E-invoicing in Poland

| Country | Poland |

| Status - B2G | Non Mandatory |

| Status - B2B | Non Mandatory |

| Status - B2C | NA |

| Formats | PEPPOL BIS, UBL UN/CEFACT CII |

| Authority | |

| Network name | Krajowy System e-Faktur(KSeF) |

Electronic invoicing (e-invoicing) is undergoing a major transformation in Poland. Starting July 2024, businesses will be required to issue and receive invoices through the National e-Invoicing System (Krajowy System e-Faktur or KSeF). This new centralized system represents the biggest change in VAT invoicing and will impact most companies operating in Poland.

The new regulations introduce the concept of a "structured invoice" which must comply with a specific XML format defined by the Ministry of Finance. E-invoices issued and received through KSeF will be given a unique identification number and stored electronically.

Legal Basis and Timeline

Poland's mandatory e-invoicing system is being introduced based on the following legal acts:

- Act of 29 October 2021 on amending the VAT Act – introduced voluntary e-invoicing via KSeF from 1 Jan 2022.

- Regulation on the use of the National e-Invoicing System – defines requirements for issuing and receiving e-invoices.

- Council Implementing Decision of 17 June 2022 – authorized Poland to introduce mandatory e-invoicing for Jan 2024 – Dec 2026.

- Act of 16 June 2023 amending the VAT Act – establishes mandatory e-invoicing via KSeF from 1 July 2024.

Important Deadlines

The timeline for KSeF rollout is as follows:

- 1 Jan 2022 – Launch of voluntary KSeF for issuing and receiving e-invoices

- 1 July 2024 – Launch of mandatory e-invoicing for domestic and foreign VAT payers with registered office or fixed establishment in Poland

- 1 Jan 2025 – Penalties introduced for not using KSeF for VAT invoices. Cash register receipts eliminated as simplified invoices.

Poland obtained approval from the EU Council to introduce mandatory e-invoicing for the period from Jan 2024 until Dec 2026. The system will become obligatory for most VAT registered businesses from 1 July 2024.

Scope of KSeF

The mandatory scope of KSeF covers B2B invoices issued by:

- Polish VAT payers to domestic and foreign clients

- Foreign taxpayers with a Fixed Establishment (FE) in Poland

Voluntary e-invoicing via KSeF is permitted for:

- Invoices issued by foreign entities registered for VAT purposes in Poland without FE

- Invoices issued by taxpayers with FE in Poland if FE is not involved

Excluded from KSeF are:

- B2C invoices issued to non-business individuals

- Invoices under special OSS and IOSS schemes

- Specific cases per Ministry of Finance

There is still uncertainty around which foreign entities will be considered as having a FE in Poland and therefore fall under the mandatory scope. Many companies are applying for individual tax rulings to clarify their status.

Access to KSeF

To access KSeF, taxpayers must authenticate using:

- Qualified electronic signature

- Qualified electronic stamp

- Trusted ePUAP Profile

- Unique TOKEN generated and assigned by KSeF

Authorizations to issue, receive or correct e-invoices can be granted electronically to other entities. Alternatively, paper authorizations can be filed for entities without an e-stamp.

When granting authorizations, it's important to restrict access only to selected individuals and prevent unmonitored access to all invoices.

Structured E-Invoice Format

E-invoices issued and received via KSeF must comply with an XML schema format published by the Ministry of Finance.

The FA(2) format specifies:

- Mandatory fields required by VAT Act

- Non-mandatory fields commonly used

- Single structure for all invoice types

Issuing non-compliant e-invoices will result in penalties. Taxpayers should validate invoices against the FA(2) schema before sending to KSeF.

The format does not allow attaching supplementary files or documentation to e-invoices. Any additional information must be provided via links or separate communication.

Issuing and Receiving E-Invoices via KSeF

There are several methods for issuing and receiving e-invoices via KSeF:

- Commercial invoicing software integrated with KSeF API

- Additional external platforms linking company systems with KSeF

- Free KSeF tools provided by Ministry of Finance

E-invoices can be sent individually or in batches. KSeF verifies the invoice format and credentials before assigning a unique KSeF identification number.

Buyers can access e-invoices by providing:

- KSeF identification number

- Seller's invoice number

- Buyer tax ID or other identifier

- Buyer name

- Invoice total amount

An e-invoice is considered issued when submitted to KSeF and received when the identification number is assigned. Dates are key for accounting and VAT reporting.

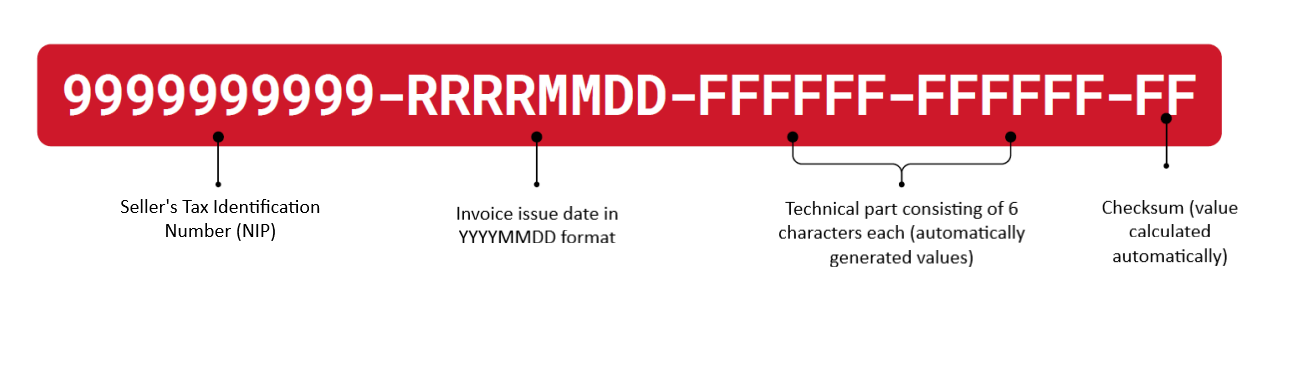

KSeF number format

The KSeF number is a unique number that identifies the invoice in the National e-Invoice System

|

| KSeF number format |

E-Invoice Corrections

The use of KSeF simplifies the process for correcting e-invoices:

- Value reductions are accounted for in the period the correction is received

- No formal acceptance by buyer is required

- Correcting non-structured invoices must still follow standard procedures

Corrections of invoices issued before 1 July 2024 must also be handled via KSeF. This requires retaining details of invoices issued outside the system.

KSeF Breakdowns and Unavailability

Special rules apply when KSeF is unavailable due to system failures or taxpayer issues:

- System Failure – Invoices can be issued in any format. Structured e-invoices must be resent within 7 days.

- Taxpayer Issues – Structured e-invoices must be issued. Resending to KSeF required within 1 day.

In these situations, alternate invoice delivery should be agreed with trading partners to avoid disruptions. The exact timing and format requirements differ depending on the nature of the outage.

Advantages and Challenges

The KSeF brings several benefits but also key challenges:

Advantages:

- Faster VAT refunds (40 instead of 60 days)

- Easier process for correcting invoices

- Invoice archiving for 10 years

- Single e-invoicing standard

Challenges:

- Adapting sales and purchase invoice workflows

- New format requires more invoice data

- Determining KSeF mandatory scope for foreign clients

- Changing dates of issuance and receipt

- Integrating accounting systems with KSeF

- New procedures for KSeF unavailability

Security Concerns

As a central repository of B2B invoices, the KSeF will contain sensitive information attractive for cyberattacks. Key recommendations:

- Apply multi-factor authentication for system access

- Encrypt invoice transmissions

- Carefully restrict user authorization levels

- Validate integration points between company systems and KSeF

- Actively monitor for unauthorized access attempts

Implementation Recommendations

To ensure a smooth transition to e-invoicing, companies should take the following steps:

- Conduct impact analysis of invoice flows and data availability

- Assess required changes to accommodate new formats

- Consult with clients on e-invoice information and integration

- Prioritize KSeF in IT development plans

- Test invoice handling with KSeF in advance

- Update internal controls and procedures

- Validate issuer-receiver business processes end-to-end

- Provide KSeF training and support for impacted staff

Companies that prepare thoroughly and test KSeF integrations well before the deadlines will avoid disruptions. It's recommended to engage closely with the IT department and external software vendors early in the process.

Frequently Asked Questions

What is the current KSeF mandatory timeline — why was the July 2024 launch cancelled and when does it actually apply?

Poland's original mandatory KSeF date of 1 July 2024 was cancelled in June 2024 following a government audit that found critical technical flaws in the system. A new phased timeline was established and signed into law:

- 1 February 2026: Mandatory for large taxpayers whose 2024 gross sales exceeded PLN 200 million (including VAT)

- 1 April 2026: Mandatory for all other VAT-registered businesses

- 1 January 2027: Mandatory for micro-entrepreneurs with monthly invoice values below PLN 10,000 gross

The new system uses an entirely redesigned FA(3) XML schema, replacing the earlier FA(2) format. No financial penalties apply during 2026 — enforcement of fines begins on 1 January 2027. [1] [2]

I am a foreign company registered for Polish VAT but have no fixed establishment in Poland — do I need to use KSeF?

No. KSeF is not triggered solely by holding a Polish VAT registration number (NIP). The mandatory obligation applies only where a taxpayer has a fixed establishment (stałe miejsce prowadzenia działalności / FE) in Poland AND that fixed establishment participates in the specific supply being invoiced.

Foreign companies registered for Polish VAT without a Polish fixed establishment are currently excluded from the mandatory KSeF obligation. However, Polish buyers may still send KSeF-structured invoices to such foreign sellers in self-billing arrangements, and there is ongoing uncertainty about which foreign entities will be deemed to have a fixed establishment. Individual advance tax rulings (interpretacja indywidualna) from the Polish tax authority are advisable for businesses in borderline situations. [1] [2]

What happens when KSeF is unavailable — can I still invoice my customers and what are the submission deadlines?

KSeF includes a defined offline mode for situations where the system is unavailable or the taxpayer cannot connect. When the Ministry of Finance officially announces a KSeF system failure (published in the BIP public bulletin), invoices may be issued in any format outside KSeF and delivered directly to the buyer. Such invoices must then be submitted to KSeF within 1 business day after the system is restored.

Where the outage is on the taxpayer's side (connectivity failure, technical issue), structured e-invoices in the correct format must still be issued and can be delivered to the buyer directly, but must be uploaded to KSeF within 1 business day. The offline mode with special QR code markers remains available until 31 December 2026. Since no penalties apply in 2026, failure to meet the resubmission deadline carries no financial consequence until 1 January 2027. [1] [2]

How do self-billing arrangements work under KSeF — can my Polish buyer still issue invoices on my behalf?

Self-billing (wystawianie faktur przez nabywcę) is permitted under KSeF but requires the seller to formally grant the buyer authorisation in KSeF using a ZAW-FA notification form. Once granted, the buyer can issue and transmit the self-billed invoice through KSeF on behalf of the seller, and the invoice receives a KSeF number as normal.

However, self-billing transactions are exempt from KSeF if either the seller or the buyer does not hold a Polish Tax Identification Number (NIP) — for example, where a foreign business without a Polish NIP is either the invoicing party or the recipient. Businesses currently operating self-billing arrangements should verify NIP status for all parties and ensure the required KSeF authorisation is in place before their applicable mandatory date. [1] [2]

How are correction invoices (faktury korygujące) handled in KSeF, and do I need the buyer's formal acceptance?

Under KSeF, correction invoices that reduce the value of the original supply are accounted for in the tax period in which the correction is submitted to KSeF and assigned a KSeF number — no formal written acceptance by the buyer is required. This is a simplification compared to the pre-KSeF rules for value-reducing corrections. The correction must reference the original invoice's KSeF number.

For corrections to invoices issued before the mandatory KSeF date (before 1 February or 1 April 2026 depending on company size), those corrections must still be submitted through KSeF, meaning sellers must retain identifying details of pre-KSeF invoices to reference them correctly. Correction notes (noty korygujące) issued by buyers to correct formal errors not affecting the tax base continue to follow existing rules and do not flow through KSeF. [1] [2]

What are the penalties for issuing invoices outside KSeF after the grace period ends, and what exactly triggers the fine?

From 1 January 2027, the head of the relevant tax office may impose a financial penalty for each invoice issued outside KSeF in breach of the obligation. The penalty is calculated as:

- Up to 100% of the VAT amount shown on the non-compliant invoice

- Up to 18.7% of the gross invoice amount for invoices carrying no VAT (zero-rated or VAT-exempt supplies)

The fine is imposed by administrative decision and may be reduced under Administrative Procedure Code mitigation rules. The penalty applies per invoice, meaning high-volume issuers with systematic non-compliance face compounding exposure. During 2026, no financial penalties apply regardless of KSeF errors — this year serves as a regulatory grace period. Businesses should treat 2026 as an implementation and testing window and aim for full compliance before 1 January 2027. [1] [2]