Croatia OIB (Tax ID) Guide — Format, Validation & Compliance

This post is also available in: Español

Osobni identifikacijski broj (OIB) — Croatia's Personal Identification Number

The Republic of Croatia introduced the Osobni identifikacijski broj (OIB) as the single universal identifier across the entire Croatian public administration system. The Ministry of Finance — Tax Administration (Porezna uprava) issues and manages all OIBs, and every interaction with Croatian state bodies requires one: tax filing, property registration, employment, company formation, and banking.

OIBs are assigned to:

- Croatian citizens — automatically at birth or upon naturalisation

- Legal entities — upon incorporation or registration of a branch in Croatia

- Foreign individuals and companies — when a legal basis for monitoring arises in Croatia (property acquisition, VAT registration, employment, or other regulated activity)

OIB Format

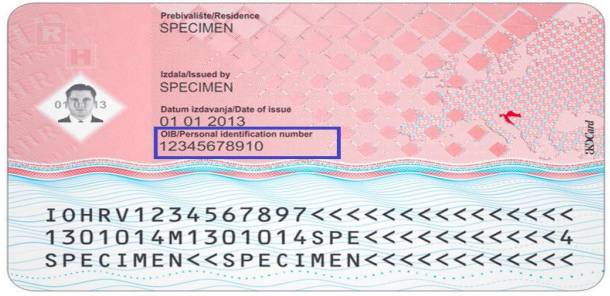

The OIB consists of 11 digits. The first 10 digits are randomly assigned; the 11th is a control digit computed using the ISO 7064 Mod 11,10 algorithm (also called "Modul 11.10"). The calculation iterates through each digit: initialize r = 10; for each digit d, compute r = ((r % 10 || 10) × 2) mod 11; then r = (11 − r) mod 10 gives the check digit. A result of 10 is invalid, so the sequence is reassigned.

Example: HR99999999999 (the HR prefix is used exclusively for the PDV-ID / VAT number; the raw OIB carries no prefix).

|

| OIB — 11-digit format |

OIB vs PDV-ID (VAT number)

The OIB and the Croatian VAT number (PDV-ID) are derived from the same underlying number but are not interchangeable:

| Identifier | Format | Used For |

|---|---|---|

| OIB | 11 digits (e.g., 12345678901) | All domestic tax, legal, and administrative purposes |

| PDV-ID | HR + 11 digits (e.g., HR12345678901) | EU intra-community VAT transactions; verifiable on EU VIES |

Only VAT-registered entities hold a PDV-ID. Every entity with a PDV-ID also has an OIB, but not every OIB holder is VAT-registered.

Matični broj subjekta (MBS)

The Matični broj subjekta (MBS) is Croatia's court company registration number, not a tax identifier. It is issued by the Commercial Court Register and used in legal and corporate filings. For invoicing and tax reporting purposes, always use the OIB (or PDV-ID for EU VAT transactions) — not the MBS.

Croatia VAT (PDV) — Key Thresholds

- Standard VAT rate: 25% (reduced rates: 13% and 5%)

- Domestic registration threshold: EUR 60,000 annual turnover (raised from EUR 40,000 in 2025)

- Non-resident / foreign businesses: no minimum threshold — registration is required from the first taxable transaction in Croatia

- EU distance selling threshold: EUR 10,000 EU-wide (applies to B2C sales across all EU member states)

Foreign non-EU companies must appoint a fiscal representative who assumes joint and several liability for all Croatian VAT obligations. EU businesses may instead register directly or use the VAT One Stop Shop (OSS) scheme to avoid a Croatian VAT establishment.

Fiscalization 2.0 and B2B E-Invoicing

Croatia's new Fiscalization Act (Zakon o fiskalizaciji, NN 89/25) took effect on 1 September 2025. Key mandates:

- 1 January 2026: Mandatory B2B and B2G e-invoicing and real-time e-reporting for all VAT-registered businesses via the HR-FISK 2.0 platform (UBL 2.1 format, HR-FISK CIUS extension)

- 1 January 2027: Mandatory e-invoicing extended to all remaining entities (non-VAT registered)

- Every invoice message must carry a qualified electronic signature tied to the issuer's OIB

- Invoice retention: 11 years

Non-compliance penalties range from EUR 2,650 to EUR 66,360 for legal entities, with repeat violations reaching EUR 92,900. Separate fines of EUR 1,330 to EUR 13,300 apply for failures in real-time e-reporting. This is a directly OIB-linked obligation — if your OIB is not properly enrolled in the Tax Administration's certificate system, your invoices cannot be legally fiscalised.

How Lookuptax can help you?

Lookuptax VAT validation revolutionizes VAT number validation with its robust platform, empowering businesses to seamlessly verify VAT numbers across over 100 countries. Our cutting-edge technology ensures accurate and efficient validation, reducing errors and enhancing compliance.

Frequently Asked Questions

Can a foreign company obtain an OIB and Croatian PDV-ID without a physical office in Croatia?

Yes, but the application requires documented justification. A non-resident legal entity is assigned an OIB when there is a legal basis for monitoring it in Croatia — typically VAT registration, property acquisition, or branch registration. To register for PDV (VAT), you must simultaneously submit Form P-PDV (VAT registration) and the OIB assignment application to Porezna uprava. Non-EU businesses must appoint a fiscal representative who assumes joint and several liability for all Croatian VAT obligations. EU businesses may register directly or use the One Stop Shop (OSS) scheme to avoid establishing a Croatian presence. The process takes 2–4 weeks when documentation is complete. [1] [2]

I need an OIB to open a Croatian bank account, but banks ask for an account number on OIB application forms — how do I break the loop?

This is a genuine documented catch-22 that expats regularly encounter. The resolution: the OIB does not require a bank account number on the application — that confusion arises from some bank onboarding forms asking for an OIB before the account is opened. In practice, you can apply for an OIB at any Porezna uprava office with only a valid passport and a stated reason (e.g., "opening a bank account" is itself a valid reason). OIB is issued free of charge, typically within one working day at the office. Once you have your OIB, approach the bank — Croatian banks classify OIB-holders without a residence permit as non-resident account holders, which involves additional documentation but is permitted. [3] [4]

My Croatian business partner is withholding 15% from my invoice — can I reduce or eliminate it?

Croatia applies a 15% withholding tax on royalties, interest, and certain services (market research, tax consulting, auditing) paid to non-resident entities. If your country has a Double Taxation Treaty (DTT) with Croatia, you may qualify for a reduced or zero rate — but relief is not automatic. The Croatian payer must obtain a tax residency certificate from your home country's tax authority and submit it to Porezna uprava before the payment is made. If no certificate is filed in time, the full 15% is withheld and you must file a refund claim afterwards. Payments to entities in EU-listed non-cooperative jurisdictions attract a higher 25% rate. Always confirm treaty eligibility before invoicing to avoid post-payment refund delays that typically take 3–6 months. [5] [6]

Does Croatia's Fiscalization 2.0 mandate require an OIB-linked digital certificate, and what are the penalties for non-compliance?

Yes. Under the Fiscalization Law (Zakon o fiskalizaciji, NN 89/25), all fiscalisation and e-reporting messages transmitted to the Tax Administration must be signed with a qualified electronic signature tied to the issuer's OIB. Mandatory B2B e-invoicing via the national HR-FISK platform takes effect on 1 January 2026 for all VAT-registered businesses, and on 1 January 2027 for all remaining entities. Penalties for failure to fiscalize an invoice range from EUR 2,650 to EUR 66,360 for legal entities; repeated violations can reach EUR 92,900. Failure to transmit real-time e-reporting data carries separate fines of EUR 1,330 to EUR 13,300. Invoice archiving must be maintained for 11 years. [7] [8]

I hold a Croatian Digital Nomad Visa and exceeded 183 days — am I now a Croatian tax resident?

Not automatically. The Digital Nomad Visa (a temporary residence permit under the Croatian Aliens Act, not a visa in the legal sense) is specifically structured so that holders remain non-tax-residents even beyond the 183-day threshold, provided their primary economic ties remain in their home country. Income from employers or clients not registered in Croatia is fully exempt from Croatian income tax during the permit period. However, if you register habitual residence or establish an economic centre of interest in Croatia — for example, by opening a Croatian-registered sole proprietorship — Porezna uprava can reclassify you as a tax resident and apply income tax rates of 15–23.6% on income up to EUR 50,400 and 25–35.4% above that threshold. Passive income (dividends, rental income from Croatian property) is taxable regardless of nomad visa status. [9] [10]

Why does my OIB pass the ISO 7064 Mod 11,10 checksum but still get rejected by a partner's system?

Passing the checksum confirms only that the number is mathematically well-formed — it does not verify the OIB is assigned to a live, active entity. Common rejection causes: (1) the OIB belongs to a dissolved or struck-off entity; (2) systems confuse the raw 11-digit OIB with the HR-prefixed PDV-ID — the OIB itself never carries the "HR" country prefix; (3) the partner's system expects the PDV-ID for VAT purposes but receives the bare OIB; (4) name or address data in the partner's registry mismatches the Tax Administration record. To confirm an OIB is genuinely active and linked to the correct entity, use the Porezna uprava public registry. For VAT-registered entities, verify the HR-prefixed PDV-ID through the EU VIES system. [11] [12]