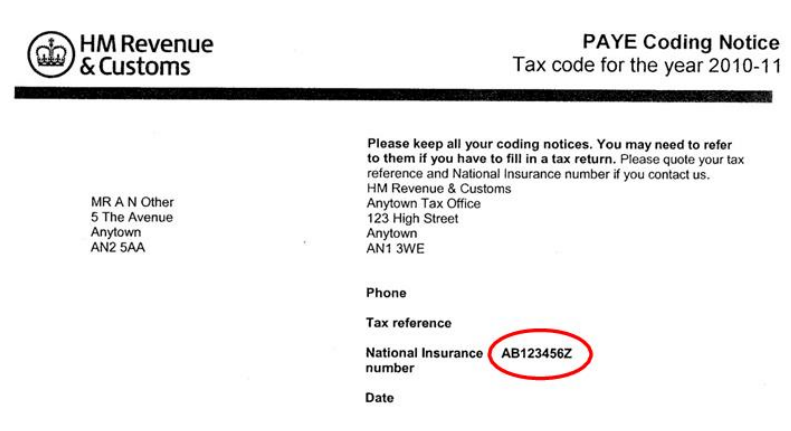

HMRC issues coding notices to taxpayers. The heading of the notice contains the National Insurance Number as indicated in the example below.The National Insurance Number may also be shown on a National Insurance card and on letters issued by the Department for Work and Pensions (DWP). The number also appears on an employee's pay slip and on a Statement of Account issued by HMRC.

|

| NINO on coding notice |

How Lookuptax can help you ?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance

Frequently Asked Questions

Does the £90,000 VAT registration threshold apply to overseas businesses selling into the UK?

No. The £90,000 annual turnover threshold (raised from £85,000 on 31 March 2024) applies only to UK-established businesses. An overseas business classified as a Non-Established Taxable Person (NETP) must register for UK VAT before making its very first taxable supply in the UK, regardless of value. [1] This is one of the most common surprises for foreign SaaS vendors and marketplace sellers: once a UK customer places a paid order, the obligation to register has already arisen. Registration is done via form VAT1 and must happen within 30 days of the trigger. [2]

Why does a UK VAT number show as invalid in EU VIES after Brexit?

Since 1 January 2021, UK VAT numbers are no longer listed in the EU's VIES database. EU VIES only covers VAT numbers issued by EU member states; the UK left the EU VAT area on that date. To verify a UK GB-prefixed number (format: GB followed by 9 digits, or 12 digits for branch traders), you must use HMRC's dedicated checker at gov.uk/check-uk-vat-number. [1] Attempting to verify a UK number via VIES will always return "invalid" — a false negative that does not reflect the number's actual registration status. Businesses relying on VIES for UK supplier checks should update their accounts-payable workflows accordingly to avoid incorrectly blocking VAT reclaim. [2]

What happens to a subcontractor's CIS deduction rate if their UTR cannot be verified?

Under the Construction Industry Scheme (CIS), a contractor must verify every new subcontractor with HMRC before making the first payment. If the subcontractor cannot provide a valid UTR — or if the name or National Insurance number submitted to HMRC does not exactly match HMRC's records — the verification will return an "unmatched" result. In that case the contractor is required to deduct tax at the higher unmatched rate of 30% rather than the standard 20% net rate or the 0% gross rate available to those with Gross Payment Status. [1] The subcontractor cannot recover the extra 10% deduction until they file a Self Assessment return and claim it as a credit. Even a transposed digit in the UTR triggers the 30% rate. [2]

If I move abroad and rent out my UK property, does my tenant have to withhold tax from my rent?

Yes, unless you apply to HMRC in advance under the Non-Resident Landlord (NRL) Scheme. Once your usual place of abode is outside the UK for six months or more, you become a non-resident landlord. Any UK letting agent must then deduct basic-rate income tax (currently 20%) from your rental income before paying it to you, and remit that tax to HMRC. If there is no letting agent and the tenant pays more than £100 per week directly to an overseas landlord, the tenant must deduct and account for the tax themselves. [1] To receive rents gross, submit form NRL1 to HMRC before departing or immediately on becoming non-resident. HMRC approval is not instant: the approval date only takes effect from the first day of the quarter in which the application was received, meaning earlier rent may still be subject to withholding. [2]

Are all VAT-registered businesses required to file VAT returns through Making Tax Digital compatible software?

Yes. Since 1 April 2022, Making Tax Digital (MTD) for VAT has been mandatory for every VAT-registered business in the UK, regardless of turnover. Businesses must keep digital VAT records and submit their returns only through MTD-compatible software — this includes accounting packages and spreadsheet-based bridging software. [1] Exemptions mirror the existing VAT online-filing exemption (for example, certain businesses where it is not reasonably practicable to use digital tools). Businesses that continue filing via HMRC's legacy VAT portal or on paper outside the exemption criteria are liable to a penalty; a points-based late-submission penalty regime also applies from January 2023. HMRC maintains a list of approved MTD-compatible software at gov.uk. [2]