France VAT guidelines

This post is also available in: Español|中文|Deutsch|Português|Français

| FACTSHEET | |

|---|---|

| Country code | FR |

| Tax name | Taxe sur la valeur ajoutée (TVA) |

| Tax Authority | Tax administration |

Overview

France follows VAT system for indirect taxes. It is known as Taxe sur la valeur ajoutée (TVA).

France is recodifying its VAT law. Ordonnance n° 2025-1247 of 17 December 2025, published in the Journal officiel on 20 December 2025, moves the legislative VAT provisions out of the Code général des impôts (CGI) and into Book II of the Code des impositions sur les biens et services (CIBS), with effect from 1 September 2026.

The recodification is à droit constant — it renumbers the provisions rather than rewriting them, and a reference to a repealed CGI provision is read as a reference to the corresponding CIBS provision. DGFiP rescrit BOI-RES-TVA-000253 of 18 February 2026 confirms that existing BOFiP doctrine and individual rulings (rescrits) issued under the CGI provisions remain applicable under the corresponding CIBS articles from that date. [1]

What this means for this guide. The CGI article numbers cited below — Article 293 B (franchise en base), Article 262 (exonérations / exports), Article 283 (redevable / autoliquidation) and the rest — keep their substance but change their statutory home on 1 September 2026. For periods from that date, update statutory references in contracts, invoice legal mentions, VAT documentation and tax-engine configuration to the corresponding CIBS Book II article. The date is the same one on which the B2B e-invoicing mandate starts (see Einvoicing below), so both changes land in a single cutover window.

Tax Rates

- Standard rates - 20%

- Pricinpal reduced rates - 10 % 5.5%

- Special Reduced rates & 2.1%

- Taxes applicable might be different in Corsica, Guadeloupe, Martinique and Reunion

Registration Threshold

France's franchise en base de TVA (Article 293 B CGI) exempts small businesses from charging and declaring TVA. The thresholds were reset with effect from 1 January 2025 and are now decoupled from the micro-entreprise regime thresholds. Each activity has a seuil (the ordinary ceiling) and a seuil majoré (the tolerance ceiling): [1]

| Activity | Seuil (ordinary threshold) | Seuil majoré (tolerance) |

|---|---|---|

| Ventes de marchandises — sale of goods, on-site consumption, accommodation | €85,000 | €93,500 |

| Prestations de services — services and other furnished rentals | €37,500 | €41,250 |

Goods - €85,000

Professionals involved in the purchase and resale of goods, sales for immediate consumption on-site, and the provision of accommodation (including activities like renting rural lodges, furnished tourist accommodations, and bed and breakfast establishments) when their turnover does not exceed €85,000. To qualify for this VAT exemption, you must meet one of the following criteria:

- Your turnover for the previous calendar year (N-1) should not exceed €85,000.

- Your turnover for the penultimate calendar year (N-2) should not exceed €85,000, and your turnover for the previous calendar year (N-1) should not exceed €93,500.

- For the current calendar year (N), your turnover must not exceed €93,500. If you surpass this threshold, you will be required to remit VAT, commencing from the first day of the month in which the threshold is exceeded.

Services - €37,500

Service providers and furnished rental companies (excluding the rental categories mentioned above) can benefit from a VAT exemption when their turnover does not exceed €37,500. In order to qualify for the VAT exemption, you need to meet one of the following conditions:

- Your sales in the previous calendar year (N-1) should not exceed €37,500.

- Your sales for the penultimate calendar year (N-2) must not surpass €37,500, and the sales for the preceding calendar year (N-1) should not exceed €41,250.

- Your sales for the current calendar year (N) must stay below €41,250. If you surpass this threshold, you will be required to remit VAT starting from the first day of the month in which the threshold is exceeded.

Domestic purchases

VAT not applicable - Article 293b of CGI: CGI : General Tax Code must appear on each invoice. (From 1 September 2026 this provision sits in Book II of the CIBS rather than the CGI — see the recodification note under Overview; the invoice mention should be updated to the corresponding CIBS article for invoices issued from that date.) By benefiting from the VAT-based exemption system, you cannot deduct it from your purchases (goods or services) made within the framework of your professional activity.

To be able to deduct VAT on your professional purchases, you must opt out of the VAT-based exemption regime .

Intra community

When you make purchases of goods, they are not subject to VAT as long as the total amount of your acquisitions does not exceed €10,000 per year. As soon as this threshold is exceeded, you are subject to payment of VAT.

On the other hand, when you purchase services, you must pay VAT regardless of the amount.

As you are subject to the VAT-based exemption regime, you will not be able to deduct VAT on your purchases . To be able to deduct VAT on your professional purchases, you must opt out of the VAT-based exemption regime.

Exports & Imports

For exports, whether you are under the VAT-based exemption regime or not, you do not charge VAT.

When you carry out imports, whether you are under the VAT-based exemption regime or not, you must pay VAT. On the other hand, with a VAT exemption, you will not be able to deduct the VAT you paid on your imports. To be able to deduct VAT on your professional purchases, you must waive the VAT exemption.

VAT number format

- FR (country code) + 2 digits + SIREN

- Country code + 11 characters. May include alphabetical characters (any except O or I) as first or second or first and second characters.

- Example - 12345678901, X1234567890, 1X123456789, XX123456789

Intra community VAT number

A company that is not liable for VAT is typically not obligated to possess an intra-community VAT number. Nevertheless, this number becomes necessary when the company engages in purchases within the EU that surpass a total of €10,000 annually or when it conducts transactions involving services with EU-based businesses.

Register for Intra community VAT number

For VAT-registered companies, the company's Tax Service (SIE) automatically provides the intra-Community company VAT number during the registration process. This number is required to be displayed on the company's commercial and administrative documents, including invoices and VAT declarations.

On the other hand, companies that are not subject to VAT must request an intra-Community VAT number online through their business account email on the Impat.gouv.fr website if they:

- Engage in transactions involving services with professionals established in the European Union.

- Conduct purchases of goods or services in the European Union that exceed €10,000.

Types of identification numbers issued to a company

| Number | Utility | Shape |

|---|---|---|

| SIREN | Unique identification of your company, its identity card. Must be provided during all steps | 9 digits |

| SIRET | Identification of each establishment of the same company in which the activity is carried out With geographical indication of activity/building. Must appear on pay slips | 14 digits = 9 SIREN digits + 5 institution-specific digits |

| EPA code (or NAF code) | Identification of the industry of your main activity for each establishment.Determine the collective agreement that applies to your employees. Must appear on pay slips | 4 digits + 1 letter |

| RCS (Trade and businesses Register) | Proof of your registration if you are a merchant as IS: IS: Sole traderor as a commercial business | SCR + city of registration + SIREN number |

| LEI ( Legal Entity Identifier or Legal Entity Identifier) | Identification of financial businesses | 20-character string of letters and numbers |

| Intra-Community VAT | Tax registration if you pay VAT. Must appear on invoices and VAT returns | FR (country code) + 2 digits + SIREN |

VAT validation

It is advisable to verify the VAT number on invoices before conducting any transaction.

In the case of an EU partner whose intra-EU VAT number is deemed "invalid," they should furnish a tax certificate issued by their tax authority. Failure to provide this certificate will result in invoicing under the French VAT system.

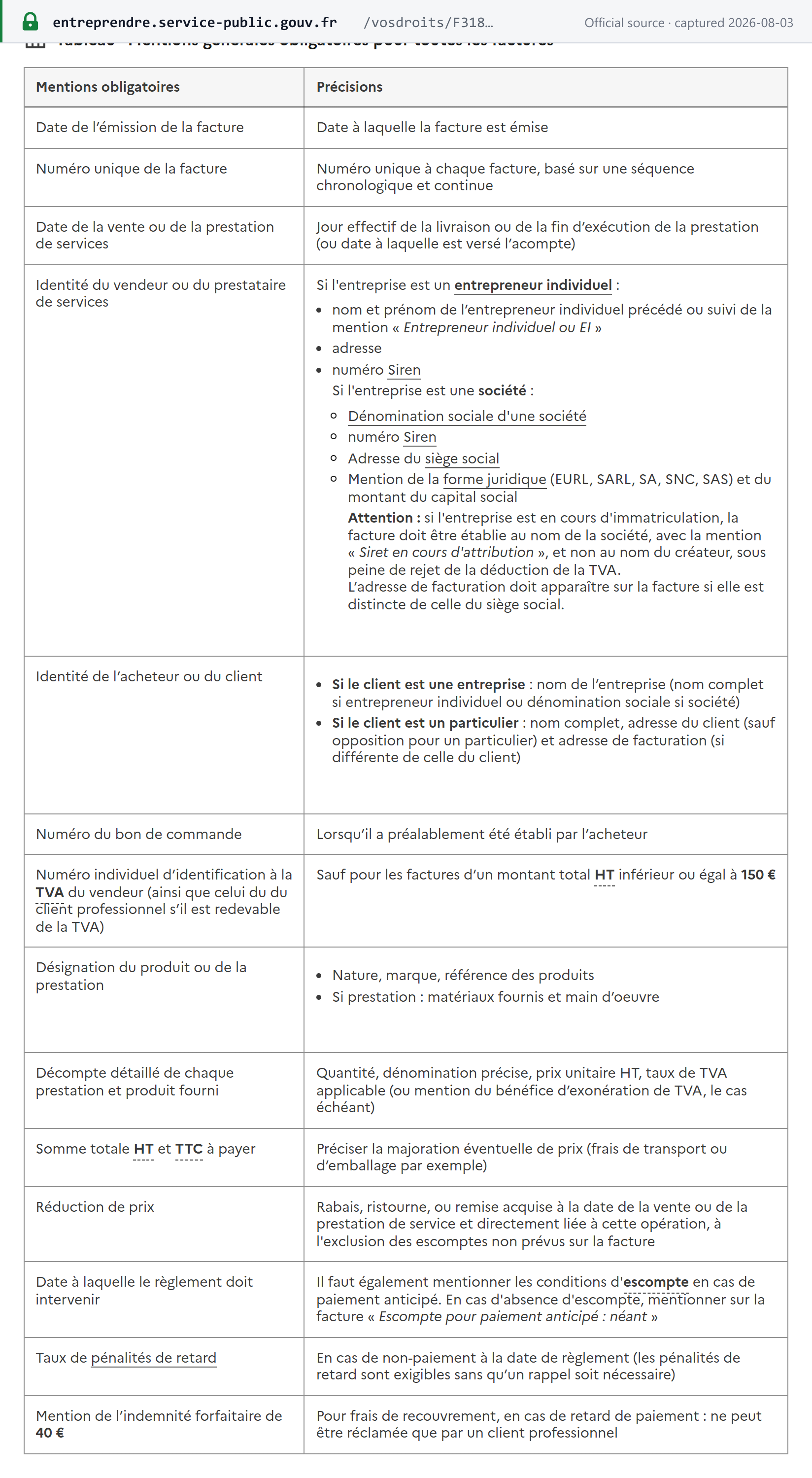

Invoice Information

| Items | Description |

|---|---|

| Date of invoice issue | The date on which the invoice is created. |

| Invoice Numbering | Each invoice should bear a unique number in a continuous chronological sequence (e.g., invoice 01, 02, 03). In specific cases, separate numbering series may be employed, such as using a prefix per year (e.g., 2018-XX) or per year and month (e.g., 2018-01-XX). For instance, if your invoice concludes in January with invoice number 25: _ January: Invoice No. 2018-01-025 _ February: Invoice No. 2018-02-026 * This number must appear on all pages of the invoice. |

| Date of sale or service provision | Current day of delivery or completion of the service |

| Buyer Identity | Name (or corporate name) Address of the registered office of a company Billing address (if different from the registered office) |

| Identity of the seller or supplier | - The full name of an individual contractor, either before or after specifying "Sole trader" or "IS." - The name of the business. - SCR number (Trade and businesses Register) for a trader. - Siren Number. - Address of the registered office, including the name of the establishment. - In the case of a business, mention of the legal form (e.g., EURL, SARL, SA, SNC, SAS) and the declared share capital. >Attention: If the company is in the process of registration, the invoice must be prepared in the name of the business, with the Siret number assigned to it, and not in the name of the creator. Failure to do so may result in the deduction of VAT being rejected. |

| Purchase Order Number | When it has been previously established by the buyer |

| VAT identification number of the seller and the professional customer, only if the latter is linked to the VAT: VAT: Value added tax(reverse charge) | Except for invoices for a total amount excluding tax: Excl. VAT: Duty-freeless than or equal to €150 |

| Description of the product or service | Nature, brand, product reference Supply: materials supplied and labor |

| Detailed breakdown of each service and product provided | Quantity and price detail (optional if the service has been the subject of a prior, descriptive and detailed quote, accepted by the customer and in conformity with the service performed) |

| List Price | Unit price not included VAT, VAT: Value added taxof products sold or hourly rate excluding VAT of services supplied |

| Possible price increase | Transport or packaging costs, for example |

| VAT rate legally applicable Total corresponding VAT amount | If transactions are subject to different VAT rates, the corresponding rate must be shown on each line |

| Price reduction | Discounts, rebates or rebates earned on the date of sale or service and directly related to this transaction, excluding discounts not provided on the invoice |

| Total sum payable excluding tax (excluding VAT) and all taxes included (including VAT) | |

| Date or time of payment | Date on which settlement is to take place Discount terms in case of early payment In the case of no discount, indicate on the invoice: Prepayment Discount: None |

| Rate of late penalties | Due for non-payment on the settlement date (late penalties are due without a reminder) |

| Mention of the lump sum payment of €40 | For recovery costs, in case of late payment |

| Additional info | |

| Member of an approved association , payment by check and credit card is accepted | If the seller or supplier is a member of a management center or an approved association |

| VAT not applicable, art. 293 B of the CGI | If the seller or supplier benefits from the VAT exemption (eg self-employed), the invoice is tax-free |

| Reverse charge Make it clear that this is a duty-free amount | If work is carried out by a subcontractor of the building on behalf of a contractor subject to VAT, the subcontractor no longer declares VAT and the main company declares it ( reverse charge of VAT ) |

| WEEE Eco-participation | Purchase of electronic products or equipment or furniture. |

| Remuneration for private copying (RCP) | Acquisition of a recording medium |

| Self-billing | If the customer produces the invoice himself instead of the seller or supplier |

| B2B invoice | B2C invoice |

|  |

Issuance of invoice

An invoice must be generated at the moment when goods are delivered or services are rendered. Nevertheless, there are exceptions where an invoice can be issued at a different time:

- In the case of a VAT-exempt supply of goods, the invoice must be issued no later than the 15th of the month following the month in which the delivery occurred.

- For services for which the customer is responsible for paying the VAT, the invoice should be issued no later than the 15th of the month following the period in which the service was provided.

Authenticity of its invoices

Companies involved in issuing or receiving invoices must have the means to verify the genuineness of their invoices. This can be achieved through one of the following methods:

- Implementing Robust Invoice Controls: This involves establishing adequate procedures to verify the source, integrity of the content, and readability of the invoice. This process is akin to a dependable audit.

- Utilizing a Qualified Electronic Signature: An electronic signature that is based on a qualified certificate is employed. It should be generated using a secure electronic signature creation device. This also extends to electronic signatures that, while not qualified, are officially recognized as such by the relevant administration.

- Employing Electronic Data Interchange (EDI) for Invoicing: EDI, which stands for electronic data interchange, can be used as a method for generating and processing invoices.

Intra community supply of goods

Imports

Before engaging in an intra-Community exchange of goods, it is imperative to secure an intra-Community VAT number from the local tax office (SIE). This number will need to be included on the invoices.

Upon the goods' arrival in France, your company is responsible for paying the French VAT based on the transaction price. The invoices issued by the seller (your supplier) will not include VAT from their country.

Exports

Goods shipped can be exempt from French VAT if the following four conditions are met:

- The delivery is made for a consideration, meaning it must be a sale and not a donation.

- Both you and your customer are subject to VAT, and you must possess a VAT registration number. If your customer is a consumer, the supply cannot be exempt from VAT. You are obliged to invoice it and remit it to France.

- Your customer does not qualify for the derogation (PBRD: Person benefiting from the derogation) that allows for the exemption of intra-Community acquisitions from VAT.

- The goods are dispatched or transported outside France. You must be able to provide evidence of the transportation, for example, through a transport invoice.

To qualify for the exemption, you also need to adhere to these conditions:

- Include your VAT number and your customer's VAT number on the invoice.

- Include the words 'VAT exemption, Article 262b(I) of the General Tax Code' on the invoice.

- Record the transaction on your VAT return under the category "exempt transactions."

Intra community supply of services

Selling to Businesses

The applicable VAT rate will align with the country in which the service purchaser is based.

You are required to issue an invoice for your service exclusive of taxes (HT, hors taxe).

It is the responsibility of your business customer to settle the VAT at the rate applicable in their own country of establishment, and they must report it to their local tax authorities.

Selling to Private Individuals

In this case, the applicable VAT rate is the French VAT rate.

You should invoice your service, inclusive of all taxes, including VAT, at the appropriate VAT rate.

Foreign currency invoice

The amount of VAT to be paid or regularized must be indicated in euro. To convert this amount into euros, the last published exchange rate by the European Central Bank (ECB). This exchange rate must be indicated on the invoice.

VAT returns format

In the context of intra-community sales and purchases, it is necessary to submit INTRASTAT and VIES declarations for goods and services, respectively.

INTRASTAT

INTRASTAT consists of two distinct procedures: a statistical survey and a VAT recapitulative statement.

You are obligated to fulfill this reporting requirement if you fall into any of the following categories:

In the previous calendar year, if your acquisitions amounted to €460,000 or more, or if your acquisitions in the previous calendar year were less than €460,000 but you surpass that threshold during the current year.

If your company engages in intra-Community deliveries, there is no specific threshold; DEB reporting is mandatory from the very first intra-Community delivery, regardless of the transaction amount. It is important to note that the statistical survey response is obligatory even if your company doesn't have a transaction flow. In such cases, you should submit a "month without a statistical response" through the DEB WEB online service.

The VAT recapitulative statement corresponds to the tax-related aspect of the DEB. You are required to retain the data used to complete the VAT Summary Report for a period of 6 years starting from the date of the transaction that generated the VAT Summary Report.

VIES

VIES pertains to the declaration of services within the European context, specifically for sales of services to a business entity. This reporting obligation is applicable without any threshold conditions.

The declaration should encompass the following information:

- Customer Name

- Customer's offset tax number

- Invoiced Amount

This declaration must be submitted on a monthly basis, no later than the 11th business day of the month that follows the transaction, whether it was conducted on paper or online.

Invoice requirements

France's invoicing rules are split across two texts. Article 289 of the Code général des impôts (CGI) sets who must issue an invoice and when; Article 242 nonies A of Annexe II to the CGI fixes the mandatory particulars (mentions obligatoires) that the invoice must carry. Both apply to every taxable person today, independently of the B2B e-invoicing mandate — that mandate's scope, platforms and timeline are in Einvoicing below. [1] [2]

From 1 September 2026 these provisions keep their substance but change their statutory home — see the recodification note under Overview. The article numbers below are the CGI numbers in force up to that date.

Mandatory content

Required particulars under Article 242 nonies A, Annexe II CGI (version in force since 1 January 2025, as amended by décret n° 2024-1195 of 21 December 2024): [2]

| Required particular | Notes |

|---|---|

| Full name, business identification number and address of the supplier and of the customer | 1° — the identification number is the one under art. R. 123-221 of the Code de commerce, i.e. the SIREN. [2] |

| Supplier's individual VAT identification number (numéro de TVA intracommunautaire) | 2° — this is one of only two particulars that a low-value or franchise-en-base invoice may omit; see Simplified invoices. [2] |

| Both parties' VAT identification numbers on intra-EU supplies of goods, and on services where the customer accounts for the tax | 3° and 4°. [2] |

| Fiscal representative's individual identification number, full name and address, where one is appointed | 5°. [2] |

| Mention "Membre d'un assujetti unique", plus that member's name, address and VAT number | 5° bis — VAT-group members. [2] |

| Date of issue | 6°. [2] |

| Unique invoice number, drawn from a chronological and continuous sequence | 7° — distinct series are allowed where business conditions justify them; see Issuance deadline and numbering. [2] [3] |

| Delivery address of the goods, where it differs from the customer's address | 7° bis — one of the four new mentions; see the note below the table. [2] |

| Per line: quantity, precise description, unit price excluding tax, and the VAT rate applicable (or the fact that the supply is exempt) | 8°. [2] |

| Whether the invoiced operations consist exclusively of supplies of goods, exclusively of services, or of both | 8° bis — one of the four new mentions. [2] |

| Rabais, remises, ristournes (rebates, discounts and allowances) acquired and directly linked to the transaction | 9°. [2] |

| Date of the supply or of completion of the service, or the date an acompte was paid, where determinable and different from the invoice date | 10°. [2] |

| Total VAT payable, and the taxable amount broken down by rate | 11° — where several rates apply, each must be shown separately. [2] |

| Mention "Option pour le paiement de la taxe d'après les débits", where the supplier has exercised that option | 11° bis — one of the four new mentions. [2] |

| Reference to the exempting provision — the CGI article or the corresponding provision of Directive 2006/112/EC — where the supply is exempt | 12° — e.g. "Exonération TVA — Article 262 I CGI" on an export. The second particular a low-value or franchise invoice may omit. [2] |

| Mention "Autoliquidation" where the customer is liable for the tax | 13° — reverse charge. [2] |

| Mention "Autofacturation" where the customer issues the invoice in the supplier's name and on the supplier's behalf | 14° — self-billing under a mandat de facturation (art. 289 I-2 CGI and art. 242 nonies, Annexe II). [1] [2] |

| Mention "Régime particulier — Agences de voyages" | 15°. [2] |

| Margin-scheme mention for second-hand goods, works of art, collectors' items and antiques | 16°. [2] |

| Characteristics of a new means of transport as defined by art. 298 sexies CGI | 17°. [2] |

| For public auction sales: the hammer price, taxes and duties, and incidental charges shown distinctly, with no VAT stated | 18°. [2] |

Source snapshot captured 2026-08-03 — original. Légifrance itself refuses automated capture (HTTP 403), so this DILA restatement stands in for the article text; the citations above point to Légifrance directly.

Source snapshot captured 2026-08-03 — original. Légifrance itself refuses automated capture (HTTP 403), so this DILA restatement stands in for the article text; the citations above point to Légifrance directly.

The buyer's SIREN (within 1°), the delivery address (7° bis), the nature of the operations (8° bis) and the "option pour le paiement de la taxe d'après les débits" mention (11° bis) are already codified in Article 242 nonies A, but the décret that introduced them (décret n° 2022-1299 of 7 October 2022) defers their application: for operations within the scope of Article 289 bis CGI, they apply to invoices issued from 1 September 2026, and from 1 September 2027 for micro-enterprises and SMEs that are not members of an assujetti unique — the same phasing as the e-invoicing obligation itself. [4] The DGFiP's public guidance presents them as "les 4 nouvelles mentions obligatoires" arriving with the reform. [5]

Every other particular in the table above is in force now, for paper and PDF invoices alike.

Separately from the VAT particulars, French commercial law adds its own mandatory mentions to a B2B invoice — the payment due date, the late-payment penalty rate, the discount terms for early payment, and the €40 lump-sum recovery indemnity. Those are set out in the Invoice Information table above. [5]

Issuance deadline and numbering

Deadline. The general rule in Article 289, I-3 CGI is that the invoice is issued as soon as the supply of goods or the service is carried out ("dès la réalisation de la livraison ou de la prestation"). Two exceptions push the deadline out: [1]

- Exempt intra-EU supplies of goods and services on which the customer accounts for the tax — the invoice may be issued up to the 15th day of the month following the chargeable event.

- A facture récapitulative covering several distinct operations for the same customer within one calendar month must be drawn up by the end of that month.

An invoice is also required for acomptes (payments on account received before the supply is carried out), with limited exceptions for exempt intra-EU supplies. [1]

Numbering. The number must be unique, assigned chronologically as invoices are issued, and continuous — no gaps and no duplicates. Distinct series (with distinct prefixes, each internally continuous) are permitted where the business genuinely needs them: several invoicing sites, different customer categories, or outsourced invoicing. [2] [3] An issued invoice is never deleted or renumbered — see Invoice cancellation below.

Credit and debit notes

France has no separate "debit note" instrument for VAT. A correction is made either by a facture rectificative (a corrective invoice, used for both upward and downward corrections and for cancelling an invoice) or, for a price reduction granted after the event, by a note d'avoir (credit note). [6]

- A facture rectificative must carry an explicit reference to the original invoice (its number and date) and repeat the ordinary mandatory particulars. [6]

- A note d'avoir must reference the initial invoice and state the amount of the rebate excluding tax together with the corresponding VAT amount — "les notes d'avoir doivent porter référence à la facture initiale et indiquer le montant « hors taxes » du rabais consenti ainsi que le montant de la TVA correspondante". It must show both parties' names and addresses and the revised totals (HT and TVA). [6]

- Where referring to one specific original invoice is impossible, the credit note may refer to a group of invoices or to the contract, specifying the period covered. [6]

Currency and language

Currency. Amounts on the invoice may be expressed in any currency — "les montants figurant sur la facture peuvent être exprimés dans toute monnaie" — provided the VAT payable is determined in euros. [1] [3] The conversion mechanism is fixed by Article 266, 1 bis CGI: where the elements of the taxable base are expressed in a currency other than the euro, the rate to apply is the last rate published by the European Central Bank on the day the tax becomes chargeable (jour de l'exigibilité de la taxe). The rate used should be shown on the invoice. [7]

Language. The VAT rules do not require the invoice itself to be drafted in French. Where an invoice is drawn up in a foreign language, the administration may — for audit purposes only, not systematically — require a translation certified by a sworn translator ("l'administration peut, aux fins de contrôle, exiger une traduction des factures certifiée par un traducteur juré"). [3]

Simplified invoices

France does not operate a separate short-form retail invoice. Instead, Article 242 nonies A, II allows a reduced field set: invoices whose total excluding tax is €150 or less, invoices issued by suppliers under the franchise en base de TVA, and those covered by art. 289-5 CGI may omit two particulars only — the supplier's VAT identification number (2°) and the reference to the exempting provision (12°). Every other mandatory particular still applies. [2] [6]

The relief does not apply to intra-EU supplies, distance sales, or other cross-border operations where the exemption reference is required by another CGI provision. [6]

Retention

Six years for tax purposes. Under Article L102 B of the Livre des procédures fiscales, books, registers, documents and supporting papers subject to the administration's right of communication and control must be kept for six years — running from the date of the last operation recorded in the books or registers, or from the date the document was drawn up. Documents established or received in electronic form must be kept in that form for the whole six years; electronic-only archiving is therefore expressly accepted, and paper documents may also be kept in dematerialised form. [8]

Where they may be stored. Under Article L102 C LPF: [9]

- Invoices issued or received must be stored in France, unless they are stored electronically in a way that guarantees the administration immediate, complete online access.

- Electronic invoices may not be stored in a country outside the EU that has no mutual-assistance agreement with France or that denies the right of immediate online access.

- The storage location must be declared with the taxpayer's returns, and any change notified where the location is outside France.

A separate, longer commercial-law retention applies to accounting books and vouchers — see Record Keeping below.

Technical format

For an invoice outside the e-invoicing mandate there is no prescribed schema. What the law requires is that the authenticity of origin, integrity of content and legibility be guaranteed from issue to the end of the retention period, by any one of: documented business controls creating a reliable audit trail, a qualified electronic signature, a structured EDI message, or a qualified electronic seal under Regulation (EU) 910/2014. [1]

For operations within the scope of Article 289 bis CGI, the invoice must be a structured electronic invoice (Factur-X, UBL or CII) transmitted through a plateforme agréée or Chorus Pro — see Einvoicing below for scope, platforms and dates.

Einvoicing

Electronic invoicing, which was initially compulsory for public entities, is progressively expanding its reach to encompass professionals. The original 2024 launch was delayed and the reform was restructured around a 1 September 2026 generalisation:

- From September 1, 2026, all businesses must be able to receive structured electronic invoices, and large enterprises and intermediate-sized companies (ETI) must send their invoices electronically.

- From September 1, 2027, small and medium-sized enterprises (SMEs) and micro-enterprises must also send their invoices electronically.

- Transmission is via a certified private platform (Plateforme de Dématérialisation Partenaire — PDP) or the public portal Chorus Pro; accepted formats are Factur-X, UBL, or CII. (Source: DGFiP, impots.gouv.fr)

Record Keeping

Invoices issued by a company must be filed chronologically in a book of accounts. Issuance dates and invoice numbering must follow each other and be consistent.

Invoice numbers should be assigned using a unique, uninterrupted, and chronological sequence, ensuring that no two invoices share the same number.

The company has the flexibility to select different numbering series, for instance, F2023-01-001, 2023-001, etc. This flexibility may be applicable in the following circumstances:

- When there are multiple billing locations, using one series per site.

- When different customer categories necessitate distinct billing rules, assigning a series for each customer category.

- When invoice outsourcing is employed for certain invoices.

The invoice number is considered an essential detail and must be visible on all pages of the invoice. In cases where an invoice spans multiple pages, each page should be sequentially numbered as n/N (where n is the page's serial number, and N is the total number of pages comprising the invoice).

Invoices must be retained for a period of 10 years.

Accounting Entries:

- Ledger and ledger books, including journal books, ledgers, inventory books, etc., must be preserved for 10 years from the year-end.

- Vouchers, such as purchase orders (PO), shipment or receipt records, customer and supplier invoices, etc., should also be retained for 10 years from the year-end.

- In cases where these documents are received in electronic form, they must be maintained in that format for 6 years from the date of the last transaction.

Tax Documents:

- Income and business tax records should be stored for 6 years.

- Industrial and commercial profits (BIC), non-commercial profits (NTB), and agricultural profits (BA) under the real tax regime should also be retained for 6 years.

- Taxes on businesses for individual companies, limited liability businesses (including agricultural holdings and liberal practice businesses) should be preserved for 6 years.

- Records related to direct local taxes (such as property taxes) should be kept for 6 years.

- Documents pertaining to company property tax (CFE: Companies Formalities Center) and CVAE: Contribution on the added value of companies should be retained for 6 years.

- Turnover taxes, including Value Added Tax (VAT) and similar taxes, as well as taxes on shows and insurance agreements, should be preserved for 6 years

Invoice cancellation

In the case of an error or when a discount needs to be applied after an invoice has been issued, it is not permissible to simply delete the original invoice to maintain the sequential numbering of invoices. Instead, there are two accepted methods for rectifying the situation:

Generate a New Invoice

Create a new invoice, and in the reference section, make mention of the canceled invoice. Clearly indicate that this new invoice supersedes the initial one.

Generate a Credit Note: In situations where a discount is granted after the original invoice has been issued, you should issue a credit note. The credit note should reference the details of the initial invoice, including the invoice number and date, and clearly state the reason for the credit. This effectively adjusts the amount owed or accounts for any discrepancies.

Recent changes

Dated, officially-sourced changes to French VAT, newest first. The full history is in our worldwide tax-updates feed.

- 2026-02-18 — DGFiP rescrit BOI-RES-TVA-000253 confirms that BOFiP doctrine and individual rulings issued under CGI VAT provisions remain applicable under the corresponding CIBS Book II articles once Ordonnance n° 2025-1247 of 17 December 2025 (JORF 20 December 2025) recodifies France's legislative VAT provisions from the CGI into the Code des impositions sur les biens et services on 1 September 2026. (DGFiP) — see issue

Reference links

- DGFiP — Les régimes d'imposition à la TVA (franchise en base thresholds)

- DGFiP — Je passe à la facturation électronique

- DGFiP — Facturation électronique et plateformes agréées

- Intra community VAT number

- Using EDI

- Electronic signature

- BOI-RES-TVA-000253 — transitional provisions for the CGI → CIBS VAT recodification (DGFiP)

- France SIREN validator

Frequently Asked Questions

What happens if I accidentally charge TVA while under the franchise en base de TVA regime?

The franchise en base thresholds, in force since 1 January 2025, are €85,000 for ventes de marchandises (seuil majoré €93,500) and €37,500 for prestations de services (seuil majoré €41,250). [1]

If a business under the franchise en base (Article 293B CGI) mistakenly charges TVA, the TVA becomes due to the DGFiP — because the invoice itself creates a tax debt (Article 283-3 CGI). The business must remit the full TVA collected but cannot offset any input TVA. The customer cannot reclaim the incorrectly charged TVA. Correct the error by issuing a credit note and reissuing without TVA. Repeated errors can trigger mandatory TVA registration. [2]

What is the difference between autoliquidation and exonération on a French invoice?

Autoliquidation (reverse charge): TVA is due but accounted for by the buyer. Invoice must state "Autoliquidation — TVA à acquitter par le preneur." Used for B2B cross-border EU services (Art. 283-2 CGI), construction subcontracting (Art. 283-2 bis). Exonération (exemption/zero-rating): No TVA is due at all — state the legal basis (e.g. "Exonération TVA — Article 262 I CGI" for exports). Confusing the two causes incorrect accounting — autoliquidation recipients must self-report TVA; exonération recipients do not. [1]

France's e-invoicing mandate — what is the current timeline?

France's B2B e-invoicing mandate was restructured after the original 2024 launch was delayed. Current timeline: (1) September 2026: all businesses must be able to receive structured e-invoices; large enterprises and ETIs must send e-invoices; (2) September 2027: SMEs and micro-enterprises must send e-invoices. Transmission via a certified platform (PDP) or the public portal Chorus Pro. Required formats: Factur-X, UBL, or CII. Since the 2025 reform of the platform framework, the DGFiP registers plateformes agréées for renewable three-year terms — only a registered platform may transmit invoices and report data to the administration. [1] [2]

Do my French VAT obligations change when the CGI articles move to the CIBS on 1 September 2026?

Not substantively — but your citations do. Ordonnance n° 2025-1247 of 17 December 2025 (JORF 20 December 2025) recodifies France's legislative VAT provisions out of the Code général des impôts into Book II of the Code des impositions sur les biens et services (CIBS) with effect from 1 September 2026, à droit constant: the article numbering changes, the rules do not. DGFiP rescrit BOI-RES-TVA-000253 of 18 February 2026 confirms that existing BOFiP doctrine and individual rulings issued under the CGI provisions remain applicable under the corresponding CIBS articles, so a rescrit you hold under a CGI article stays opposable to the administration. What to update for periods from 1 September 2026: statutory references in contracts and terms, invoice legal mentions (for example the franchise en base mention citing Article 293 B CGI, and the export exemption mention citing Article 262 I CGI), VAT documentation, and tax-engine configuration. Because the same date starts the B2B e-invoicing mandate, plan both in one cutover. [1]

My French supplier's TVA number fails on VIES — but they say they're registered. What should I do?

A French TVA number (format: FR + 2 check characters + 9-digit SIREN) failing on VIES may mean: (1) the business is under franchise en base — no TVA registration exists; (2) new registration lag (1–5 days before DGFiP updates VIES); (3) data entry error; (4) deregistration. Ask for an attestation de régularité fiscale from the DGFiP. Do not apply reverse charge or zero-rating until VIES confirms the number. [1]

For more details on French tax identifiers including TVA number format, see our France TVA Verification Guide.